Marketplace Facilitator Laws Explained for Amazon, Etsy and eBay Sellers

Marketplace Facilitator Laws Explained for Amazon, Etsy and eBay Sellers

Selling on a marketplace feels easy until a levy notice arrives. Then sellers ask one question. Who owes the money, the company or me. The answer is both, for different parts of the business. Marketplace facilitator laws reshaped online sales duty in the US. Similar rules now shape VAT in the UK and EU. This guide explains when Amazon, Etsy and eBay handle the charge for you, and where your own duties remain.

Expect plain answers, comparison tables and short checklists you can use this week.

What Marketplace Facilitator Tax Means for Sellers

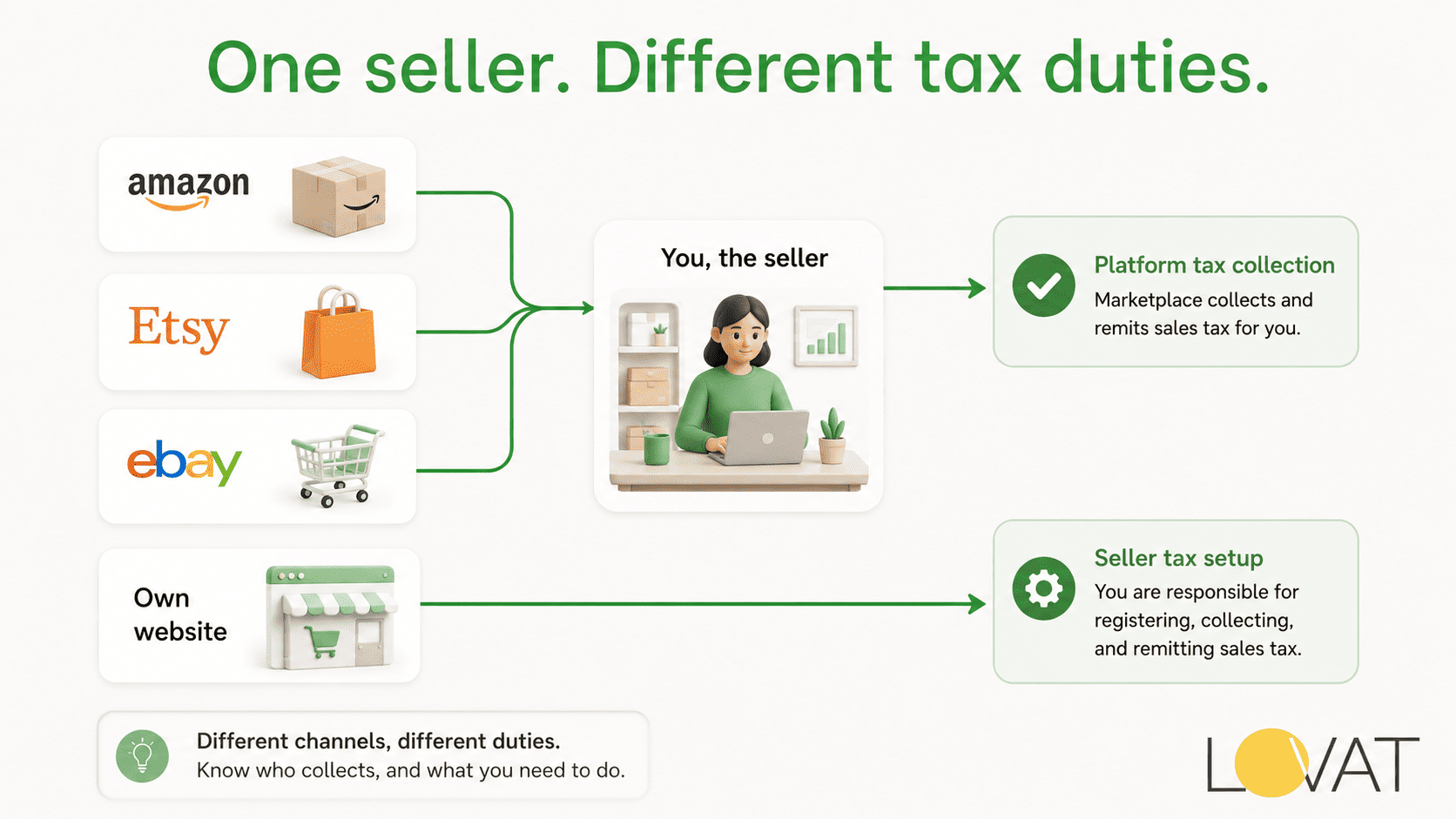

A facilitator is a site that lists goods, takes payment, and pays the merchant. Amazon, Etsy, eBay and Walmart Marketplace all fit this description for most listings.

Marketplace facilitator laws require these sites to collect a charge for third-party merchants, instead of leaving that job to each shop owner. Authorities find it easier to audit one large company than thousands of small businesses.

This rule now exists in nearly every part of the US with a general sales levy. That single fact matters more than any other detail on this page.

Background to the Wayfair Decision

The starting point is South Dakota v. Wayfair, a 2018 Supreme Court case. Before that ruling, an authority could only force collection on a business with a physical footprint there, such as an office or stock.

Wayfair changed that. Lawmakers gained the right to base a duty on economic activity alone. This is called economic nexus, usually set by a revenue amount, a transaction count, or both.

Once nexus became legal, officials saw that small marketplace merchants rarely crossed those limits alone. So legislators placed the collection duty on the companies that process the bulk of online trade instead.

What Is Marketplace Facilitator Tax in Practice

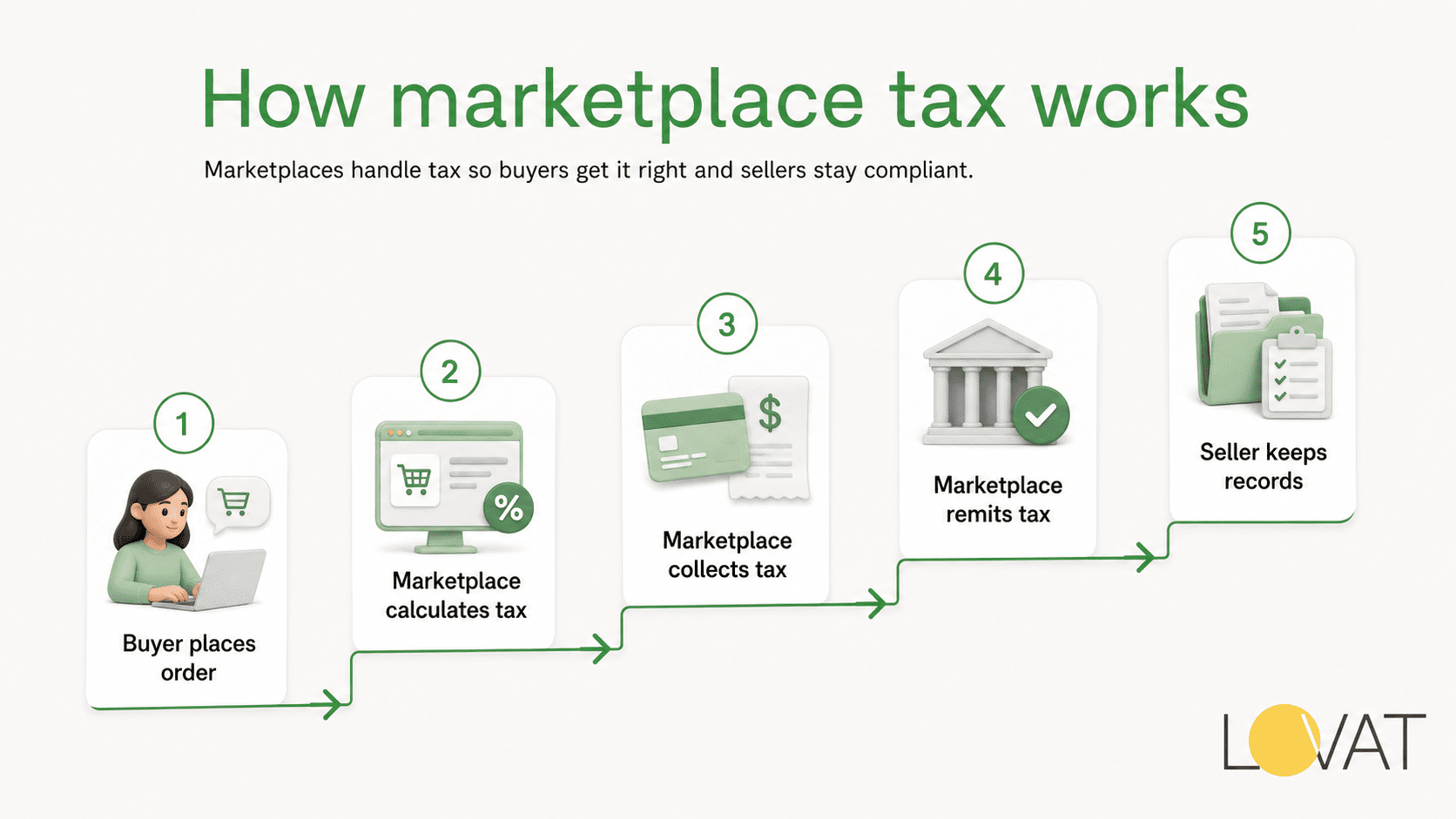

What is marketplace facilitator tax, in one line. It is the charge a site collects and pays to an authority on a merchant’s behalf. The shop owner never holds that money. It moves from buyer to site to revenue office directly.

A few points follow from this:

- The rate applied depends on the buyer’s address, not the merchant’s

- The duty starts once the marketplace crosses a threshold, not the merchant alone

- Businesses cannot opt out where the rule is mandatory

- Coverage applies to orders placed through that company only, not off-site revenue

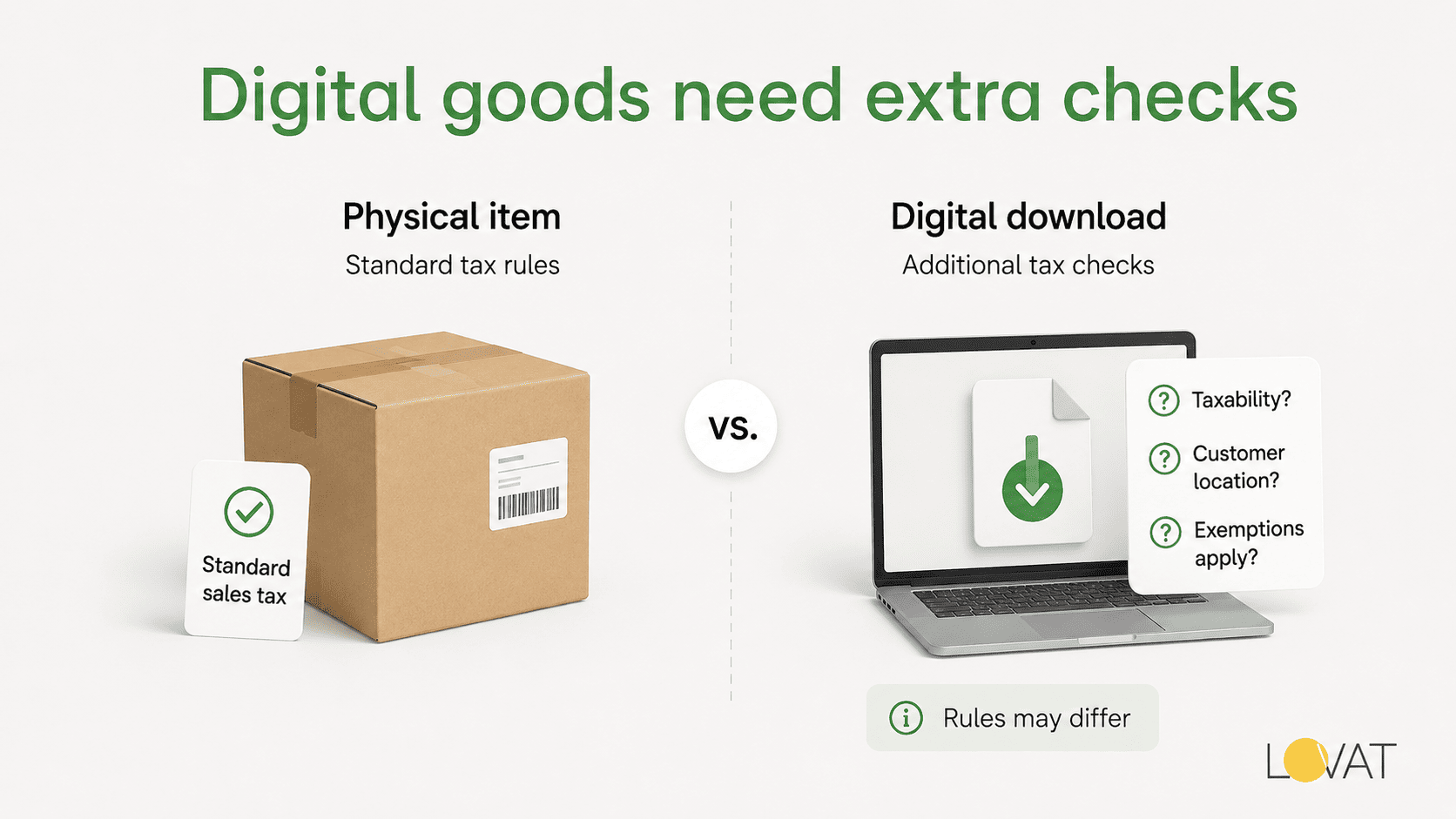

- Digital products are increasingly included, though wording differs by jurisdiction

Once a business owner can answer what is marketplace facilitator tax in one sentence, the next question follows naturally, since knowing what marketplace facilitator tax really covers shapes every later registration choice.

Why Lawmakers Shifted Collection to Platforms

Before these rules, enforcement was weak. An office might track tens of thousands of small shops shipping a handful of parcels each month. Many never registered, and many buyers never reported a use charge on their own.

By placing marketplace facilitator tax duty on platforms, authorities cut that workload sharply. A handful of large companies now cover most online sales levy revenue.

For merchants, this created a split. Some orders carry an automatic charge. Others, mainly a direct website or wholesale revenue, do not. Mixing the two without clear bookkeeping is the top mistake we see in support tickets. Sorting which orders carry a built-in duty and which do not is the first habit worth building.

Amazon Sales Tax Collection Step by Step

Amazon was an early mover on building automatic logic into checkout. Today, Amazon handles Amazon sales tax collection in nearly every US state that imposes a facilitator rule.

Here is what that means for a third-party shop owner.

- Amazon sets the rate from the ship-to address

- Amazon adds that amount at checkout

- Amazon sends the collected sum to the right revenue office

- The payout excludes that sum, since it never belonged to the merchant

- Sellers can view the breakdown inside Seller Central reports

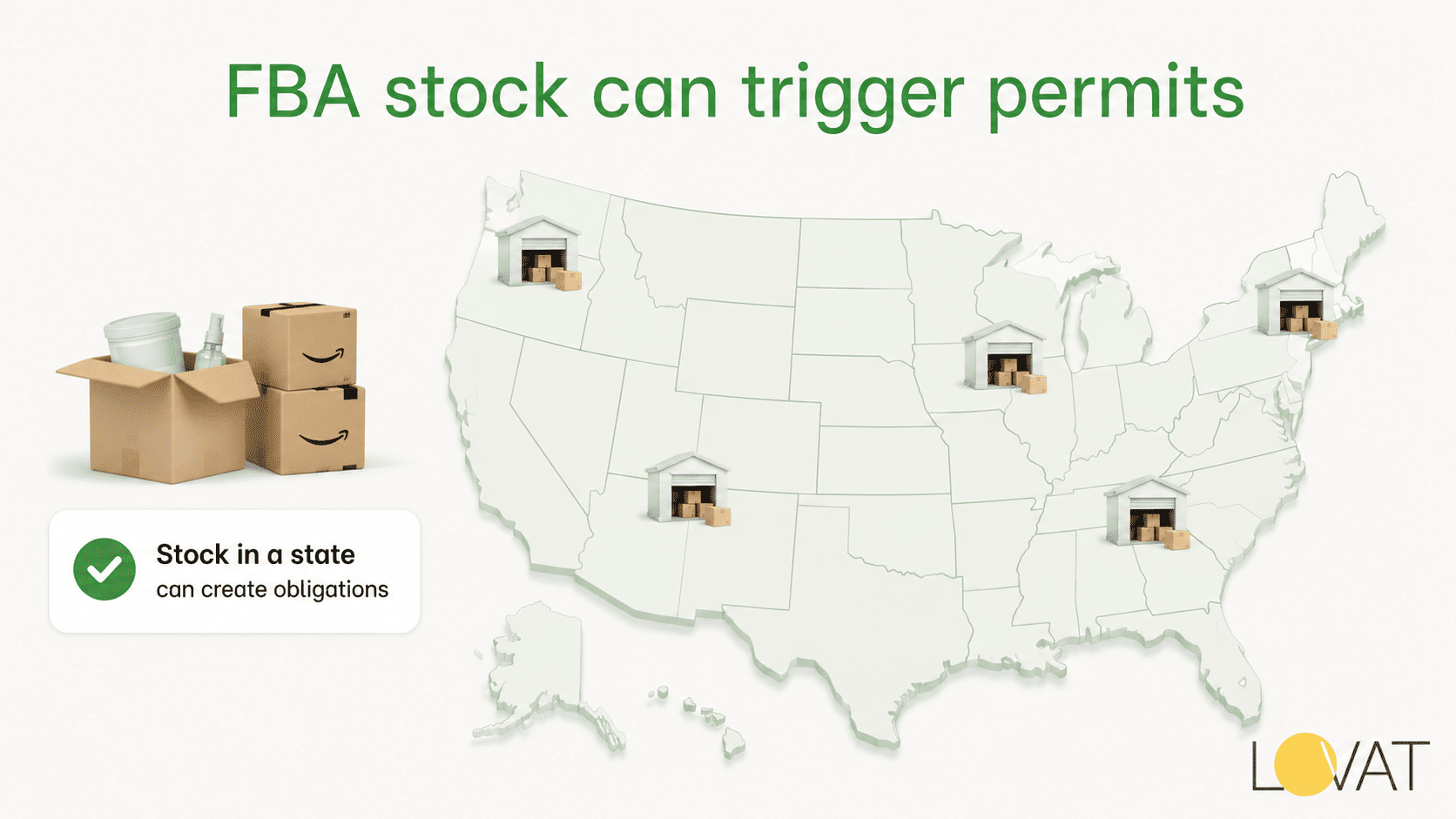

Amazon sales tax collection runs the same way in every covered state, with no manual switch for a merchant to flip. This does not remove every duty. A business based in a given state, holding FBA stock there, or trading through other channels there, may still need an active permit, even while Amazon manages the checkout-level charge.

Etsy Sales Tax Duties for Shop Owners

Etsy sales tax works on the same basic model, with a few quirks that catch craft businesses off guard.

Etsy applies a charge automatically on orders shipped into states with a facilitator law. Etsy sales tax works the same way across most covered areas, with no per-listing override for the shop owner. Most shop owners never touch a rate field for those areas. Adding a manual entry for an already-covered area usually causes a double charge.

Sales Tax Etsy Sellers Often Get Wrong

Where sales tax Etsy gets tricky is digital downloads. Some places treat digital goods like physical ones for revenue purposes. Others exempt certain digital items entirely. Etsy applies its own logic by category, but a shop owner should still confirm settings match the listed product type.

Etsy also began sharing earnings data with UK and EU authorities under new reporting duties, a separate matter from collecting a charge at checkout. How Etsy applies the levy and how Etsy reports income to HMRC are two different processes that merchants often mix up. We cover that distinction further down.

eBay Sales Tax Rules Sellers Must Understand

eBay sales tax follows the same structure. eBay applies and pays a charge for orders shipped into states with a facilitator law, at the rate set by the buyer’s address.

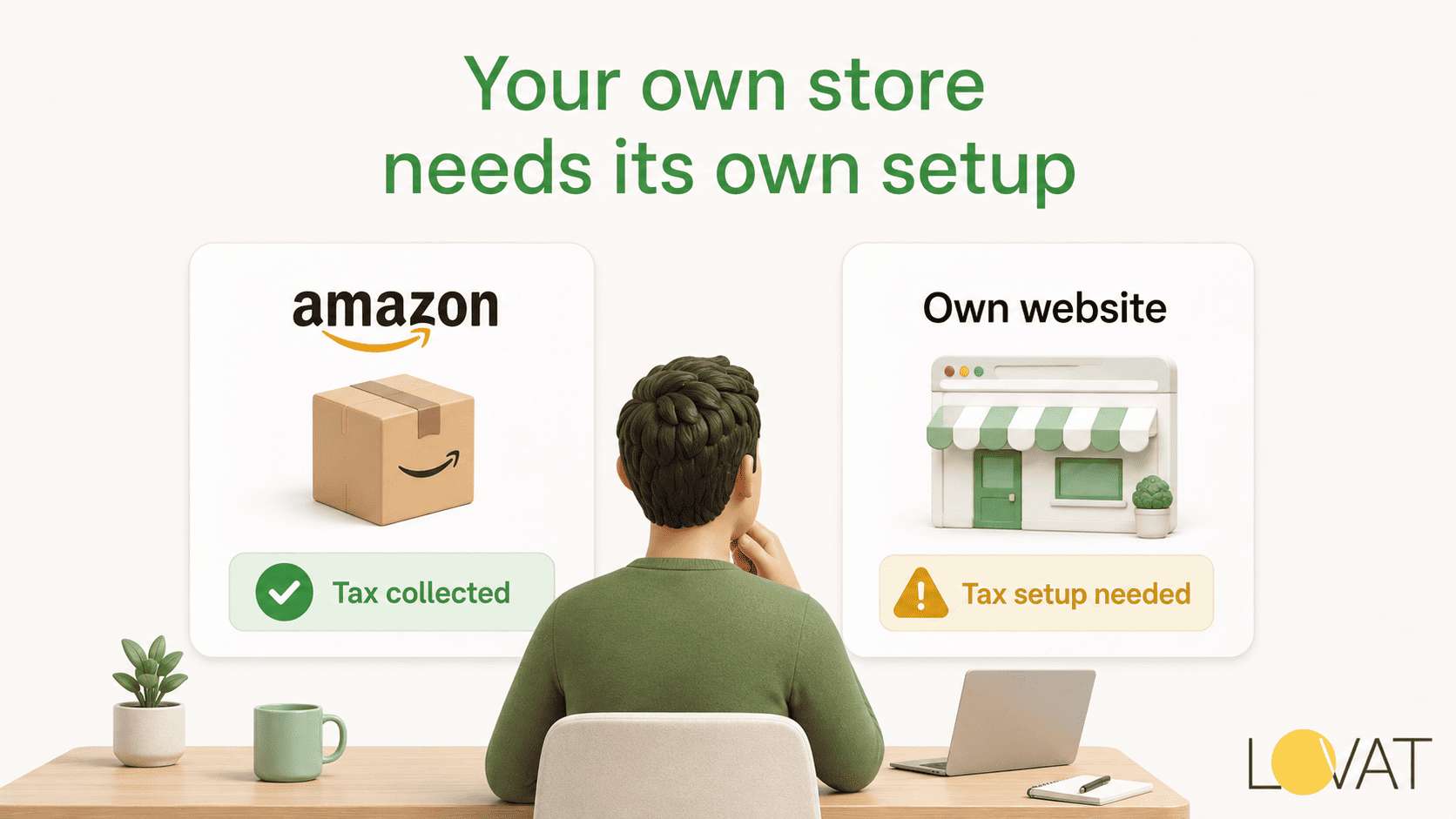

A trader running the same stock on eBay and on a personal store needs to split these two income streams with care. eBay’s system only covers eBay orders, and eBay sales tax never extends to a separate storefront. A standalone store needs its own setup, and the two will never reconcile on their own.

This gap shows up often during reviews. A merchant assumes the company already covers everything, without checking which channel actually processed which order.

Sales Tax Marketplace Facilitator Rules by State

Nearly every US state with a general sales levy has adopted a version of this rule. Limits, start dates and wording differ, so large traders should check guidance per jurisdiction rather than assume one rule fits all. Sales tax marketplace facilitator duty now touches nearly every state with a general levy, which is why a single national checklist rarely fits every business’s exact mix of regions.

| State group | Typical trigger | Platform handles |

| Large states (CA, TX, NY, FL) | $100,000 in revenue or 200 orders | Most third-party orders |

| Smaller states | Flat $100,000 revenue test | Facilitated orders only |

| States dropping order counts (UT, IL 2026) | Pure dollar test, no order count | Same scope |

| Local-only areas (AK boroughs) | Local test, often $100,000 | Local levy, not statewide |

A clear pattern stands out. Officials are dropping the old “200 order” rule in favour of a single dollar test, usually $100,000. Illinois follows this path from January 1, 2026, after Utah made the same move mid-2025. Tracking facilitator-driven duty by region this way is far simpler than treating each jurisdiction as a fresh research project.

Key Dates Worth Tracking This Year

Save this list. New limits often start at the new year or mid-year, and a missed date can mean a late scramble to register.

| Change | Date | Effect on sellers |

| Utah drops the order count test | July 1, 2025 | Only the $100,000 revenue test stands |

| Illinois drops the order count test | January 1, 2026 | Pure dollar test going forward |

| Alaska boroughs simplify limits | January 1, 2025 | Flat $100,000 gross revenue test |

| UK platform reporting fully live | Early 2026 | eBay, Etsy, Vinted must report seller data |

| EU low-value parcel duty starts | July 1, 2026 | New flat fee on most small imports |

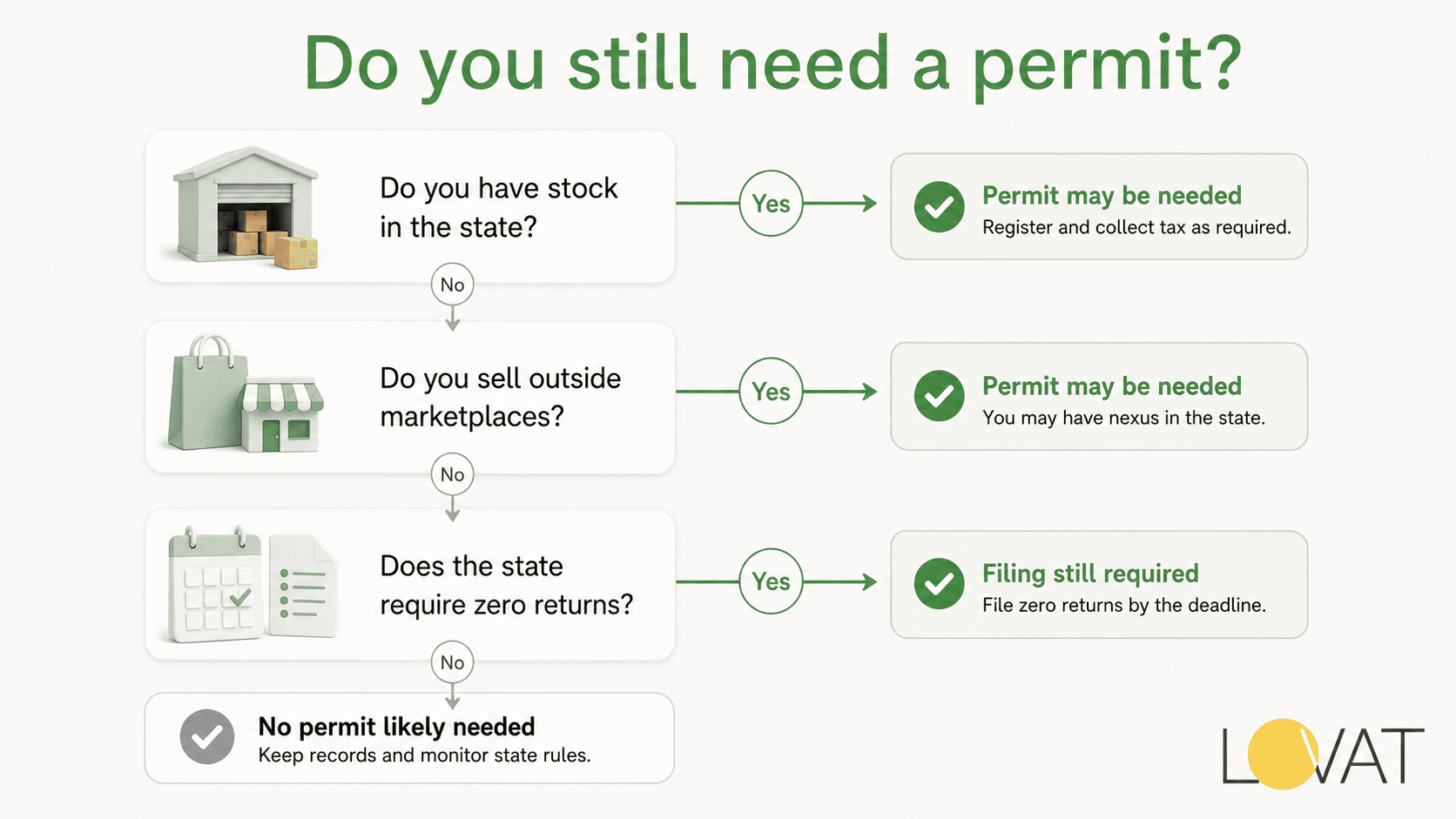

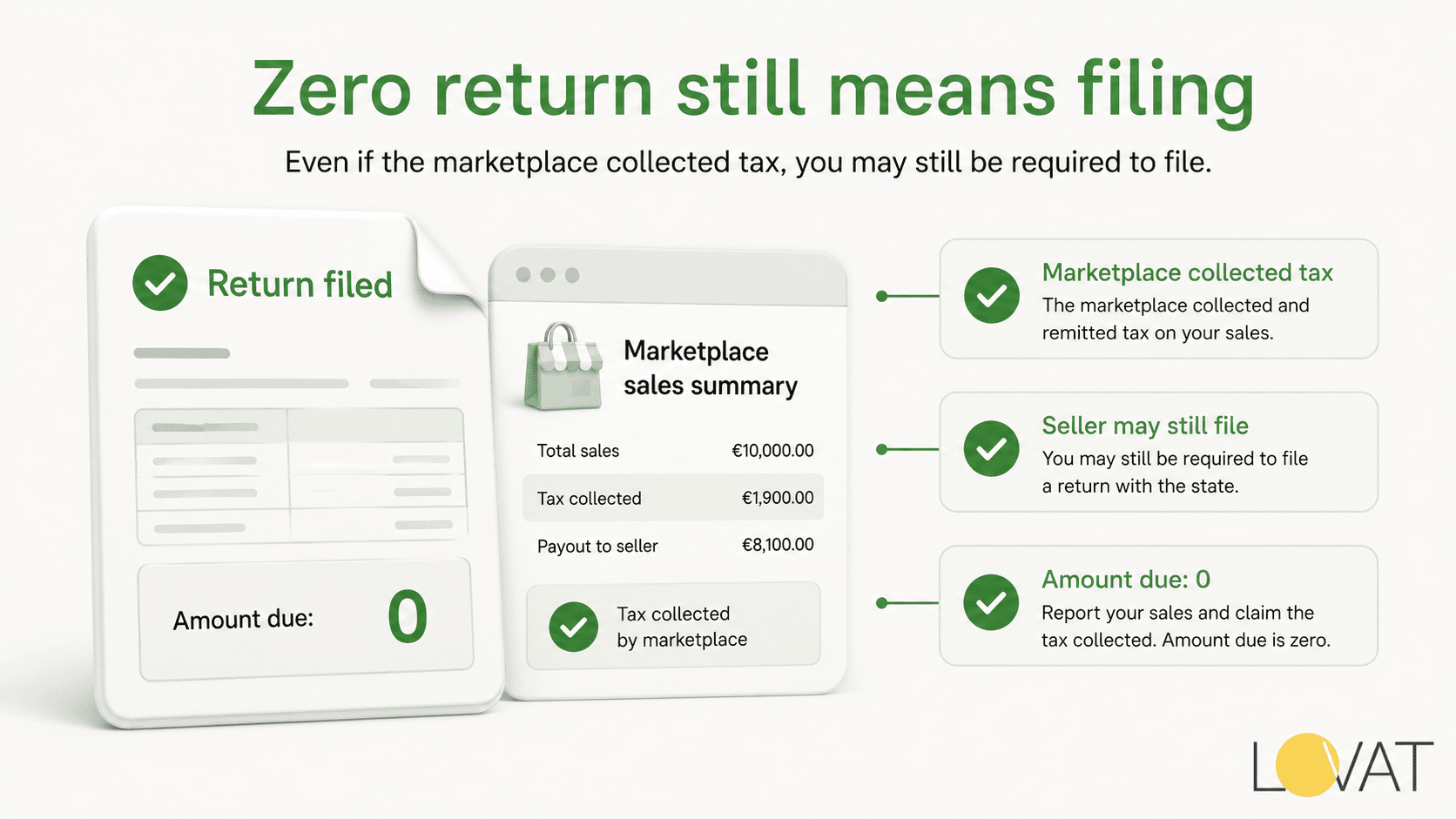

Do You Still Need a Sales Tax Permit

Often yes. The company shifts the collection step, not always the underlying paperwork.

Keep a permit active when any apply.

- You are based in the state, even if all orders run through a marketplace

- You hold stock there through a fulfilment scheme such as Amazon FBA

- You also trade direct through your own site or at shows there

- The authority asks for a “zero return” even when the site handled the charge

- You want clean, audit-ready bookkeeping across channels

Letting a permit lapse just because a company collects the levy is a common, fixable error. Tax offices do flag active merchants with no permit history.

What Marketplace Coverage Leaves Out

Platform coverage has real edges. Knowing the gaps stops business owners from assuming full cover when they have none.

- Your own website is never covered by Amazon, Etsy or eBay systems

- Wholesale orders placed outside the marketplace stay your own duty

- Income reporting and yearly filings sit apart from sales levy collection

- Trade shows and pop-up stalls are never marketplace-handled

- A few states exclude certain goods from the rule entirely

- Treat service coverage as one part of a wider plan, never the full plan

Comparing Amazon, Etsy and eBay Tax Handling

The pattern holds across all three companies. Checkout-level cover is strong for US orders placed in the marketplace. Anything sold elsewhere stays with the business owner.

| Feature | Amazon | Etsy | eBay |

| Auto US collection | Yes, all covered states | Yes, all covered states | Yes, all covered states |

| Digital item handling | Varies by class | Category-based logic | Limited digital sales |

| Merchant override | Not allowed | Not allowed | Not allowed |

| UK and EU reporting | Platform-level rules apply | Reports to HMRC since Jan 2024 | Reports live from 2026 |

| Off-platform orders covered | No | No | No |

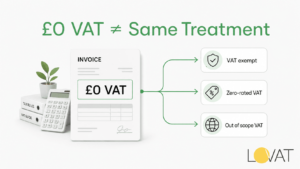

Tax on eBay Sales UK for Overseas Sellers

The UK runs a parallel scheme called the “deemed supplier” rule, which answers a common version of tax on eBay sales UK that trips up cross-border traders.

Under this scheme, HMRC treats the company, not the merchant, as the party charging VAT in two cases.

- Goods sent from outside the UK to a UK buyer, taxed at checkout

- Goods already stored in the UK by an overseas business, for example through FBA, no matter the price

An overseas trader using UK stock still needs a UK VAT number from day one, even though eBay charges the VAT at checkout. The trader’s task becomes filing accurate nil or deemed-supply returns.

VAT Duties for UK Based eBay Traders

For UK merchants shipping UK stock to UK buyers, eBay is usually not the deemed supplier. The trader stays liable for charging VAT once registered.

A UK number becomes mandatory once turnover passes £90,000 in any rolling 12 months. Traders get roughly 30 days to tell HMRC and begin charging VAT once they cross that line.

Apart from VAT, companies such as eBay, Etsy and Vinted must now send UK earnings data straight to HMRC under OECD-style reporting. This starts once a trader passes 30 sales or about £1,750 in a year. Reporting income is not the same as charging VAT, but the two now overlap heavily for busy resellers.

EU VAT Duties Layered on Marketplace Rules

EU rules copy the UK shape closely. Platforms act as deemed suppliers in two cases, low-value imports and EU-stored stock owned by a non-EU business.

From July 1, 2026, a flat fee lands on most small parcels entering the bloc, even those moved through the Import One Stop Shop. This shift touches a large share of cross-border orders and should sit in your pricing now, not after launch.

Need help mapping your EU duties before that fee starts. Book a free call with our team and we will walk through your setup.

Comparing US, UK and EU Marketplace Models

| Feature | United States | United Kingdom | European Union |

| Legal basis | State facilitator statutes | Deemed supplier VAT rule | Deemed supplier VAT rule |

| Trigger | Economic nexus limit | Import or UK stock by overseas seller | Import or EU stock by non-EU seller |

| Permit still needed | Often, based on presence | Yes, from day one with UK stock | Yes, depending on storage and OSS use |

| Platform reporting | Limited, region by region | Mandatory, OECD-based | Growing, DAC7-style |

A Compliance Checklist for Hybrid Sellers

Most growing shops trade across a marketplace and a direct store. A short list keeps that mix in check.

- List every channel you trade through

- Mark which channels already add a charge for you

- Check active permits exist wherever you hold stock or staff

- Split site-collected revenue from self-collected revenue in your books

- Set a quarterly note to review new threshold changes

This short list catches most gaps we find during onboarding calls.

Common Mistakes With Facilitator Coverage

A few patterns repeat across support tickets and calls, and most are easy to fix.

- Thinking marketplace coverage means no permit is ever needed

- Forgetting that a direct site is never covered by Amazon, Etsy or eBay

- Mixing service and self-collected revenue under one bookkeeping line

- Skipping a “zero return” where one is still due

- Ignoring new limits, such as Illinois dropping its order count rule in 2026

Fixing these early costs far less than answering a notice later.

Record Keeping Sellers Often Skip

The collection shift does not remove your own bookkeeping duty. Authorities still expect clear, exportable files in a few areas.

- Gross revenue by channel, split clearly

- Charge the company collected versus revenue you collected yourself

- Stock location history, mainly for FBA-style schemes

- Saved copies of site reports, stored off the marketplace

- Permit certificates and filing proof for each live jurisdiction

Most US states want these on hand for three to four years, and the UK asks for six years of VAT files. Losing access to a seller account should never mean losing your own paper trail.

Audit Risk and What It Can Cost

Risk has grown as authorities gain sharper data tools. Several now match platform reports against a merchant’s own filings and flag gaps on their own.

Costs vary by place, but one truth holds everywhere. Spotting a gap yourself almost always beats a notice from an office.

| Risk point | Likely outcome | How to lower it |

| Lapsed permit while still trading | Back charges plus interest | Keep permits live even with platform cover |

| Blended records across channels | Flags during review | Split bookkeeping by channel |

| Missing UK VAT with FBA stock | Backdated bill, possible account hold | Sign up before the first sale |

| Skipped reporting overlap checks | Mismatch versus your own filing | Check platform data each quarter |

Marketplace Facilitator Tax Compliance for Growing Sellers

Marketplace facilitator tax compliance looks automatic from a merchant’s seat, but the rules behind it shift often across states and countries. A company handling checkout collection does not register your business, does not file your zero returns, and does not watch new UK or EU shifts for you.

Real marketplace facilitator tax compliance means knowing exactly which permits stay active, which jurisdictions still expect a zero return, and which channels sit outside platform cover entirely. Staying on top of facilitator duties across several marketplaces is rarely a one-time setup task.

This is where a steady partner earns its place. We track threshold changes, UK deemed supplier news, and EU customs shifts as they land, so you skip checking fifty separate government sites on your own.

If your orders already span several states or countries, a quick review can catch gaps before an office does. Book a free consultation and we will check your setup together.

How Walmart and TikTok Shop Fit the Same Rule

Amazon, Etsy and eBay draw most attention, but the same logic covers Walmart Marketplace, TikTok Shop and most multi-vendor sites. Any company that lists goods, takes payment, and links buyers to third-party merchants tends to meet the legal test.

Shops running stock across five or six channels often find small gaps between sites in edge cases, even though the core duty stays the same. Checking each company’s own help page once a year is a smart habit, since wording and coverage shift as software updates roll out.

Digital Goods and the Taxability Question

Coverage gets harder once digital items enter the mix. Physical goods see fairly steady treatment everywhere. Digital downloads, software plans and online services see far less consistency.

Some places treat digital goods like physical ones. Others exempt certain digital classes. A few set a separate digital rate. This patchwork means a shop selling both physical stock and digital add-ons cannot assume one rule fits both.

Sites try to apply the right class automatically, but slips happen, mainly for bundles that pair a physical item with a digital key or warranty. Checking your product class inside each account twice a year catches most slips early.

International Sellers Entering US Marketplaces

Non-US shops joining Amazon, Etsy or eBay meet an extra layer, since the American system works very differently from VAT regimes most overseas business owners already know.

A few points surprise new entrants often.

- No single federal rate exists, since each state, and often each city, sets its own figure

- Nexus limits apply per jurisdiction, so a shop can owe money in one place and owe nothing next door

- A US permit, where needed, never replaces a home VAT or GST number

- Platform coverage does not remove the need to weigh US income reporting for the firm itself

Rules shift often, and last year’s setup may not match this year’s, as Illinois and Utah both show.

For shops moving from the EU or UK into American sites, treat the two systems as entirely separate. Trying to map one onto the other tends to cause the early errors we see most.

A Short Glossary Worth Saving

Keeping this short list straight makes every later chat with an accountant, a support agent, or a revenue office go far more smoothly.

| Term | Plain meaning |

| Economic nexus | A revenue limit that creates a duty with no physical footprint |

| Marketplace facilitator | A company that collects payment and a charge for a merchant |

| Deemed supplier | The UK and EU match, where a platform accounts for VAT instead of the seller |

| Zero return | A filing showing no money is due, often still required even with platform cover |

| Platform reporting (DAC7 / OECD) | Rules forcing companies to send seller income data to authorities |

Practical Steps Before Your Next Sales Tax Filing

A short pre-filing routine saves time and avoids late surprises. Run through these steps before each filing window closes.

- Pull a fresh report from each channel, not just your main store

- Match each company’s collected figure against your own bookkeeping line

- Flag any jurisdiction where your own permit needs a zero return this period

- Or note any new threshold change, such as the Illinois shift January 1, 2026

- Save a dated copy of each report outside the platform, in case access is lost later

Repeating this routine each quarter turns a stressful task into a short, known checklist.

Setting Up Tax Settings on Each Platform

Most merchants never open their own settings panel, since checkout cover feels automatic. A short look at each panel still pays off.

On Amazon, Seller Central shows a settings page where you confirm your home address and view collected figures by state inside reports, even though you cannot change the rate charged. Merchants asking how Amazon applies the charge on their orders should start with this same report, not a third-party tool.

On Etsy, shop owners can review category assignments per listing, which matters most for digital items. The way Etsy handles its checkout charge leaves little room for manual adjustment outside that listing-level class.

On eBay, the Payments tab shows the figure collected per order, useful for matching against your own books at filing time. Checking how eBay applies its charge inside that same tab avoids guesswork later.

When to Handle Filing Yourself and When to Bring in Help

Some shops can run their own filings for a while. Others reach a point where outside help saves more than it costs.

A short review with a specialist, even once a year, often pays for itself by catching one missed permit or one wrong zero return before an office does.

| Situation | DIY often works | Outside help often pays off |

| One state, low volume, marketplace-only orders | Yes | Not yet needed |

| Stock held in two or more states | Maybe, with strong records | Often worth a review |

| Selling into the UK or EU with stored stock | Rarely | Yes, deemed supplier rules are easy to miss |

| Mixed platform and direct-site revenue | Maybe, with split books | Worth a check at scale |

| Past notice or late filing on record | No | Yes, fix the gap before it grows |

Seasonal Factors That Affect Filing

Sales fee holidays, end-of-year volume spikes, and platform fee changes can all shift what a filing period looks like. A few seasonal notes worth a calendar entry.

- Some states run short relief windows on items like school supplies or clothing, which briefly change what counts as taxable

- Holiday volume spikes can push a business past an economic nexus limit mid-quarter, triggering a new duty sooner than planned

- Some platform fee or policy updates might land just before peak season, so check settings in early autumn, which avoids late surprises

Year-end is the right time to confirm every active permit is still needed, and to close out any jurisdiction where trading has stopped.

Building these checks into a yearly calendar keeps compliance steady, rather than reactive.

Sample Workflow for a Multi Platform Seller

A worked example often helps more than another list. Picture a shop selling home goods on Amazon, Etsy and a Shopify store, with stock split between a home state and one Amazon FBA hub elsewhere.

In the home state, the shop holds a permit and files a return each period, since presence there is clear. In the FBA state, the shop also holds a permit, even though Amazon collects the checkout charge there, since stored stock alone creates a duty in most places. Amazon and Etsy both handle checkout collection for their own orders. The Shopify store does not, so the owner sets rates there, matched to each state where a permit is active.

Each quarter, the shop pulls a report from all three channels, splits platform-collected money from self-collected money, and checks both totals against active permits. Where a state shows marketplace-only orders and a zero return is due, the owner files that return rather than skipping it. This one habit, repeated each quarter, is the single biggest gap-closer we see across hybrid businesses.

The same shop, once it starts shipping to UK and EU buyers, adds a second layer. UK orders sent direct from the home state fall under the deemed supplier rule if a marketplace handles the sale, but a direct Shopify order to a UK buyer does not get that cover. The owner needs a UK VAT number once turnover crosses the threshold, regardless of how the US side is set up. EU orders follow the same split, with IOSS covering low-value imports sold through a registered scheme, and local stock rules applying wherever goods sit inside the bloc before sale.

This layered view, one column per country, one row per channel, is the clearest way we have found to keep a growing, multi-platform shop audit-ready without drowning in separate rulebooks.

Closing Notes on Ongoing Support

Marketplace facilitator laws solved one problem for merchants, checkout-level collection, while opening another, knowing where your own duty starts again. The safest path treats platform cover as one part of the plan, then builds permits, books and filings around the gaps left open.

A useful way to frame this for a team or a co-founder is to split the business into two columns on a single page. One column lists every channel that already adds a charge for you, Amazon, Etsy, eBay, and any other covered marketplace. The other lists every channel that does not, your own site, wholesale deals, trade shows, and direct invoices. Anything in the second column needs its own rate setup, its own filing calendar, and its own review each time a new state or country enters the mix. Anything in the first column still needs an active permit wherever presence, stock or other channels apply, even though the platform handles the actual collection at checkout.

Revisiting that two-column page once a quarter, alongside the checklist earlier in this guide, keeps most growing businesses ahead of new threshold changes rather than reacting to them after a notice lands.

If you trade on Amazon, Etsy, eBay or your own store and want a clear map of where you stand, our team can review your US, UK and EU position in one call. Schedule your free consultation or try our fee quote tool to see what ongoing support would cost.