Reverse charge invoice for a buyer: 4 steps to be compliant

Reverse charge invoice for a buyer: 4 steps to be compliant

This article is for a business that receives an invoice with the note “reverse charge”. Because in such a situation obligation to calculate VAT is on the buyer and it can have serious consequences.

Reverse charge scheme – is a European approach to charge VAT on the destination principle (where the buyer is located). This method is used within the EU for B2B transactions only – where two contractors are both VAT-registered businesses. The use of reverse charge invoices helps avoid multiple registrations in countries where the customers are located. Because it is a business buyer needs to calculate VAT at destination principle.

- The first step you need to do when you received a reverse charge invoice is to calculate VAT on this invoice. General attitude: you use a standard VAT rate in your country apart from cases when you bought goods or services taxed at the reduced rate.

- The second step is to add this invoice to your VAT return as output VAT.

- The third step is to add this reverse charge invoice in your VAT return as input VAT.

- Forth step is optional you may need to indicate this amount in your Intrastat report.

Purchase of service from another country

General approach: A business buyer receiving an invoice from a service provider must follow the 4 steps we described earlier. But the more complicated case is when a buyer has multiple VAT registrations in the EU – which number should they use? The universal method is to use the main VAT number (where the place of establishment of the business). Exceptions might be the cases where the place of supply differs from the place of the buyer of the service. Such exceptional services might be cultural events or services connected to buyer property – for such kinds of services the place of supply is where the event takes place and VAT of this country should be charged.

For the majority of services, the place of supply is where the customer is, which means that the main VAT number of the buyer should be used for VAT accounting and reporting.

Purchase of goods from another EU country

When goods move from one EU country to another the place of supply for goods is the destination country – where goods are shipped. If your business has multiple VAT registrations you should use a VAT number of the arrival country. A buyer who has purchased goods in another country must calculate the VAT on these goods in the country of arrival at the normal rate applicable for sales in that country. And also follow those 4 steps that we mentioned earlier in this article.

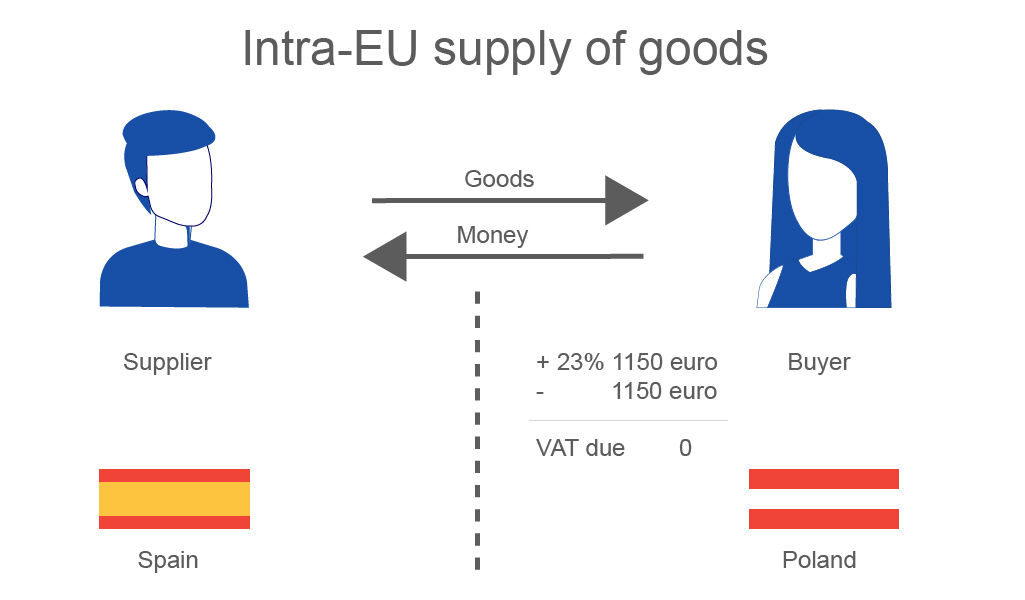

Example: UK established company with VAT registration in Poland bought goods from a Spanish supplier. Spanish supplier issued an invoice with the words “reverse charge” and the Polish VAT number of the buyer. I received a reverse charge invoice for 5000 Euro what should I do? Add this invoice to your tax records and calculate VAT on top of the invoice.

The Buyer needs to calculate Polish VAT 23%- 1150 Euro and fill this information into the Polish VAT return.

What will happen if a buyer didn’t calculate VAT on the reverse charge invoice?

In case a business doesn’t calculate VAT on its intra-community purchases, the Tax authority during a tax audit will do this. In this scenario, such a taxpayer couldn’t credit the same amount in their VAT return as it would be with a voluntary declaration. In this case, the company will have to pay additional tax accrued as part of the audit.