Poland E-invoice

Provinces

General

Provinces

General

About

General

About

General

General

General

Managed by the Ministry of Finance through the Krajowy System e-Faktur (KSeF) platform. Aims to enhance tax compliance, reduce VAT fraud, and streamline business operations.

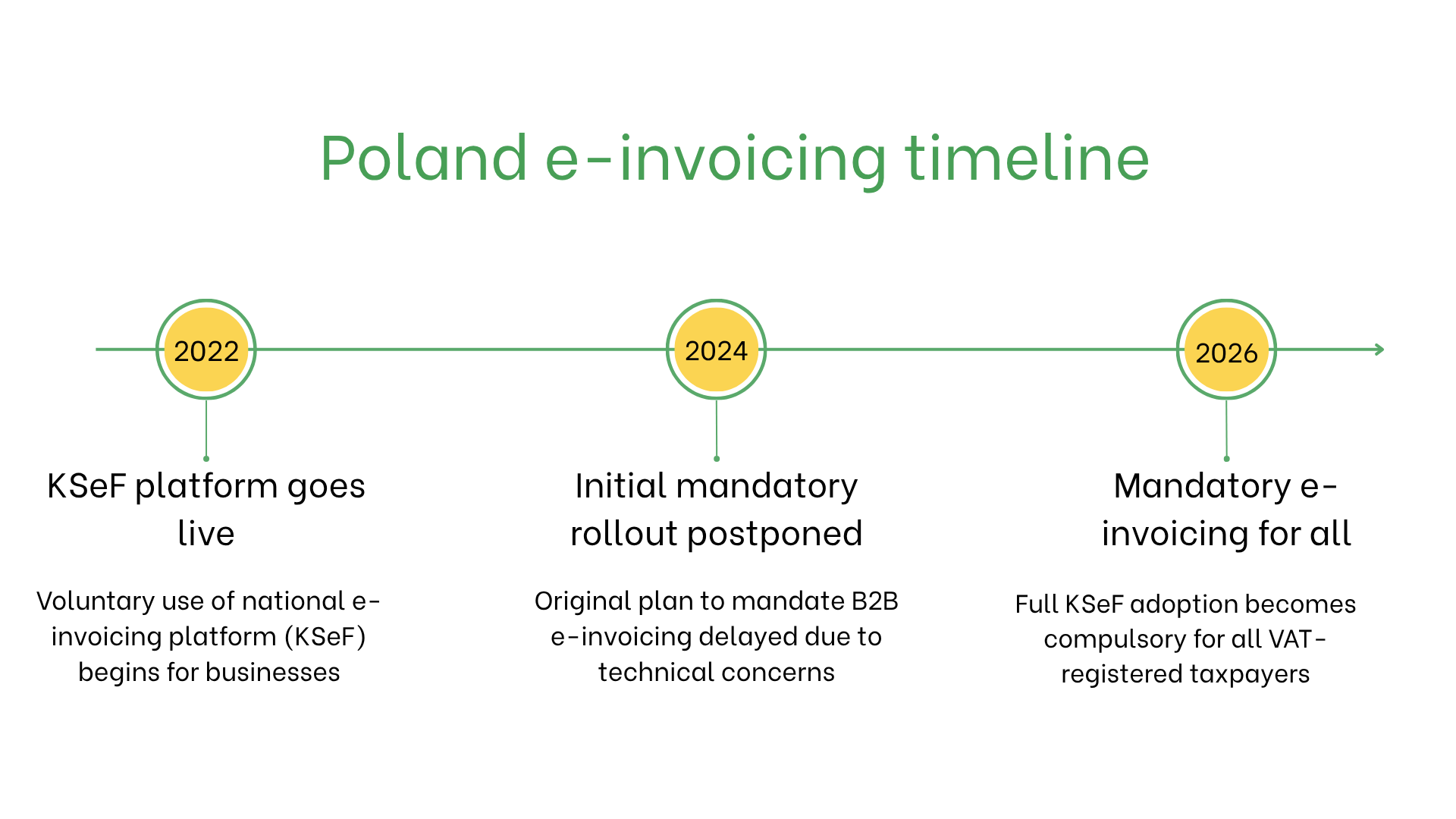

Poland is introducing mandatory B2B e-invoicing through the government-operated KSeF (Krajowy System e-Faktur) platform, gradually transitioning from voluntary to compulsory adoption:

Poland is introducing mandatory B2B e-invoicing through the government-operated KSeF (Krajowy System e-Faktur) platform, gradually transitioning from voluntary to compulsory adoption:

Implementation of mandatory e-invoicing in Poland

Poland is introducing mandatory B2B e-invoicing through the government-operated KSeF (Krajowy System e-Faktur) platform, gradually transitioning from voluntary to compulsory adoption:

- January 1, 2022: The Polish Ministry of Finance launched the voluntary phase of its e-invoicing system, allowing businesses to issue and receive structured e-invoices via KSeF. Early adopters gained benefits such as faster VAT refunds (up to 40 days instead of 60).

- 2024 (original date): E-invoicing was initially planned to become mandatory for all VAT taxpayers starting July 1, 2024, but the rollout was postponed due to major concerns over KSeF's readiness, performance, and cybersecurity vulnerabilities. The government announced that more time was needed to stabilize the platform and respond to stakeholder feedback.

- New date – February 1, 2026: The revised mandatory implementation date for B2B e-invoicing in Poland has now been set for February 2026. All VAT-registered businesses will be required to issue invoices exclusively via KSeF. This includes issuing, receiving, archiving, and auditing processes. Traditional invoice formats (PDFs, paper) will no longer be valid for VAT purposes.

Who needs e-invoices in Poland?

E-invoicing in Poland is required for:- Large Enterprises: Mandatory starting July 2024 for all domestic and cross-border VAT transactions.

- SMEs: Subject to the same mandatory requirements starting July 2024.

- Non-Resident Businesses: May be required to issue e-invoices for transactions with Polish VAT-registered entities.

E-Invoicing vs. E-Billing

| Aspect | E-Invoicing | E-Billing |

| Purpose | Tax compliance through KSeF | Informal or customerfocused transactions |

| Format | Structured formats required by KSeF | Flexible, non-regulated formats |

| Validation | Real-time via KSeF | Not validated |

| Archiving | Mandatory for 10 years | Optional |

Key features of Poland’s e-invoicing system

- Submission Platform: Invoices must be submitted via KSeF for validation before being shared with recipients.

- Compliance Checks: Validation includes format checks, VAT calculations, and buyer-seller identification.

- Archiving: Invoices must be archived digitally for at least 10 years.

E-Invoicing dataset

- Buyer/Seller IDs: VAT identification numbers.

- Invoice Details: Invoice number, issue date, and payment terms.

- Goods and Services: Descriptions, quantities, and pricing.

- Taxes: Applicable VAT rates and amounts.

- Transaction Info: Total payable amount, currency, and payment method.

E-invoicing across transaction types

B2B Transactions:- Mandatory e-invoicing ensures accurate tax reporting and faster payment cycles.

- Cross-border B2B transactions must also comply with KSeF requirements starting in 2024.

- While not mandatory for most B2C transactions, e-invoicing can be used to streamline processes and improve customer experience.

- Businesses may issue electronic receipts for transparency and efficiency.

- E-invoicing is already mandatory for transactions with government entities, ensuring compliance with public procurement regulations.

Penalties for non-compliance

- Fines: Up to 100% of the VAT amount or a specified monetary penalty per invoice.

- Operational Delays: Rejected invoices can disrupt payment and cash flow.

- Legal Risks: Increased likelihood of audits or disputes due to non-compliance.

Subscribe to the newsletter

No spam, only interesting news