Permanent Establishment Risk for Remote and Ecommerce Businesses

Permanent Establishment Risk for Remote and Ecommerce Businesses

A founder in Berlin signs one contractor in Warsaw to close a handful of deals. Nothing feels different for a year and a half, until Poland’s tax office sends a letter asking why the German parent never registered there at all. That letter is the endpoint of a concept most owners never learn until it lands on their desk: permanent establishment. It marks the moment a foreign government earns the right to tax a slice of your profit, with no branch, no subsidiary, and sometimes no visible footprint on the ground. Distributed teams, dropshipping brands, and subscription software providers now walk closer to that moment than they realize.

What follows breaks down how this concept works in practice, why the US, UK, and EU each read it a little differently, and which dates on the calendar deserve attention this year.

What Is Permanent Establishment for Remote and Ecommerce Businesses

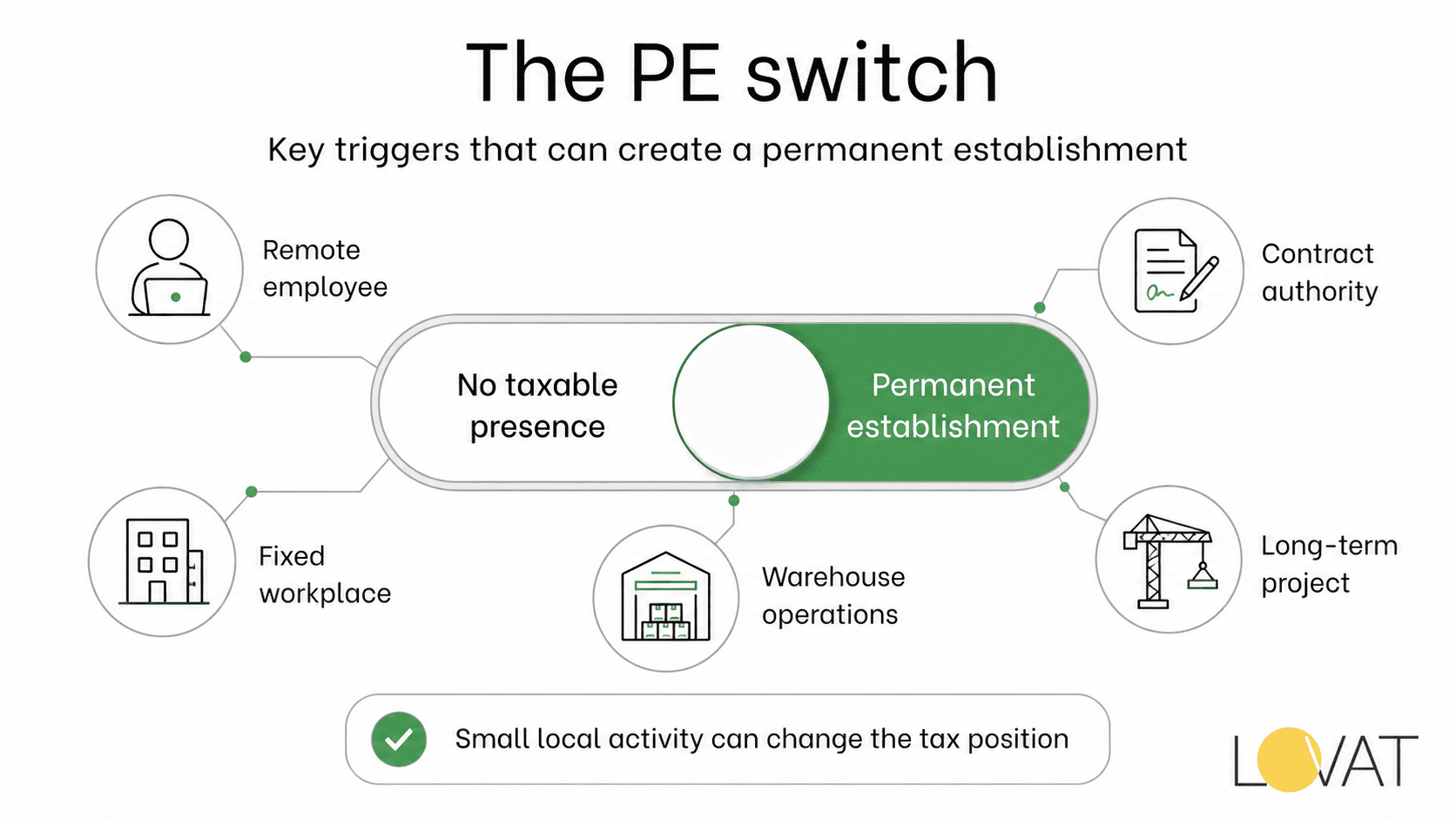

What is permanent establishment? Strip away the jargon, and it functions like a switch. Flip it, and a country you never incorporated in gains standing over a portion of your taxable earnings. The switch itself comes from the OECD’s Model Tax Convention, borrowed nearly verbatim by hundreds of bilateral treaties: a durable spot where a company conducts part of its work.

Several practical outcomes trail behind that single switch.

- Where tax lands depends on daily conduct, not a certificate framed on a wall

- One overseas hire, in unusual cases, can flip that same switch a full branch office would

- Zero physical footprint offers no shield to online sellers or SaaS providers on its own

- Treaty language, ahead of any single nation’s own tax code, generally settles whether the switch flips

Naming what is permanent establishment takes one sentence. Fitting that sentence onto a patchwork remote workforce takes far longer, since a new contractor or an extra storage arrangement can shift the outcome overnight.

Permanent Establishment Definition Under the OECD Model

Look inside Article 5 of the OECD Model Tax Convention, and you find the permanent establishment definition underneath most treaties written today. Its central clause paints a durable spot for conducting a trade, wholly or partly, sitting inside a border other than the company’s own.

A short roster of textbook examples sits alongside that clause

- A place of management

- A branch or an office

- A factory or a workshop

- A mine, an oil or gas well, a quarry, or a comparable extraction site

- A construction or installation job stretching past a full twelve months

A deliberate carve-out keeps certain footprints outside this permanent establishment definition. Goods parked purely for storage, display, or hand-off, plus supply purchases or market research run solely for a parent entity, both escape the switch as long as the work backs up the trade instead of forming its backbone. Base erosion reforms at the OECD trimmed that carve-out sharply, so a storage setup that once felt harmless might read very differently today.

Home Offices Under Current Permanent Establishment Rules

Few surprises hit founders harder than a scattered team logging in from different borders. New permanent establishment rules from the OECD, dated November 2025, tackle exactly that scenario, adding pages of commentary on staff clocking in from home offices abroad.

Two linked checks anchor that fresh commentary.

- A clock runs first. Log under half of a rolling year from an overseas home base, and a fixed place of business typically stays off the table on that measure alone

- A motive check follows, triggered only once the clock check fails. Tax offices then probe whether the company had any real operating reason to sit there, separate from an employee’s own choice of postcode

Parallel permanent establishment rules already steer reviews inside the UK, drawn from HMRC’s own manual and its set of worked scenarios covering remote and seconded staff. A holiday extended by a few weeks of work rarely clears the permanence bar, given how little about it looks settled. A pattern repeating annually in the identical role reads differently, since repetition itself starts to resemble a fixture. Teams scattered across borders fare better tracking where staff genuinely sit day to day, rather than what a contract happens to declare.

Dependent Agent Exposure for Online Sellers

Bricks and mortar are not the only doorway into this exposure. Treaties open a second one, built around people instead of premises, labelled a dependent agent.

- Two conditions, standing side by side, open that doorway. A person routinely holds, and puts to use, the power to sign contracts binding the foreign company inside a given border

- That person operates outside the role of an independent broker or commission agent running a separate business on standard terms

Online retailers and software vendors most often meet this through a local sales representative, distributor, or contractor who finalises deals directly rather than passing along a warm lead. A genuinely independent agent, splitting time across several unrelated clients on ordinary terms, rarely opens that doorway. A lone local contractor answering to just one company, holding sign-off power over its contracts, carries a much sharper permanent establishment risk than a genuinely independent partner ever would.

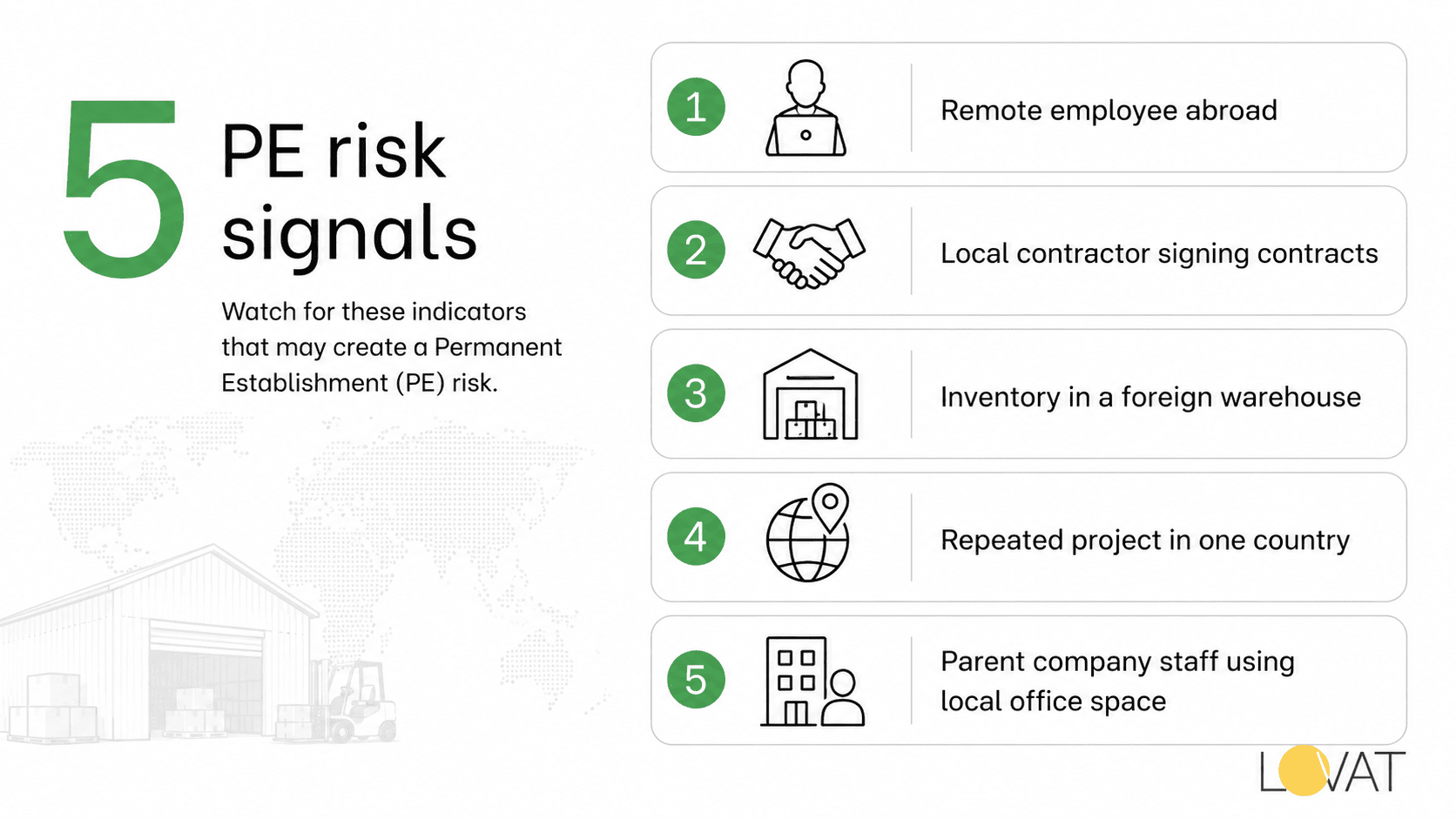

PE Risk Signals Behind a Growing Footprint

PE risk of this shape rarely announces itself through one loud event. It piles up through everyday, small-scale calls that eventually resemble a settled base overseas.

A scattered team is worth checking against this shortlist.

- A single remote hire clocking most of a year from one unchanged home setup

- An overseas contractor who closes contracts for the company as a matter of routine

- Inventory parked in a foreign warehouse beyond plain storage or a quick hand-off

- A short-term project abroad that drifts quietly into a yearly fixture

- Office space owned by a subsidiary used directly by the parent company’s own staff

No single line on that shortlist decides anything alone. Layered together across time, though, they nudge a company away from clearly safe ground toward a genuinely open question, and that flavour of permanent establishment risk almost always costs more to sort out once a notice has landed than it would to sort out beforehand. Groups running several country operations at once frequently carry more than a single one of these permanent establishments simultaneously, each judged on its own separate facts.

Permanent Establishment Tax Consequences and PE Tax Exposure

Cross that switch, and permanent establishment tax duties follow close behind. Article 7 of the OECD Model hands the host country standing to tax profit tied to that footprint, treating the local slice as its own distinct business trading at arm’s length with headquarters.

PE tax exposure reaches well beyond a single headline profit charge. Paperwork tied to PE tax slips through the cracks most at companies assuming a modest footprint means nothing needs filing at all. Many first hear about the shortfall only once a foreign authority writes in, and interest has generally been building by that point already.

Here is what a crossed threshold typically brings with it, spelled out rather than tucked into a short label.

- A corporate return normally falls due locally, even in years where the profit assigned to that footprint stays thin

- Only earnings traceable to the local slice face tax there, never the company’s full worldwide profit

- Payroll, VAT, or withholding duties can stack on top as a separate matter entirely

- Relief from double taxation demands an active, documented claim rather than a quiet assumption that a treaty will simply apply

None of that adds up to an automatic large bill. What gets attributed mirrors the real value a footprint contributes, and for a lone remote hire or a modest agent, that value often stays thin. A filing duty still holds regardless of size, and a missed permanent establishment tax return, far more than the underlying setup itself, is usually what draws a penalty notice.

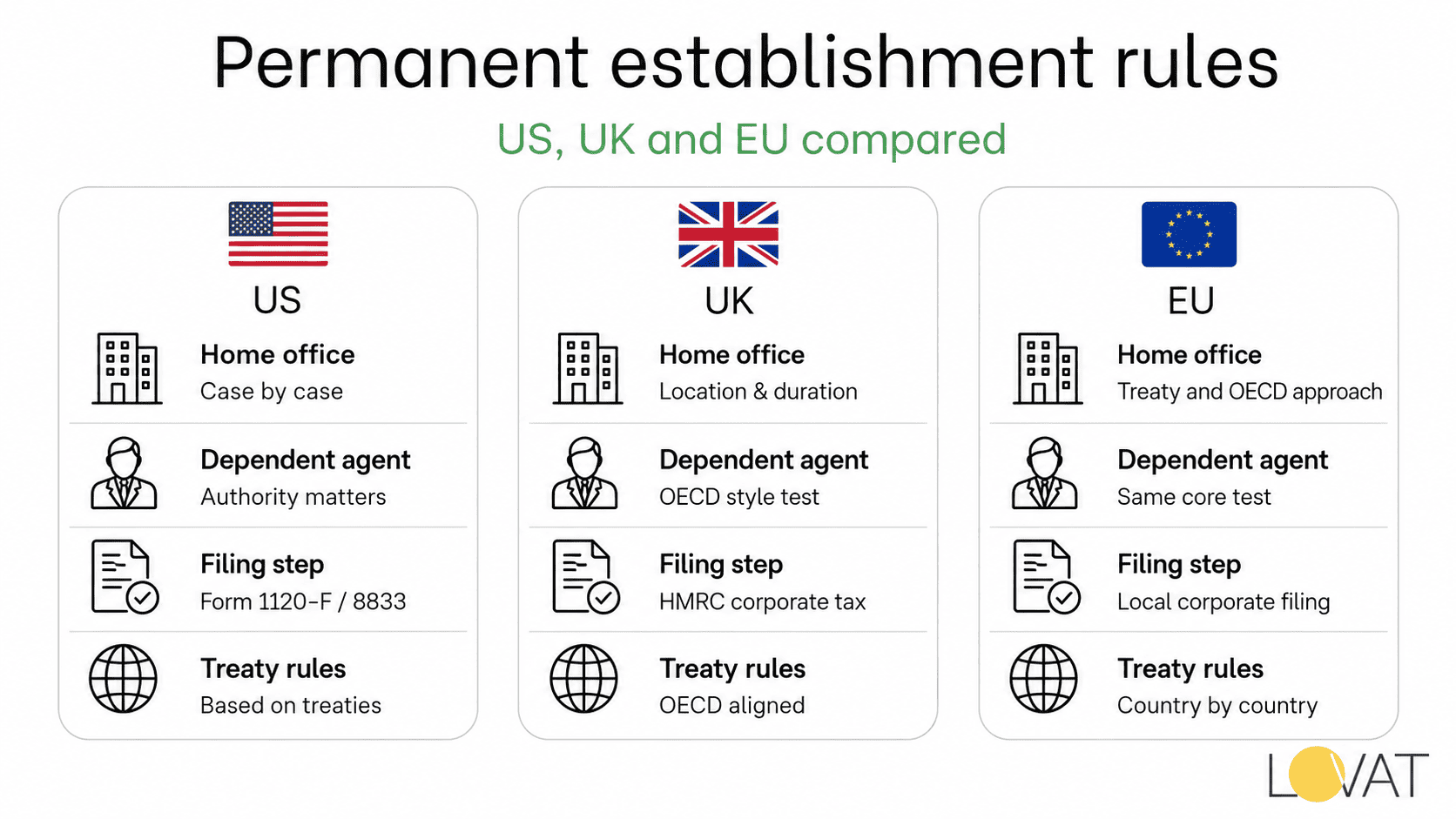

Comparing PE Rules Across the US UK and EU

Wording diverges country by country even while every jurisdiction nods toward one shared OECD source.

| Feature | United States | United Kingdom | EU member states |

| Legal footing | Treaty PE running beside a domestic “trade or business” test | Statute at CTA 2010 s.1141, echoing treaty phrasing | National statutes tied back to the OECD Model, each country its own way |

| Home office bar | Weighed case by case, with no set percentage anywhere | A degree-of-permanence test, again with no set percentage | Tracks the 2025 OECD update wherever a treaty points there |

| Dependent agent bar | Habitual contract authority, independent agents carved out | Same test, rooted in OECD language | Same test, rooted in OECD language |

| Filing step | Form 1120-F, treaty stance claimed through Form 8833 | Corporation tax sign-up handled through HMRC | Local corporate sign-up, details shifting by country |

A foreign company can sit fully inside a US trade or business test under domestic law while still dodging real US tax on those earnings, provided a treaty applies and the right stance gets filed on time. Skipping that single filing step is a frequent, easily corrected slip, and it has nothing to do with whether any PE tax was genuinely owed in the first place.

Key Dates Worth Tracking This Year

Pin this short table somewhere visible. Guidance here shifts nearly every year, and a read that held twelve months ago may no longer carry over cleanly.

| Change | Date | Effect on businesses |

| OECD signs off on updated remote work commentary | November 19, 2025 | A new two-step home office test drops into Article 5 |

| Refreshed OECD Model text reaches print | Expected 2026 | Formal wording folds the new commentary directly in |

| HMRC’s nomad worker guidance keeps running | Ongoing, INTM264435 | Five worked scenarios continue guiding UK reviews |

| US Form 1120-F and treaty stance filings come due | Annual, tied to calendar or fiscal year end | Protective filings still apply even where no PE gets claimed |

A Compliance Checklist to Lower Exposure

A brief internal sweep, run once a year, catches most PE risk long before a foreign tax office does.

- Chart every country holding a remote employee, a contractor, or stored goods

- Track the share of working hours each remote hire actually logs in that country

- Verify whether any local contractor closes deals on the company’s behalf as routine practice

- Confirm which treaties genuinely apply, and whether any stance calls for an annual filing

- Keep preparatory or auxiliary work abroad clearly apart from the company’s core revenue work

Wiring this sweep into a standard quarterly finance review keeps the picture live rather than something checked only after trouble starts.

Not sure where your remote team already stands. Book a free consultation and our team will map your setup country by country.

Common Mistakes That Create an Unplanned Footprint

A short set of habits keeps resurfacing across the businesses we work alongside.

- Reading “no office” as proof of “no exposure,” while a long-running remote hire goes unchecked

- Letting a short-term project abroad slide quietly into a yearly routine without a second look

- Recasting a foreign warehouse as active management the moment local staff start handling orders themselves

- Skipping a protective treaty filing on the assumption that no tax was owed anyway

- Folding VAT registration duties together with corporate permanent establishment duties, two matters with little in common

Catching these early, through a proper VAT registration or sales tax registration check where it fits, runs far cheaper than answering a foreign notice years down the road.

Closing Notes on Managing This Risk

Cross-border hiring and ecommerce both raced ahead of most tax treaties years back. The OECD’s 2025 home office update shows regulators finally catching that pace, with further work on remote employment, transfer pricing, and payroll tax due to land through 2026.

Treat every new remote hire, every contractor abroad who sticks around, and every stored inventory deal as worth a short look, not a safe guess. Businesses that check their footprint each quarter rarely stumble into a surprise filing. Businesses that wait for a letter instead usually end up paying well past the original tax bill, once interest and back filings stack on top.

If your team already spans several countries, a short review can confirm your position before a tax office raises the question first. Schedule a free call with our compliance team, or explore our tax academy guides for more on cross-border registration.