A Complete Guide Introduction to DAC 7

A Complete Guide Introduction to DAC 7

Introduction to DAC 7

DAC7 Thresholds Basics and DAC 7 Practice in the EU

| Rule element | Value under DAC7 (EU) |

| Transaction threshold | More than 30 transactions per calendar year |

| Value threshold | More than EUR 2,000 in consideration |

| Activities without thresholds | Real estate rental, services, transport |

| First EU reporting period | Transactions from 1 January 2023 |

| First unified deadline | 31 January 2024 |

This table reflects the basic logic of the DAC7 thresholds and helps C-level teams quickly compare DAC7 EU requirements with local jurisdictions that have implemented similar rules.

How DAC 7 reporting requirements change platform management

Regional DAC7 EU and EU DAC 7 Framework for Marketplaces

| Country / regime | Legal basis | Start of transaction tracking | First reporting year | First filing deadline | Threshold specifics |

| EU (dac7 EU) | dac7 directive | 1 January 2023 | 2023 | 31 January 2024 | 30 transactions or EUR 2,000 for goods; no thresholds for services/rentals |

| Australia (SERR) | OECD MRDP | 1 July 2023 (rideshare & accommodation), 1 July 2024 (other platforms) | 2023–24 / 2024–25 | 31 January or 31 July; key full-scope deadline: 31 January 2025 | No transaction/value thresholds; depends on activity type and seller status |

| Canada | OECD MRDP | 1 January 2024 | 2024 | 31 January 2025 | Canada’s regime officially recognised by the EU as equivalent to DAC7 |

| New Zealand (DPI) | OECD MRDP | 1 January 2024 | 2024 | 7 February 2025 | Focus on services and rentals; goods module not yet fully implemented |

| United Kingdom | OECD MRDP + UK regs 2023 | 1 January 2024 | 2024 | 31 January 2025 | Thresholds defined through small-seller exceptions; structure similar to EU DAC 7 |

India, Singapore, and Switzerland: Approaches to DAC7 Thresholds,

India

India does not yet have a unified regime fully analogous to the DAC7 thresholds. Instead, the government is strengthening regulation of platform labor and discussing taxation of digital platforms as part of tax reforms and BEPS. Research on digital platform taxation in India and new labor codes emphasize worker protection and income distribution, but do not introduce a direct equivalent to DAC 7 marketplace reporting.

For C-level teams at global marketplaces, this means that in India, monitoring labor laws and tax regulations is more important than following a copy of the DAC 7 thresholds, although general principles for transparently reporting platform sellers’ income are already being discussed.

Singapore

Singapore has traditionally been quick to adapt international tax transparency standards, but has not yet introduced its own version of the DAC 7 thresholds for marketplaces. The country’s focus is on country-by-country reporting for international groups and a separate law on platform workers, the Platform Workers Act 2024, which covers protections for couriers and drivers, rather than information reporting for sellers similar to DAC 7.

At the same time, Singapore’s tax authorities closely follow the OECD model rules for platforms. This is evident in their active participation in the global agenda and the structure of their digital economy analysis in relevant reports. For companies that have already implemented DAC7 thresholds in the EU, scaling the approach to Singapore assets is done through the general principles of the MRDP, rather than through a direct reference to the DAC7 Directive.

Switzerland

Switzerland has not yet implemented its own regime similar to the DAC7 thresholds for marketplaces. However, new VAT rules are important for platforms. According to them, from January 1, 2025, marketplaces are recognized as suppliers of goods in their own right in certain cases, even if they only operationally connect sellers and buyers.

Swiss divisions of international groups fall under the DAC7 EU if the platform works with EU sellers, and the exchange of information on digital platforms is initiated through automatic exchange agreements. Therefore, the EU DAC7 thresholds indirectly affect Swiss structures, although local law does not yet replicate the EU DAC7.

How DAC7 Marketplace Reporting Impacts Global Platform Design

Even when a country does not formally adhere to the DAC7 Directive, C-level teams see that the DAC7 marketplace reporting approach is gradually becoming a global standard. Australia, Canada, New Zealand, and the UK are already using the OECD model rules, and the EU, through DAC7 EU, has specified thresholds and deadlines.

The practical effect is clearly visible at three levels of the DAC7 thresholds.

Data Architecture

Unified seller identifiers, activity type classifications, and minimum threshold counters are needed for the EU and countries using the MRDP.

Operational Processes

Seller due diligence, as required by the DAC7 reporting requirements, must be integrated into onboarding, payments, and support to avoid manual data collection at the end of the year.

Deadline Management

Specific dates (January 31, March 31, February 7, July 31, and others) appear on the C-level team calendar, and internal milestones for DAC7 thresholds and similar regimes are linked to them.

This approach helps view DAC7 marketplace reporting not as a local European issue, but as part of an overall multi-year program for tax transparency of digital platforms.

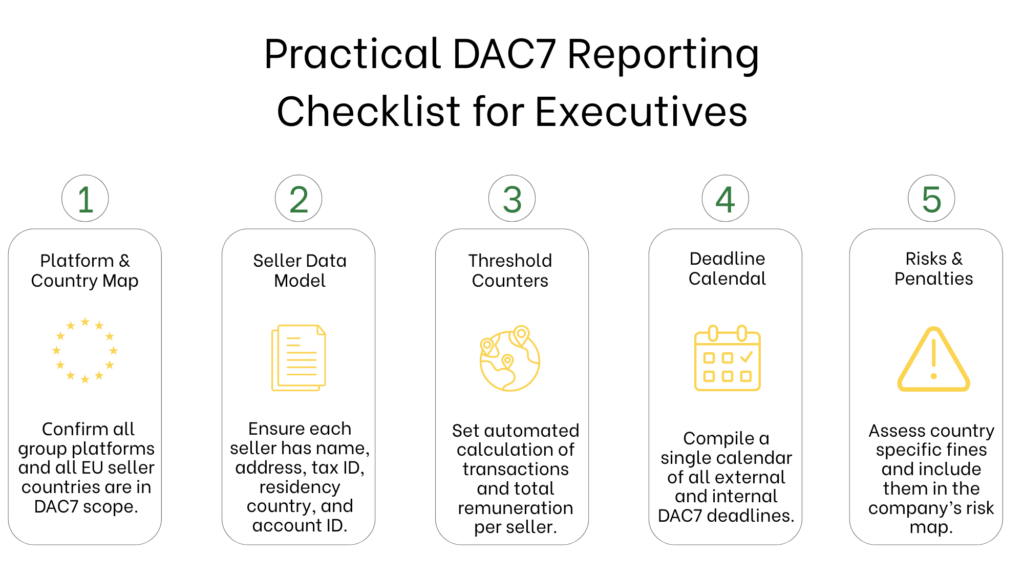

C-level checklist for updating processes for DAC7 reporting requirements

Jurisdiction Map

C-Level Responsibilities

Unified Data Model

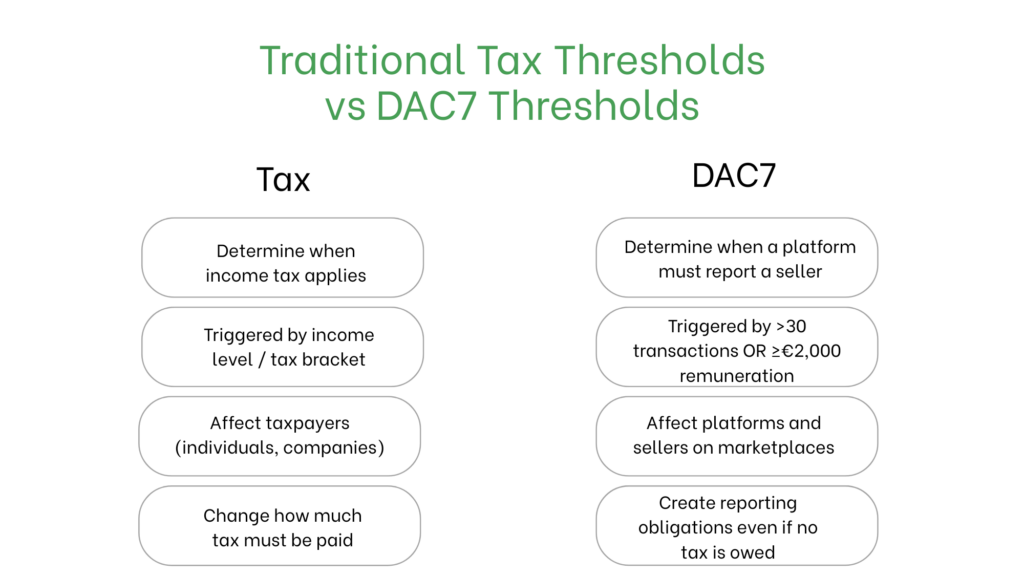

How DAC7 Thresholds Relate to Traditional Tax Thresholds

- Data used for applying national tax thresholds (income tax, VAT, etc.); and

- DAC7-specific counters that determine when a seller becomes reportable under marketplace reporting regimes.

Deadline Calendar

Risk Reassessment

Development Plan

In summary

Frequently Asked Questions

Which sellers are subject to DAC7 thresholds in the EU

A seller of goods becomes reportable if they conduct more than 30 transactions or receive at least €2,000 in revenue on a single platform within a calendar year. For services, real estate rentals, and transport, there are no numerical thresholds under the EU DAC7 and EU DAC 7 requirements; reporting begins with the first relevant transaction.

What data must platforms collect in accordance with the DAC 7 reporting requirements

Platforms must collect the seller’s name, address, country of residence, taxpayer identification number, bank or account identifier, as well as the total remuneration amount and the number of transactions per quarter and per year. These fields are used for both DAC 7 marketplace reporting and for internal control.

Which sellers are subject to DAC7 thresholds in the EU

What data must platforms collect in accordance with the DAC 7 reporting requirements

Are DAC7 thresholds displayed in the submitted report file

No. The platform filters sellers by DAC7 thresholds before generating the file. The DAC 7 reporting requirements for the platform itself only include sellers already identified as covered and their aggregated data. How does DAC 7 impact non-EU platforms?

If a non-EU platform has EU-resident sellers or real estate located in the EU, it may be covered by the DAC7 EU Directive. In this case, the group typically establishes a single reporting entity in the EU and reports there, with tax authorities exchanging information with other Member States.

How do other countries relate to the DAC7 Directive

Australia, Canada, New Zealand, and the UK use regimes based on the OECD model rules, which are similar in spirit to the DAC7 Directive but have their own thresholds and deadlines. The EU DAC7 thresholds only apply within the Union, but many groups are aligning global data models with these rules.

What are the key reporting deadlines to consider

For the EU, the first major reporting deadline under the EU DAC 7 Directive was January 31, 2024, for 2023, with an extension to March 31, 2024, in some countries, such as Germany. For new regimes, the typical first deadline is January 31, 2025, or early February 2025, so C-level teams now track multiple fixed dates in a single calendar.

What should C-level teams focus on when reporting on the DAC 7 market

Three key aspects are important: a unified merchant and transaction data model, integrated due diligence and reconciliation processes, and a clear calendar linking DAC 7 thresholds, DAC 7 market reporting, and other MRDP-based regimes into a single management view.