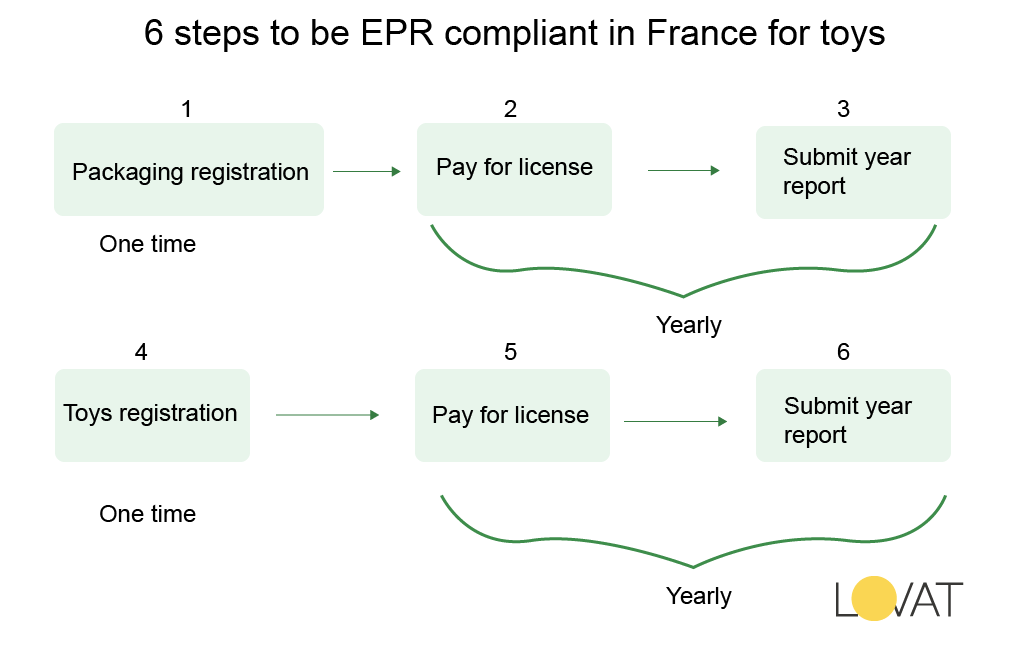

EPR in France (toys)

Who is considered by law to be a producer and/or marketer of toys?

Are considered as producer and/or marketer of toys, “all natural or legal persons who, in a professional capacity, either manufacture in France, or import, or assemble or introduce toys for the first time on the national market […] intended to be transferred against payment or free of charge to the end user by any sales technique whatsoever or to be used directly on national territory. If toys are sold under the sole brand of a reseller, the reseller is considered to be the marketer” (art. R. 543-320 of the Environmental Code).

As a producer and/or marketer, what are your new obligations?

Provide or contribute to the prevention and management of the resulting waste.

Adopt an eco-design approach.

Promote the extension of the lifespan of the said products as far as possible ensuring – for all the professional and private repairers concerned – the availability of the means essential for efficient maintenance.

Support reuse, reuse, and repair networks such as those managed by social and solidarity economy structures or promote integration through employment.

Contribute to development aid projects for the collection and treatment of their waste and develop the recycling of waste from products (art. L. 541-10.-I of the Environmental Code).

What products are affected by the games and toys EPR?

EPR applies to toys belonging to the following product families:

Toys, as defined in article 2 of decree no. 2010-166 of February 22, 2010, relating to the safety of toys. This article designates “products designed to be used, exclusively or not, for play purposes by children under fourteen years of age or intended for this purpose ”.

Models, puzzles, and board games.

The following are not concerned: writing or drawing articles as well as products covered by REP on electrical and electronic equipment (art. R543-320 of the Environmental Code).

Reporting period

Quarter for a year, “N” |

Reporting period |

Payment date at the latest |

| 1st quarter, from January 1st to March 31st N | April 1st to 30th | May 15 |

| 2nd quarter, from April 1st to June 30th N | July 1st to 31st | August 15 |

| 3rd quarter, from July 1st to September 30th N | October 1st to 31st | November 15th |

| 4th quarter, from October 1st to December 31st N | January 1st to 31st N+1 | February 15th N+1 |

Derogatory reporting regime:

By way of derogation, the contract provides for a simplified procedure with a single annual declaration. In this case, this declaration must be made either at the time of marketing or on a flat-rate basis.

Any company whose marketing is less than 15,000 pieces per year (subject to a total weight of less than 15 T) can benefit from the derogatory model. The marketer will determine, at the beginning of each financial year, his reporting methods: in real or on a flat-rate basis.

The marketer applies an annual flat rate of €220 per 1,000 pieces, without declaring these products’ category, weight, or material.

The declaration period for members eligible for the derogatory regime will be in January of the year N+1:

Month of declaration |

Payment date at the latest |

|

| From January 1st to December 31st N | January N+1 | February 15th N+1 |

To learn about EPR requirements in different countries, including registration thresholds, you can visit the page “EPR thresholds by country”.

Read more information about the EPR in France here.