South Korea E-invoice

Provinces

General

Provinces

General

About

General

About

General

General

General

Regulated by the National Tax Service (NTS) to ensure transparency, enhance tax compliance, and streamline business transactions. Mandatory for VAT-registered businesses, with phased implementation based on annual sales thresholds.

South Korea has been one of the early adopters of mandatory electronic invoicing, focusing on real-time transparency and digital tax reporting:

South Korea has been one of the early adopters of mandatory electronic invoicing, focusing on real-time transparency and digital tax reporting:

Implementation of mandatory e-invoicing in South Korea

South Korea has been one of the early adopters of mandatory electronic invoicing, focusing on real-time transparency and digital tax reporting:

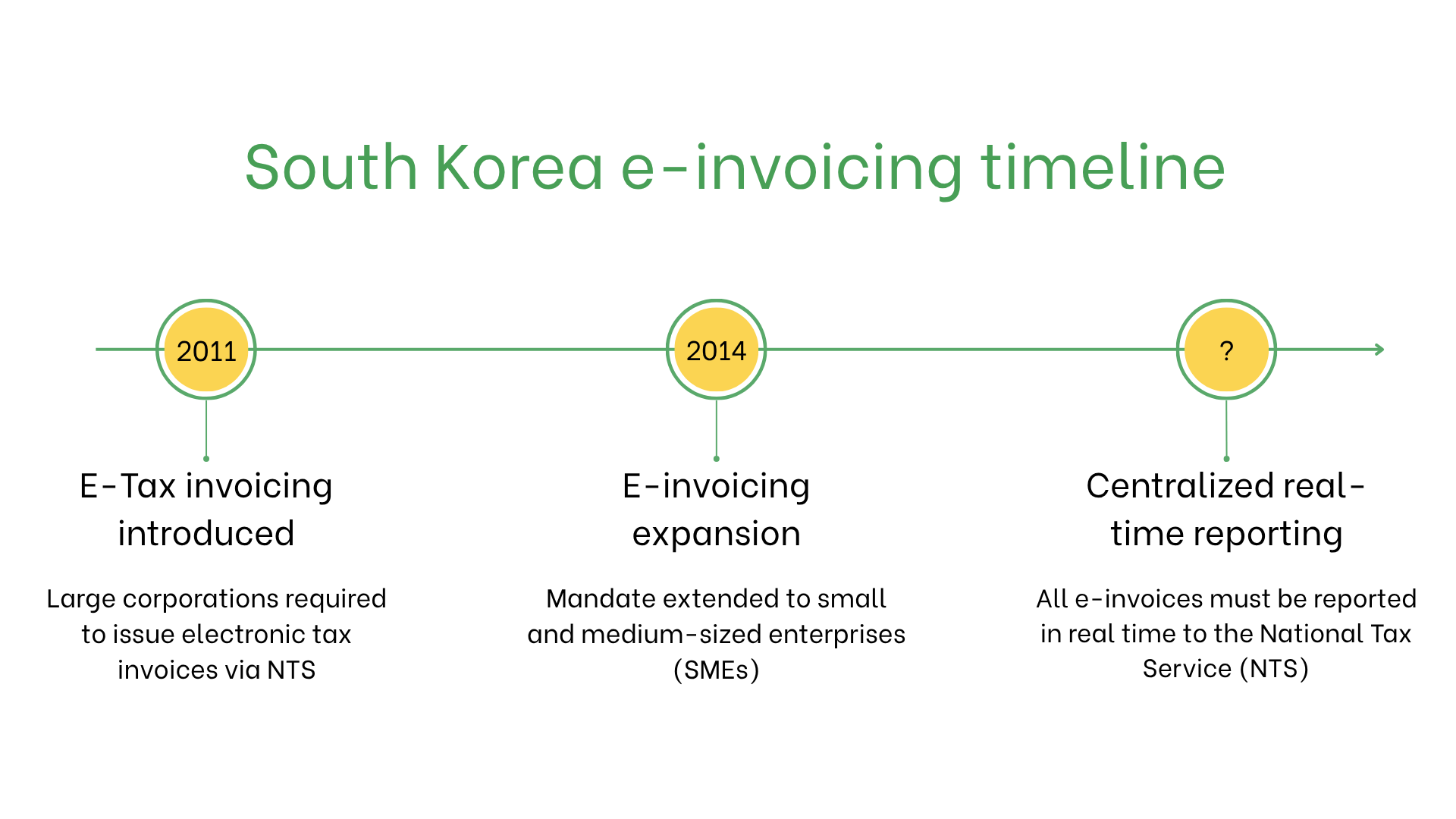

- January 1, 2011: South Korea introduced mandatory electronic tax invoices for corporations with annual sales exceeding KRW 3 billion. These invoices must be issued through a government-certified system and reported to the National Tax Service (NTS) in real time.

- July 1, 2014: The obligation was expanded to include small and medium-sized enterprises (SMEs). Now, all registered businesses are required to issue e-tax invoices for B2B transactions, regardless of size, ensuring wide adoption across the economy.

- Current system: E-invoices must be submitted to the NTS platform within one day of issuance. This applies to both issuance and receipt of invoices, and late or non-reporting may result in penalties. The system ensures near real-time visibility for tax authorities, enabling accurate VAT tracking and minimizing fraud.

Who needs e-invoices in South Korea?

- Large Enterprises: Businesses with significant turnover, mandatory since 2011.

- SMEs: Required based on turnover thresholds, phased in by 2014.

- Exporters: Required for cross-border transactions to ensure accurate VAT reporting.

- Non-Resident Businesses: Must issue e-invoices for transactions with South Korean entities if VAT-registered in South Korea.

E-Invoicing vs. E-Billing

| Aspect | E-Invoicing | E-Billing |

| Purpose | Compliance with Spanish and EU regulations | Informal or internal transactions |

| Validation | Real-time via FACe or SII platforms | Not validated |

| Format | Facturae XML | Flexible, non-regulated formats |

| Archiving | Mandatory for six years | Optional |

Key features of South Korea's e-invoicing system

- Submission Platforms: Invoices must be submitted via FACe for public sector transactions or SII for VAT reporting.

- Validation: The platform ensures compliance with mandatory fields, digital signatures, and VAT rules.

- Archiving: E-invoices must be stored electronically for 6 years in compliance with Spanish tax laws.

E-Invoicing dataset

- Buyer/Seller IDs: NIF (Tax Identification Numbers).

- Invoice Details: Invoice number, issue date, and payment terms.

- Goods and Services: Line-item descriptions, quantities, unit prices, and subtotals.

- Taxes: Applicable VAT rates and amounts.

- Transaction Info: Total payable amount, currency, and payment method.

- Delivery Details: Ensures authenticity and integrity of the invoice.

E-invoicing across transaction types

B2B Transactions- Mandatory for all VAT-registered businesses.

- Real-time e-invoicing ensures compliance, reduces errors, and facilitates VAT refunds for cross-border transactions.

- Not mandatory but encouraged for improved transparency and internal records.

- Required for suppliers to public entities via the NTS platform.

Penalties for non-compliance

- Fines: Up to €10,000 per violation for failing to meet public sector requirements.

- Operational Delays: Rejected invoices may lead to payment delays and strained client relationships.

- Legal Risks: Audits and reputational damage for repeated noncompliance.

Subscribe to the newsletter

No spam, only interesting news