VAT Exempt vs Zero Rated Supplies Explained

VAT Exempt vs Zero Rated Supplies Explained

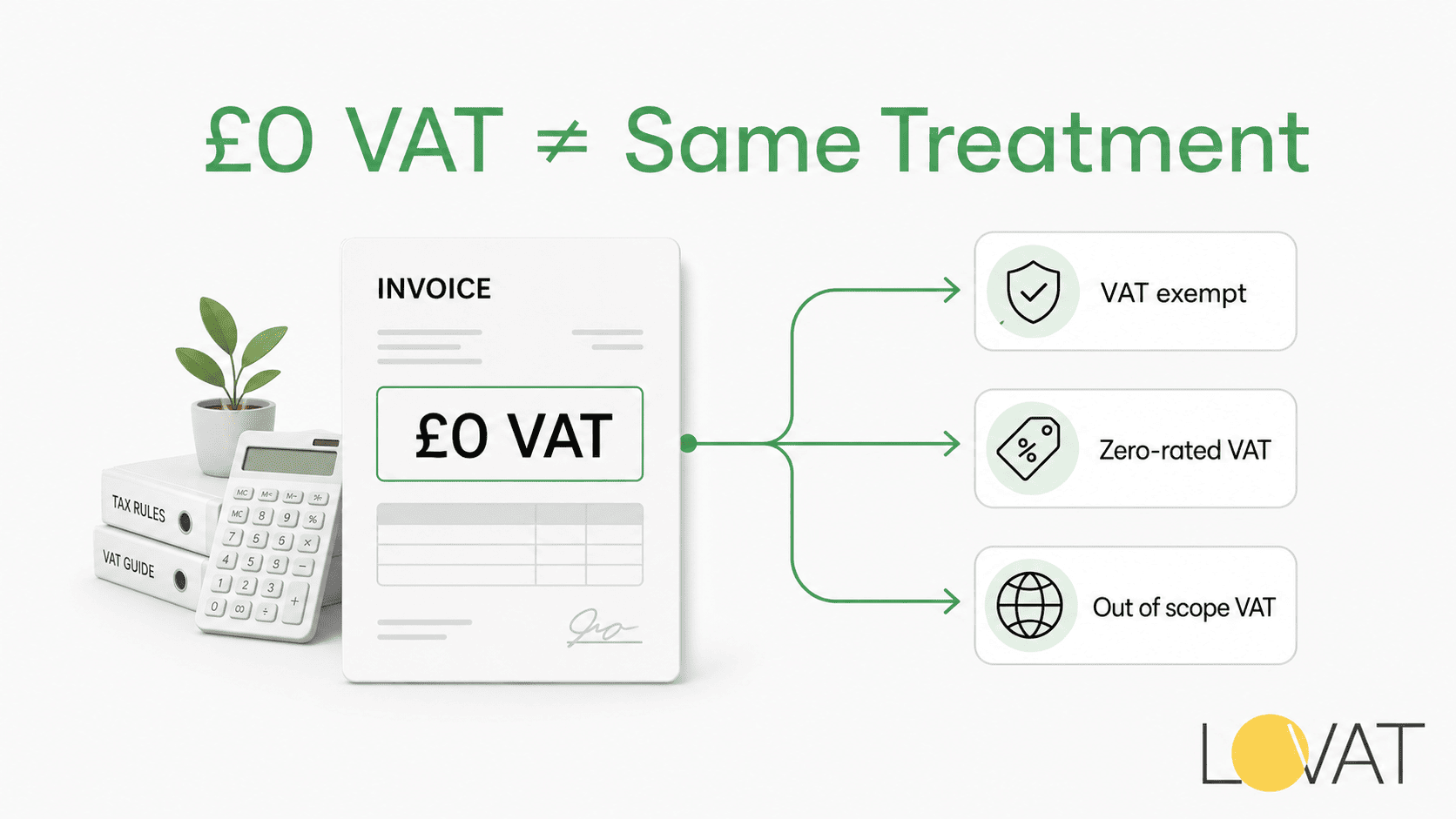

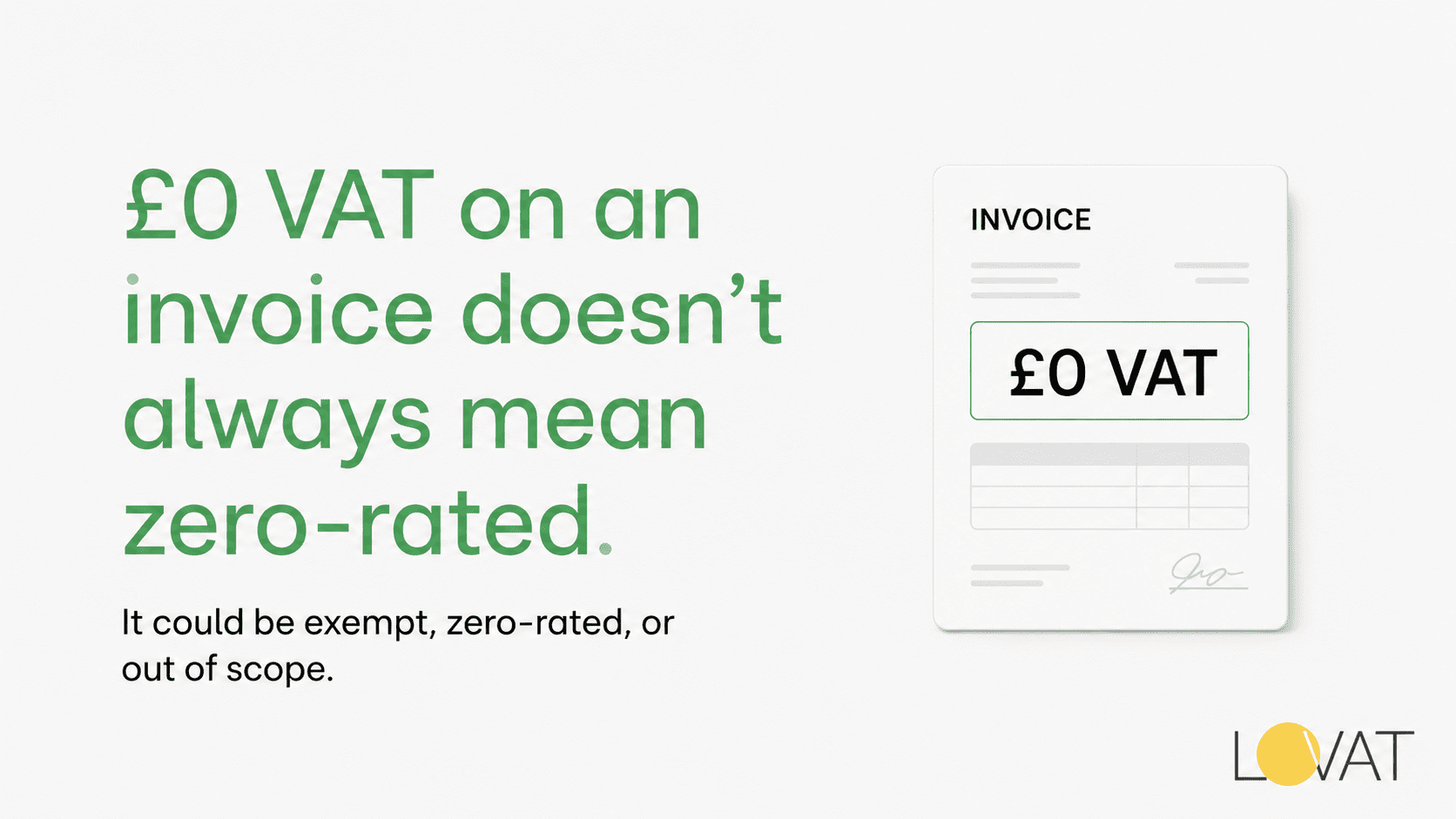

A £0 line on an invoice can mean three completely different things. Most business owners never check which one applies to them. A supply might be VAT exempt, sitting outside tax systems altogether. It might be zero-rated instead, taxed inside the system but at a nil rate. Or it might fall into a stranger category: a transaction that was never a taxable supply at all. Confusing these three is one of the most costly mistakes in business bookkeeping. Wrong treatment changes your return. It also changes your registration position and your input tax recovery. This guide walks through VAT exempt vs zero rated supplies in plain language. Then it explains the overlooked third category that trips up even experienced finance teams.

VAT-exempt meaning and core rules

The VAT exempt meaning is simpler than most people expect. The consequences, though, rarely are. Certain goods and services are removed from this levy entirely by law. Not taxed at zero. Not taxed at a reduced rate. Just placed outside that system completely. Tax authorities publish specific lists of exempt categories, and those lists rarely shift without warning. Insurance sits on that list. So does most finance and credit. Education and training usually qualify too. Health services from registered professionals usually qualify as well. Letting commercial land or buildings is often exempt in most circumstances.

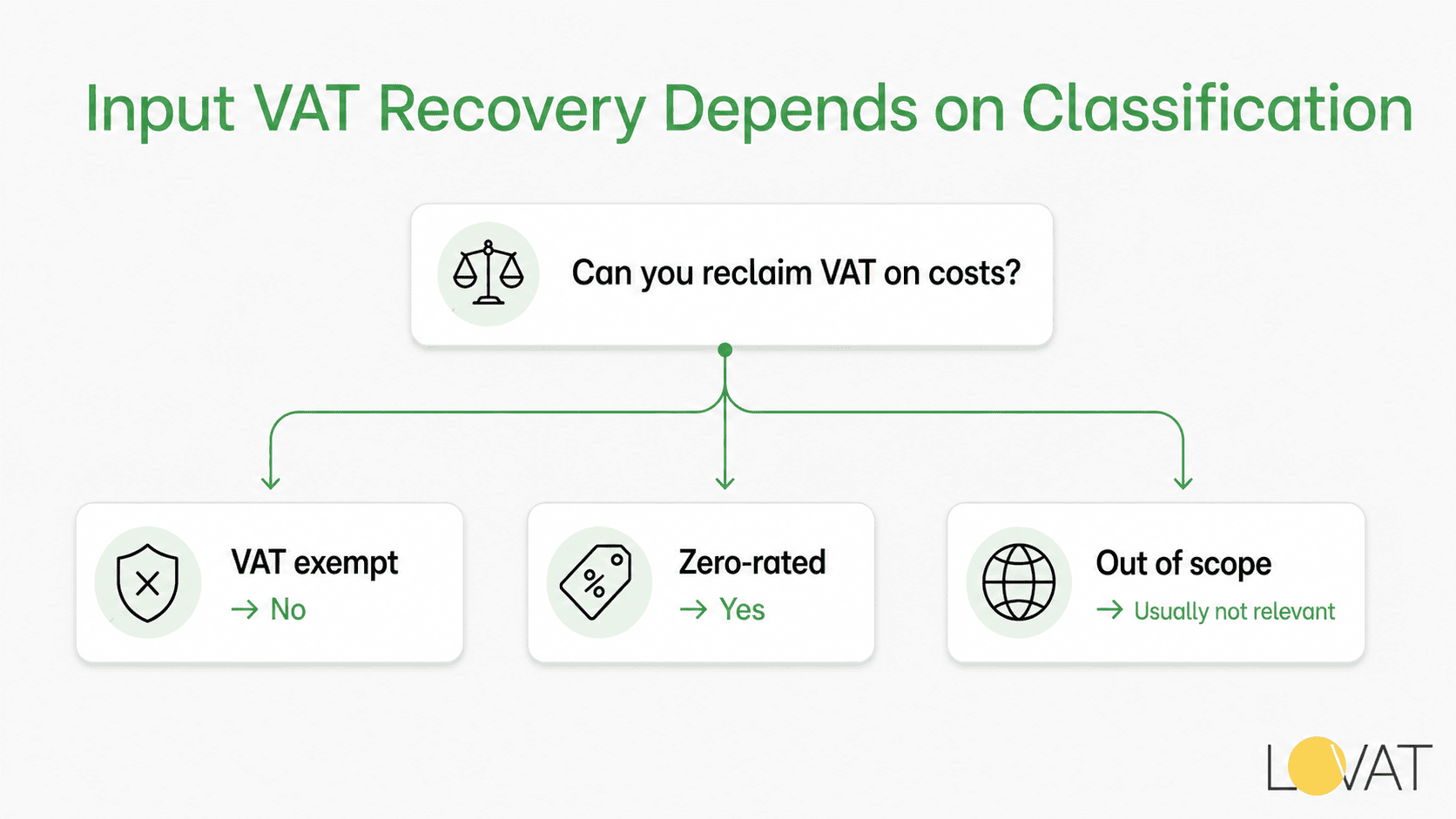

None of these sales ever enter your tax calculations. You charge nothing on the price. You also cannot reclaim tax on costs tied to that exempt supply. A business selling only exempt goods typically cannot register at all. That single detail separates exempt status from everything else in this guide. A sale exempt from VAT is still a real, legal supply. It simply lives outside the taxable system. This exemption applies the moment your sales match a listed category. No application or election is required from you.

A vat-exempt business carries a compliance burden that’s easy to underestimate. Charging tax on sales is off the table. Recovering tax on related purchases is equally blocked. That turns input tax into a direct cost rather than something to claim back. Private tutors and small consultancies often find themselves in this position. Mortgage brokers and insurance intermediaries commonly sit here too. Sometimes a business only realises it once an accountant flags the issue. Once a sector is classified as vat-exempt, that status rarely shifts year to year. Getting that initial classification right matters for exactly this reason.

What is zero rated VAT

What is zero rated VAT, and how does it differ from exemption? Short answer: zero-rated supplies remain fully taxable in law. They’re just taxed at a rate of nil. That single distinction carries real practical weight. Most food, children’s clothing, and books fall under this rule. Public transport does too, alongside qualifying exports. Exporters typically zero-rate goods shipped outside their home country.

Because a zero-rated VAT supply never leaves the taxable system, recovery rules work firmly in the seller’s favour. A business selling zero-rated goods can still register. Crucially, it can reclaim tax paid on related costs. Customers were never charged a penny, yet input tax still comes back. That’s a meaningful cash flow advantage. Exporters and food producers often push hard to confirm zero-rating wherever it applies. An alternative position offers no such recovery at all.

None of this happens automatically, though. Zero-rating usually comes with conditions attached. Children’s clothing has to meet specific age and sizing rules. Exports need evidence proving goods actually left the country. Printed material has to fit a fairly narrow legal definition. Miss any condition, and a sale slides back to standard rate. Sometimes that happens retroactively, if a tax authority later disagrees.

Comparing exempt and zero rated treatment

Side by side, that practical gap becomes far easier to see.

| Aspect | VAT exempt | Zero-rated VAT |

| Tax charged to customer | None | 0% |

| Counts as a taxable supply | No | Yes |

| Input tax recovery | Not allowed | Allowed |

| Registration effect | Cannot register if only exempt | Can register and reclaim |

| Common examples | Insurance, finance, education | Food, books, exports |

Two invoices can show the exact same £0 line. They can still sit in completely different categories. That gap shows up the moment someone tries to reclaim input tax.

Out of scope VAT and why it differs

A third category confuses even seasoned bookkeepers. Supplies can fall out of scope VAT, meaning they were never VAT supplies at all. They aren’t exempt. They aren’t zero-rated. They sit outside the entire tax framework, as though no tax ever applied. Wages sit here. So do dividends, statutory fees, and fines. Donations given with nothing handed back also qualify.

Plenty of transactions end up out of scope for VAT purely because of where the supply happens. It’s about location, not what’s being supplied. Services sold to business customers abroad often land here under place-of-supply rules. That test can be genuinely strict. Miss one condition, and the supply reverts to standard treatment instead. If the place of supply sits outside the seller’s home country, no local levy applies at all. Selling a business as a going concern works the same way. Tax law treats that transfer as no supply whatsoever. It sidesteps this levy entirely rather than reducing it. No registration test even applies once a transaction sits out of scope for VAT.

Why no VAT or zero rated labels cause confusion

Plenty of invoices simply read no VAT or zero rated. Nothing further explains why. That habit looks harmless at first glance. It quietly causes real problems further down the line. A bookkeeper reading that line can’t tell whether the supply was exempt, zero-rated, or genuinely out of scope. Each answer changes the return in a different way. A vat-exempt supplier benefits from a clear label just as much as a zero-rated one does.

The fix is straightforward, even if it’s rarely followed. Every invoice template should state the actual classification, not just the absence of a charge. Zero-rated tells a reader that supply stays inside the system, with full recovery rights. Exempt tells them the opposite. That scope-of-supply label tells them no supply ever happened. Swapping a vague no VAT or zero rated note for the precise category takes seconds in most accounting software. It also removes an entire category of disputes. Those disputes would otherwise surface during an inspection, when sorting them out costs far more time and money.

Zero-rated VAT vs VAT out of scope

Zero-rated VAT and VAT out of scope items both show £0 on the invoice. Legal reasoning behind each one could hardly be more different.

| Aspect | Zero-rated VAT | Out of scope VAT |

| Is it a taxable supply | Yes, taxed at 0% | No, not a supply at all |

| Included in taxable turnover | Yes | No |

| Appears on the return | Yes | Usually no |

| Input tax recovery | Allowed | Generally not relevant |

| Typical examples | Exports, books, food | Wages, dividends, fines |

Confusing these two categories is one of the most frequent bookkeeping errors. That fix starts in one place: classify the transaction correctly before it reaches the return.

Tax treatment examples by supply type

Real examples make all three categories far easier to apply correctly.

| Supply type | Tax treatment | Example |

| Private health consultation | Exempt | A registered doctor’s appointment |

| Children’s shoes | Zero-rated | Shoes sized for under 14s |

| Export of goods | Zero-rated | Shipment to an overseas buyer |

| Employee wages | Out of scope | A monthly payroll payment |

| Bank loan interest | Exempt | Interest charged on a business loan |

| Charity donation | Out of scope | A gift with nothing given in return |

These six rows cover most disputes that businesses bring to their accountants. Misreading any single row can shift a return materially.

How to determine if a supply is exempt from VAT

Working out whether a supply is exempt from VAT takes a structured approach, not guesswork. Start by checking your tax authority’s published guidance for your sector. Most categories already have dedicated, detailed rules. Insurance, finance, education, and health each carry specific guidance worth reading in full. Compare your exact supply against the listed conditions before assuming anything. Understanding vat exempt meaning behind each rule turns a long checklist into a five-minute check.

Consider these steps when classifying any new product or service line:

- Identify the exact goods or service being supplied.

- Check whether published rules list that supply as exempt or zero-rated.

- Confirm any conditions tied to that classification actually apply.

- Check whether the place of supply sits inside your home country.

- Record the chosen VAT code consistently across every invoice.

Skipping any of these steps risks an incorrect classification. That treatment often only surfaces months later, during a compliance review nobody was expecting.

Practical steps for exempt and zero rated compliance

Strong processes prevent most classification errors long before they happen. Many finance teams only properly answer what is zero rated VAT for their own product lines after a first enquiry letter arrives. A simple checklist prevents exactly that kind of late discovery. Consider building these habits into your invoicing workflow:

- Tag every product or service with its correct VAT code at setup.

- Replace vague nil-rate notes with an exact classification on each invoice.

- Review zero-rating conditions whenever product details or sourcing change.

- Separate exempt sales clearly within your bookkeeping software.

- Track partial exemption calculations if you sell both exempt and taxable items.

- Re-check classifications on a regular schedule, since tax guidance does get updated.

Businesses that mix exempt and zero-rated sales face an added layer of complexity. They become partly exempt and must apportion input tax accordingly. That’s rarely a calculation worth doing by hand once volumes grow. Getting professional advice early often saves far more than it costs.

Manually tracking VAT exempt, zero-rated, and out of scope supplies across several markets gets messy fast. That’s especially true once a business starts selling into multiple countries at once. The vatcompliance.co platform classifies transactions automatically and keeps every return audit-ready. See how it works

Related articles

Common Questions About

Exempt And Zero Rated Supplies

Is vat exempt meaning the same as zero-rated

No. Exempt supplies sit outside this levy entirely, with no input tax recovery. Zero-rated supplies stay taxable, charged at 0%, with full recovery rights. Seeing no VAT or zero rated on an invoice tells you nothing about which one actually applies.

What is zero rated VAT used for

It applies mainly to essential goods governments want to keep affordable. Food, books, children’s clothing, and qualifying exports are typical examples.

Can a business reclaim VAT on exempt purchases

Generally, no. A fully exempt business usually cannot register for VAT. It therefore cannot reclaim any related input tax either.

What does out of scope for VAT actually mean

It means no VAT supply ever existed. Wages, dividends, fines, and certain overseas services fall into this group. Anything genuinely vat out of scope never appears on a return.

How do I know which tax category applies to my sales

Check your local tax authority’s published guidance for your sector first. A tax specialist can confirm the correct treatment quickly.

Still unsure whether your latest product line counts as VAT exempt, zero-rated, or out of scope? The vatcompliance.co team reviews your supply chain and confirms the right treatment within days. Talk to a VAT expert