EU E-Invoicing Rules and Digital VAT Reporting for Businesses

EU E-Invoicing Rules and Digital VAT Reporting for Businesses

EU E-Invoicing Rules and Digital VAT Reporting for Businesses

A Berlin logistics outfit called Hellmann shipped pallets to a Lyon client last March. They sent the customary PDF invoice. Then they watched €18,400 freeze in receivables for 47 days. The PDF was no longer legal tender for that transaction. France had switched on Chorus Pro reporting. Unstructured documents fell out of scope overnight. Several finance teams discover this the painful way — a refund denied, a VAT credit frozen, or a fine from the Direction Générale des Finances Publiques.

Brussels has been quietly rewiring how taxable transactions move across the continent. The reform package called ViDA — VAT in the Digital Age — extends the EU’s earlier directive on e-invoicing. The original 2014 text was drafted for public procurement. What used to be a regional concern in Italy, Hungary, and Poland now reaches every importer. Even a SaaS startup with one EU buyer feels the shift.

Numbers tell the story. The VAT gap across member states hit €89 billion in 2022. Italy’s clearance model recovered around €4.1 billion in its first two years. Tax authorities have read those numbers. The direction is locked. By 2030, structured invoicing becomes the default for cross-border B2B flows. Continuous transaction controls sit on top of existing tax reporting rules across the EU.

Here is the practical map. You will see who enforces what. You will see where deadlines actually fall. You will see which file formats survive at the border. You will see where operational landmines hide. The piece skips buzzwords. If you sell into the EU, the new e-invoicing rules across Europe already touch your ledger.

Why the EU E Invoicing Directive Rewires Trade Across the Single Market

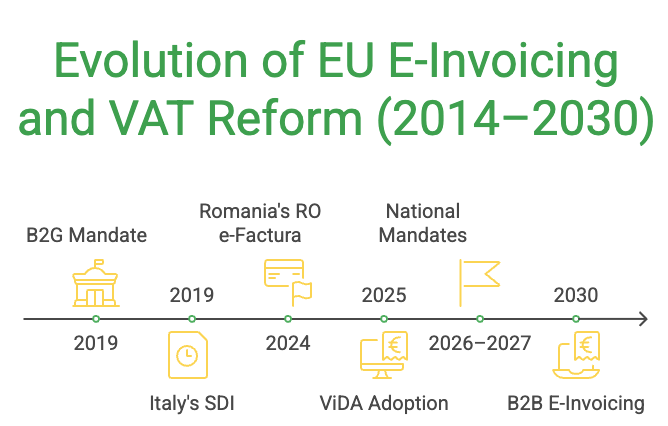

The eu e invoicing directive — formally Directive 2014/55/EU — started life as a procurement rule. Public buyers in every member state had to accept structured invoices from suppliers by April 2019. That was the warm-up. ViDA was adopted by ECOFIN in March 2025. It extends the same machinery into private commerce. It also introduces digital reporting obligations for intra-Community supplies.

Budget logic shaped the eu e invoicing directive from day one. Member states lose tens of billions each year to carousel fraud and missing-trader schemes. Under-reporting compounds the leak. Real-time clearance crushes those tactics. The tax authority sees the transaction before the buyer files a deduction. Italy went first in 2019. Hungary followed with RTIR. Spain rolled out SII. Each program tightened the screw.

That directive on e-invoicing now reaches well beyond procurement. A US software firm registered for VAT in Germany falls under the German invoicing mandate from January 2027. A Brazilian exporter to a Polish factory needs structured documents the moment KSeF goes live. Compliance is no longer a Brussels problem. It lands wherever you collect VAT.

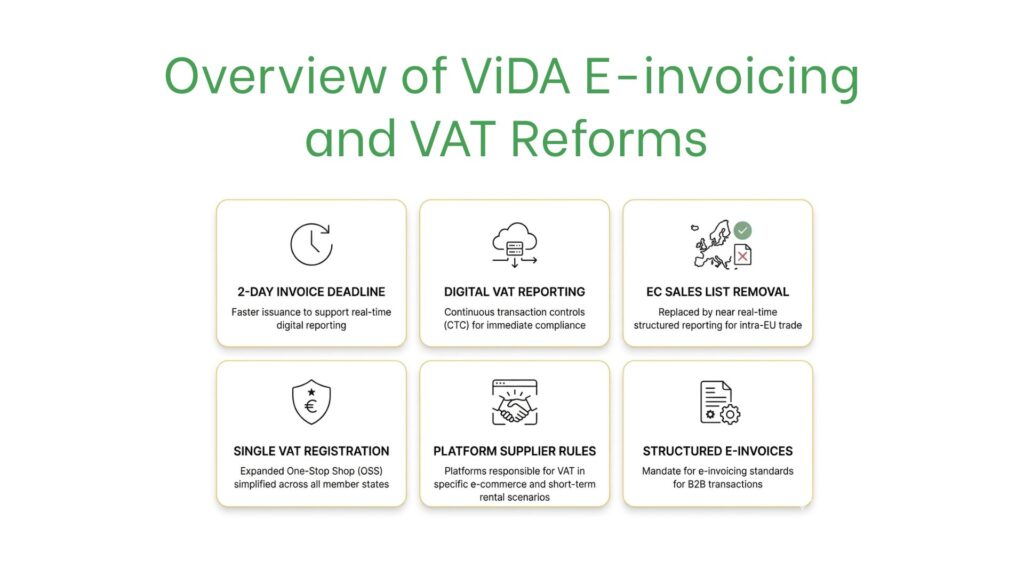

What ViDA actually changes:

- Mandatory structured invoices for intra-Community B2B by 1 July 2030, with member states free to mandate domestic e-invoicing without prior Commission approval.

- A two-day issuance deadline replaces the current 15-day window for cross-border supplies.

- Digital reporting replaces recapitulative statements, killing the EC Sales List as we know it.

- Single VAT registration for platform economy operators, sparing them dozens of national filings.

- Deemed supplier rules for short-term accommodation and passenger transport platforms.

- Removal of the optional summary invoice for cross-border B2B sales.

Country Snapshot for Electronic Invoicing Europe — Mandates, Formats, and Deadlines

electronic invoicing europe moves on different clocks. Italy lit the fuse seven years ago. Romania switched on RO e-Factura in 2024. Germany requires inbound capability from January 2025. Full issuance follows by 2027. France delayed its B2B mandate twice. The country settled on September 2026 for receipt and September 2027 for issuance. Spain’s Verifactu arrives in 2025. The broader B2B Crea y Crece law lands in 2026 and 2027.

Format fragmentation makes electronic invoicing europe messy at the technical layer. Italy uses FatturaPA over SDI. France adopts Factur-X plus UBL through PPF. Germany leans on XRechnung and ZUGFeRD. Poland will mandate FA(2) over KSeF. The European standard EN 16931 sits underneath all of them. But the syntaxes and channels diverge. A shared invoicing engine that handled FatturaPA last year now needs PEPPOL BIS, UBL 2.1, and CII too.

Border-spanning groups feel the strain first. A French retailer with a Polish DC and a Czech 3PL touches three different clearance models. Three different validation schemas pile on top. Mistakes cascade for cross-border e-invoicing in Europe. A single rejected file can stall a customs release. It can delay a tax credit. It can trigger an audit months later.

| Country | Mandate Live Date | Format and Channel | Penalty Bracket |

| Italy | January 2019 (B2B) | FatturaPA via SDI | €250–€2,000 per missing invoice |

| Germany | January 2027 (full B2B) | XRechnung, ZUGFeRD | Up to €5,000 per breach |

| France | September 2026 (receipt) | Factur-X, UBL via PPF | €15 per invoice, capped €15,000 yearly |

| Poland | February 2026 (B2B) | FA(2) via KSeF | Up to 100% of VAT amount |

| Romania | July 2024 (B2B) | UBL via RO e-Factura | RON 5,000–RON 10,000 |

| Spain | July 2025 (Verifactu) | Facturae, Veri*Factu | €10,000 fixed plus 1% of revenue |

Decoding the E Invoicing Requirements Europe Demands From Your Stack

The phrase e invoicing requirements europe sounds abstract until you hit your accounting system. A structured invoice is not a PDF with metadata. It is an XML or JSON payload. The payload carries every taxable line, every tax rate, every counterparty identifier. It also carries the unique reference number assigned by the clearance platform. Your ERP either generates that payload natively, or you bolt on middleware that does.

Most teams underestimate the integration burden e invoicing requirements europe places on their systems. The accounting team owns master data. The IT team owns connectivity. Procurement owns supplier onboarding. Each silo blocks the next. Projects that succeed treat the work as cross-functional from week one. Sometimes that means pulling a tax advisor into IT standups — which feels strange but pays off.

The reverse case bites too. A buyer that cannot ingest structured invoices from a German supplier risks losing the input VAT deduction. The deduction sits on the supplier’s filing. But the buyer must still prove receipt and validate the file. Both sides need working pipelines. Europe’s e-invoicing requirements operate as a two-way handshake, not a broadcast.

B2B, B2G, and B2C Scenarios Compared

B2G remains the gentlest path. Public buyers have accepted EN 16931 invoices since 2019. Validation tooling is mature. Transaction volumes are predictable. PEPPOL coverage is wide enough that most ERPs handle it natively. Friction shows up at small subnational entities. A Czech municipal hospital may still ask for PDFs over email. That is where Europe’s e-invoicing requirements bump against everyday operations.

B2B is where the rules harden quickly. Real-time clearances, two-day deadlines, and 10-year archive obligations. Bilateral mutual recognition. In 2026, a Dutch wholesaler invoicing a Polish retailer will have to check against KSeF schemas. The wholesaler must store proof of acceptance. They must also reconcile with their own ledger. The e-invoicing requirements covering European B2B trade leave very little room for improvisation.

B2C sits at the edge for now. Most member states have not extended structured invoicing into retail. ViDA carves out a path though. Voluntary B2C reporting comes first. Mandatory adoption follows for high-risk sectors. Hospitality, short-term lets, and ride-hailing already feel the pull through deemed-supplier rules introduced for platforms. Expect e-invoicing requirements in European consumer markets to expand quietly through 2028.

Building a Roadmap Toward European VAT Compliance

european vat compliance lives or dies on the quality of your project plan. A four-quarter runway is the bare minimum. Year-one work covers diagnosis, vendor selection, and master-data cleanup. Year-two work covers parallel runs, supplier outreach, and audit-grade archive setup. Cutting corners costs more than the project budget. Penalties in Hungary alone reached €37 million across 1,400 audited companies last fiscal year.

The diagnostic phase reveals surprises about european vat compliance readiness. A mid-sized French exporter found that 22% of its outbound invoices already failed Factur-X validation. Product codes had been entered as free text. Another team discovered something worse. Its German subsidiary had been issuing invoices under the wrong company registration since 2022.

Supplier readiness usually surfaces last and hurts most. You can have perfect outbound machinery. But if your suppliers send broken XML, you cannot reclaim input VAT. Treat onboarding as a campaign. Segment suppliers by risk. Run technical clinics. Publish your test endpoint. Inbound exception handling is where VAT compliance across Europe actually gets tested.

A 12-month e-invoicing program — what to do, in order:

- Map every EU jurisdiction where you hold a VAT number or trade above the local threshold.

- Audit your current invoice formats and compare them against EN 16931 mandatory fields.

- Run a fit-gap analysis on your ERP — native module, middleware, or hybrid stack.

- Select a clearance platform vendor with multi-country reach (PEPPOL access point preferred).

- Cleanse master data — counterparty tax IDs, item classification, payment terms.

- Build a sandbox environment and connect it to each clearance platform test instance.

Pilot with two friendly suppliers and two friendly customers per jurisdiction. - Train accounts payable and accounts receivable teams on the new exception flows.

- Set archive policy at 10 years, immutable, retrievable on tax authority request.

- Schedule a dry-run audit using a Big Four firm or local tax advisor.

Habits That Keep You Aligned With EU Tax Reporting Rules

eu tax reporting rules evolve every quarter. Treating compliance as a one-time project guarantees regression. Live systems drift. Suppliers change platforms. Tax authorities publish updates faster than most ERPs can absorb. A monthly cadence with a named owner keeps the wheel turning. Even a part-time owner works. The cheapest mistake is forgetting to subscribe to your local clearance agency release notes.

Operational hygiene matters more than the choice of vendor when eu tax reporting rules shift mid-year. The same vendor can deliver compliant or non-compliant outcomes. It depends on how the customer runs it. Audit logs and version control set the floor. Reject-rate dashboards and quarterly reconciliations separate well-run deployments from sloppy ones.

The strongest finance teams build muscle memory around exceptions, not the happy path. A rejected invoice is the smoke alarm. Investigate, log, fix, and feed back into the master data. Tax reporting rules across EU jurisdictions reward this discipline. Cleaner audits and far fewer reconciliation cycles follow.

Operational habits that pay off:

- Owner accountability assign one named person per jurisdiction with a calendar reminder for release notes.

- Validation gate every outbound invoice runs through schema and business-rule checks before clearance submission.

- Weekly Review of tracking dashboard rejects by counterparty, error code and root cause.

- Master data freeze cycles lock tax IDs and product codes at month-end close to prevent silent drift.

- Test endpoint discipline rerun sandbox tests after every clearance platform release.

- Archive integrity quarterly retrievability tests confirming you can produce any invoice on demand.

- Cross-team review monthly stand-up with tax, IT, and AR/AP teams to surface exceptions and shared blockers.

FAQ

When does ViDA actually take effect across the EU?

- ViDA was adopted by ECOFIN on 11 March 2025. It entered into force shortly after. Single VAT registration provisions activate in July 2028. The cross-border digital reporting requirements start on 1 July 2030. Member states with existing national mandates keep their schedules. The 2014 EU directive on e-invoicing — the procurement rule — stays in full force as the legal base layer.

Which e-invoicing requirements should non-EU companies prioritise?

- If you are based outside the EU but registered for VAT in a member state, the local mandate binds you the same way it binds domestic firms. The exception is the reverse-charge mechanism. It can shift the obligation back to your EU buyer. Most non-EU sellers focus on three things first — PEPPOL connectivity, EN 16931 conformance, and clearance platform access in their highest-volume countries. Cross-border invoicing requirements within Europe reward a clear sequencing plan over a brute-force rollout.

Is PEPPOL mandatory under the new framework?

- Not strictly. PEPPOL is one of several recognised channels. France’s PPF uses it. The Belgian Mercurius routes through it. Norway, Sweden, and Finland rely on PEPPOL for B2G. Italy bypasses PEPPOL with SDI. Germany allows multiple delivery paths. If you sell across multiple member states, joining a PEPPOL access point cuts complexity sharply. Coverage for electronic invoicing across European borders keeps widening.

How do penalties compare across member states?

- Penalty ranges vary widely. Italy fines between €250 and €2,000 per missing invoice. Hungary: fines of 1 million HUF per violation. Poland: 100% recoupment of VAT not paid. France: annual penalties capped at €15,000 for repeat issues. Spain has approved fixed fines plus a 1% revenue overlay. The clearest signal sits in audit frequency. Countries with live clearance audit faster. Rigorous compliance with EU VAT rules reduces exposure long before the assessor knocks.

What records must we keep, and for how long?

- The baseline archive period is 10 years across most member states. Bulgaria and Romania use longer windows for certain sectors. Records must be retrievable in their original structured format. Metadata must remain intact. Digital signatures must be verifiable. WORM storage (write once, read many) is a common solution. National tax reporting rules in EU jurisdictions also expect a clear audit trail from invoice issuance through clearance acceptance to VAT return reconciliation.