India E-invoice

Provinces

General

Provinces

General

About

General

About

General

General

General

Managed by the Goods and Services Tax Network (GSTN). Centralized Invoice Registration Portal (IRP) validates and issues e-invoices. Aims to simplify GST compliance, reduce tax evasion, and improve transparency.

India adopted e-invoicing under GST law to increase transparency and reduce tax evasion:

India adopted e-invoicing under GST law to increase transparency and reduce tax evasion:

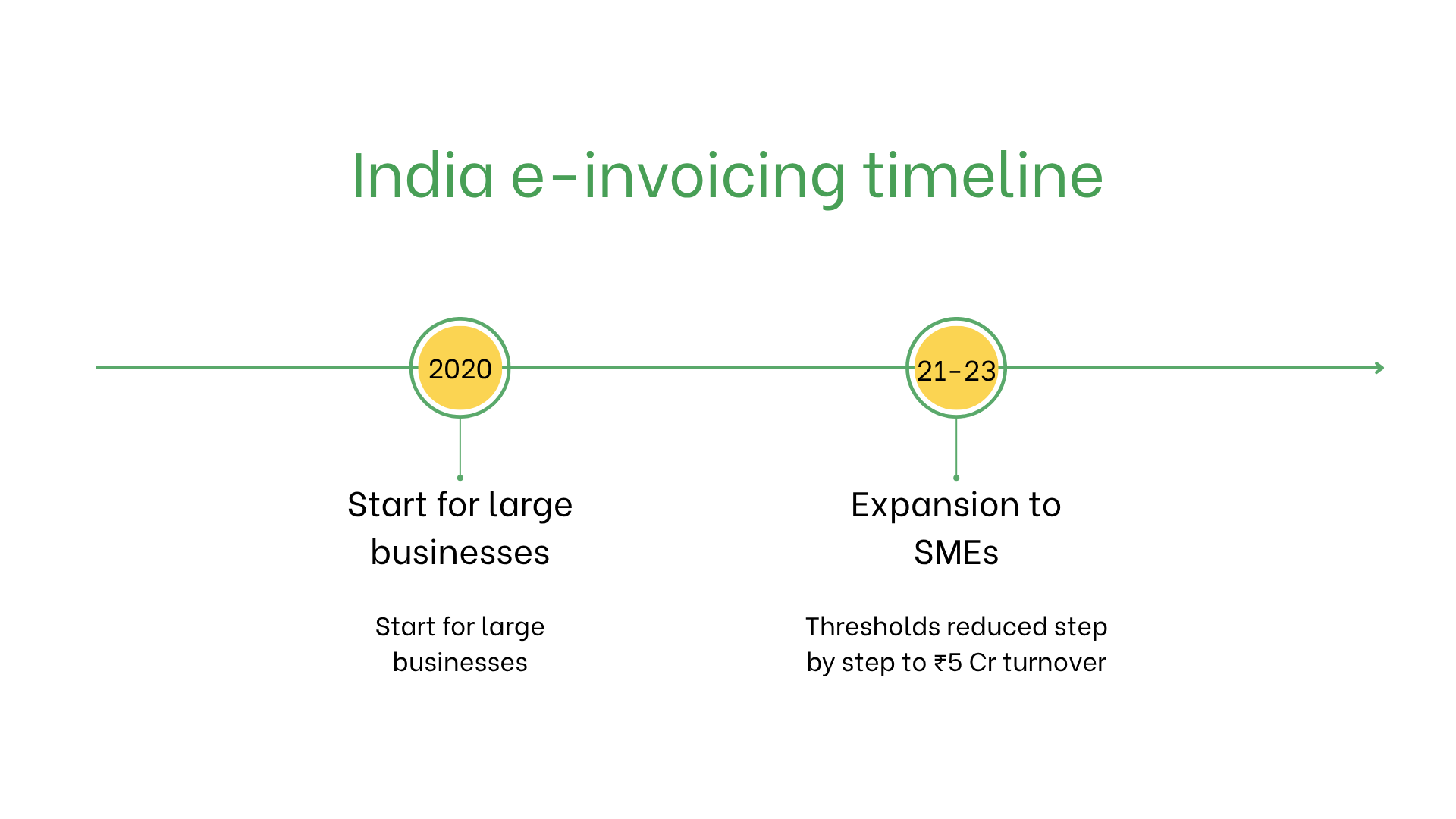

Implementation of mandatory e-invoicing in India

India adopted e-invoicing under GST law to increase transparency and reduce tax evasion:

- Starting October 2020, e-invoicing became mandatory for businesses with turnover over ₹500 crore. This threshold was progressively lowered.

- By August 2023, the limit was reduced to ₹5 crore, bringing many SMEs under the system. Invoices must be submitted to the Invoice Registration Portal (IRP) for validation and QR code generation.

Who needs e-invoices in India?

E-invoicing in India is required for:- Large Enterprises: Businesses with turnover above 10 crore must comply by issuing e-invoices.

- SMEs: Included in rollout based on turnover thresholds.

- Exporters: Required for export transactions, ensuring integration with GST returns.

- Non-resident businesses: Exempt unless GST-registered for business transactions in India.

E-Invoicing vs. E-Billing

| Aspect | E-Invoicing | E-Billing |

| Purpose | GST compliance, mandatory by law | Internal/customer transactions |

| Validation | Real-time via IRP | Not validated |

| Format | JSON with structured GST details | Flexible, non-mandatory formats |

| Archiving | Required for 8 years | Optional |

Key features of India’s e-invoicing system

India’s e-invoicing system ensures real-time validation through the Invoice Registration Portal (IRP), which includes:- Real-Time Validation: IRP validates invoices, generates an Invoice Reference Number (IRN) and a QR code.

- Submission Format: JSON format for digital processing.

- Archiving: E-invoices must be stored electronically for 8 years.

E-invoicing dataset

- Buyer/Seller IDs: GSTINs for both parties.

- Invoice Details: Number, date, and supply type (domestic/export).

- Goods and Services: HSN codes, quantities, unit prices, and VAT details.

- Taxes: CGST, SGST, or IGST amounts.

- Transaction Info: Total payable amount, currency, and payment terms.

- QR Code: Encodes invoice data for simplified verification.

E-invoicing across transaction types

B2B Transactions:- Mandatory validation through IRP.

- Facilitates compliance and input tax credit claims.

- Not mandatory, but QR-coded invoices improve customer experience.

- Required for goods/services supplied to government entities.

Penalties for non-compliance

- Fines: Penalties up to 10,000 (approximately €120) per invoice, along with additional late fees for filing discrepancies.

- Input Tax Credit Denial: Buyers may lose eligibility for tax credits on non-compliant invoices.

- Legal Risks: Repeated violations can trigger audits and reputational damage.

Subscribe to the newsletter

No spam, only interesting news