Spain E-invoice

Provinces

General

Provinces

General

About

General

About

General

General

General

Update Notice – December 2025

Spain has officially postponed the mandatory implementation of certified B2B e-invoicing software (Verifactu system) to 2027. New deadlines:- January 1, 2027 – Companies subject to Corporate Income Tax

- July 1, 2027 – Self-employed individuals (autónomos) and Personal Income Tax taxpayers

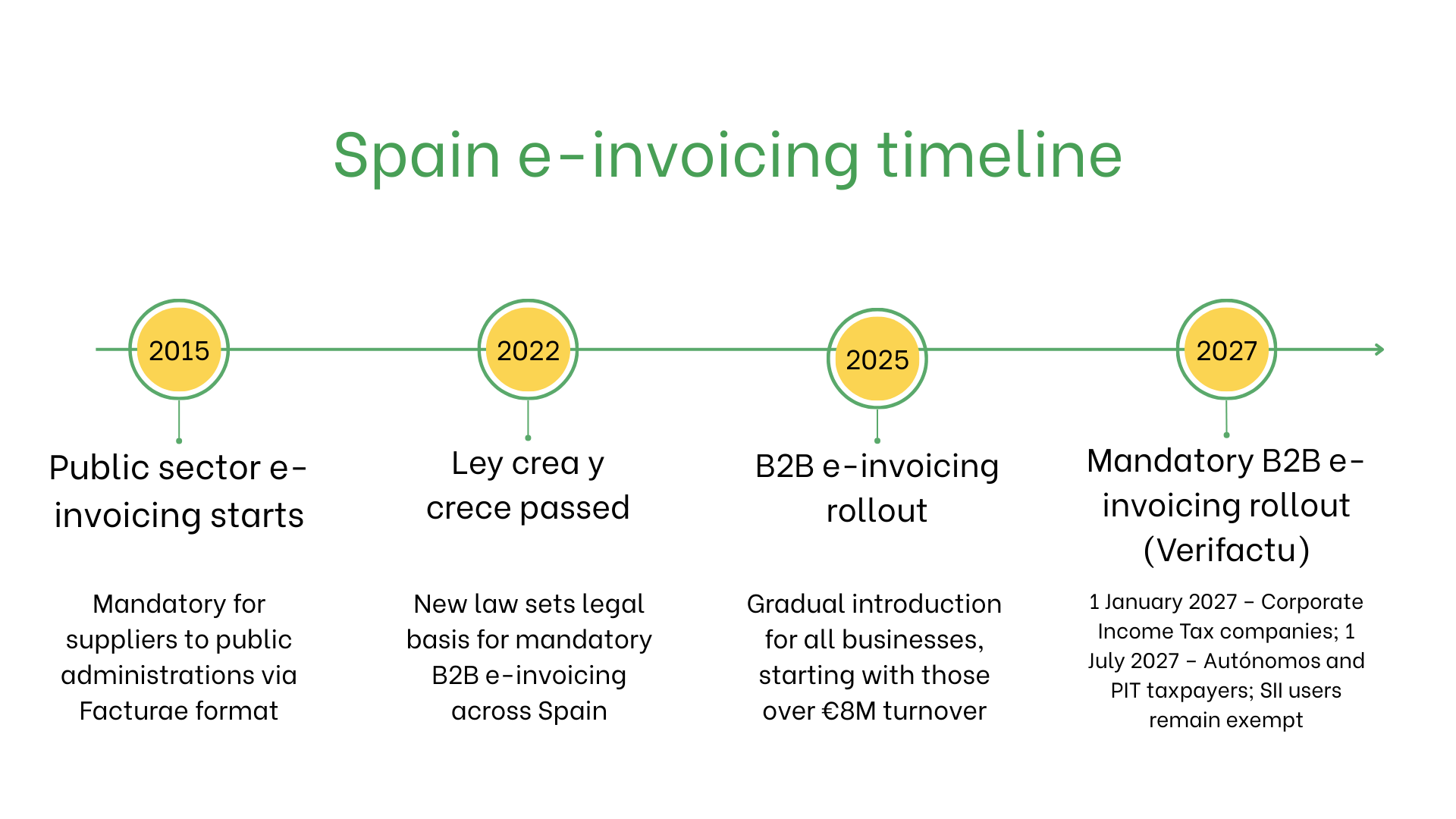

Implementation of mandatory e-invoicing in Spain

Spain is moving toward full-scale mandatory e-invoicing in both the public and private sectors, driven by national digitalization policies and alignment with EU standards:

Spain is moving toward full-scale mandatory e-invoicing in both the public and private sectors, driven by national digitalization policies and alignment with EU standards:

- January 2015: E-invoicing became mandatory for all suppliers to the Spanish public sector. Companies must use the government-approved Facturae XML format and submit invoices via the FACe portal (Punto General de Entrada de Facturas Electrónicas).

- September 29, 2022: The Spanish government approved the Ley Crea y Crece, a legislative reform to encourage business growth and combat late payments. A key element is the mandatory use of e-invoicing for all B2B transactions, applicable to all Spanish companies and freelancers.

- Starting 2025: Businesses with annual turnover over €8 million will be required to issue and receive structured e-invoices.

- Updated Deadline — Mandatory B2B e-invoicing (Verifactu system): Due to a government decree issued in December 2025, the obligation to use certified invoicing software connected to AEAT (Verifactu) has been postponed: January 1, 2027: For companies subject to Corporate Income Tax; July 1, 2027: For autónomos and Personal Income Tax taxpayers. Businesses already reporting invoices through SII remain exempt from Verifactu requirements.

Who needs e-invoices in Spain?

- Public Sector Suppliers: Required to issue e-invoices via FACe.

- Large Enterprises: Businesses with turnover > €8M will need to comply with the upcoming B2B e-invoicing mandate.

- Exporters: E-invoicing is mandatory for transactions involving cross-border VAT reporting.

- Non-Resident Businesses: Required to issue e-invoices for transactions with Spanish public entities if registered for VAT in Spain

E-Invoicing vs. E-Billing

| Aspect | E-Invoicing | E-Billing |

| Purpose | Compliance with Spanish and EU regulations | Informal or internal transactions |

| Validation | Real-time via FACe or SII platforms | Not validated |

| Format | Facturae XML | Flexible, non-regulated formats |

| Archiving | Mandatory for six years | Optional |

Key features of Spain’s e-invoicing system

- Submission Platforms: Invoices must be submitted via FACe for public sector transactions or SII for VAT reporting.

- Validation: The platform ensures compliance with mandatory fields, digital signatures, and VAT rules.

- Archiving: E-invoices must be stored electronically for 6 years in compliance with Spanish tax laws.

E-Invoicing dataset

- Buyer/Seller IDs: NIF (Tax Identification Numbers).

- Invoice Details: Invoice number, issue date, and payment terms.

- Goods and Services: Line-item descriptions, quantities, unit prices, and subtotals.

- Taxes: Applicable VAT rates and amounts.

- Transaction Info: Total payable amount, currency, and payment method.

- Delivery Details: Ensures authenticity and integrity of the invoice.

E-Invoicing across transaction types

B2B Transactions- Upcoming mandate will make e-invoices mandatory for all B2B transactions.

- Integrated with AEAT for real-time VAT reporting.

- E-invoicing is not mandatory for B2C transactions but is encouraged to enhance transparency and simplify tax reporting.

- Mandatory for all suppliers to public administrations via the FACe platform.

- Invoices must comply with Facturae standards and include a digital signature.

Penalties for non-compliance

- Fines: Up to €10,000 per violation for failing to meet public sector requirements.

- Operational Delays: Rejected invoices may lead to payment delays and strained client relationships.

- Legal Risks: Audits and reputational damage for repeated noncompliance

Subscribe to the newsletter

No spam, only interesting news