VAT reverse charge mechanism cases for sellers and buyers

A reverse charge for sellers

1 Supply between EU member states (EU-EU)

Reverse charge is a special scheme when a buyer calculates VAT and pays it. It occurs in situations of cross-border sales when your buyer is a VAT registered business.

Let me give you an example:

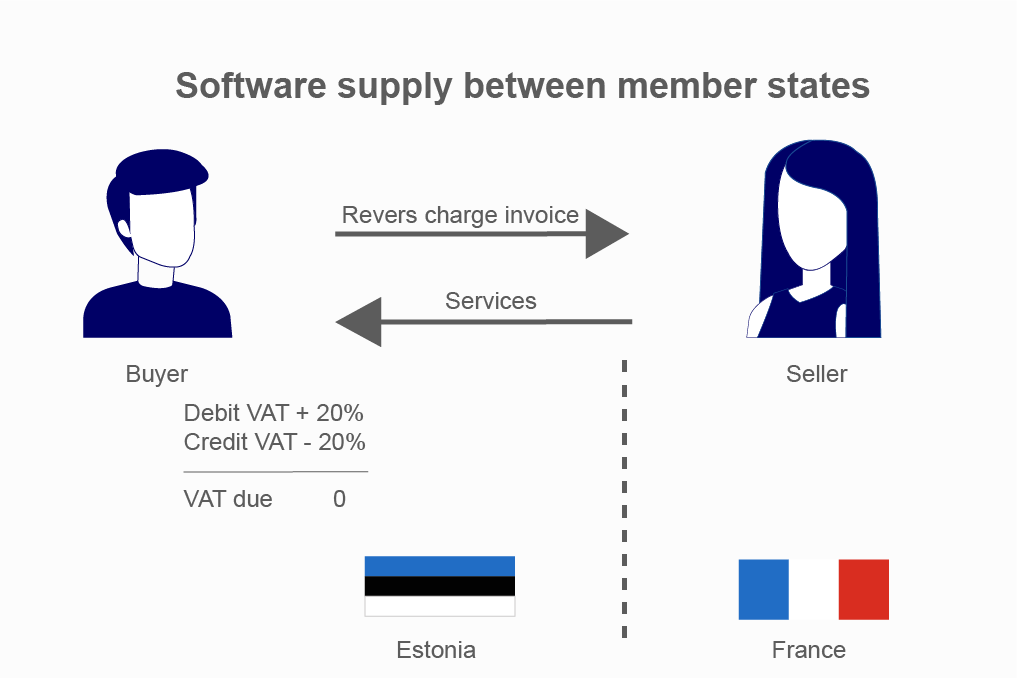

French businesses sell software to businesses registered in Estonia. It is an intra-community B2B sale. A place of supply for such service is a place where a customer is registered (General rule). That means that the place of supply is Estonia and Estonian VAT must be calculated. French supplier needs to issue a reverse charge invoice for such supply.

A reverse charge invoice is a normal VAT invoice with a customer VAT number and “reverse charge” sign. The Estonian customer will add this invoice to a VAT ledger and calculate the Estonian VAT. They may at the same time credit this VAT, so in total VAT due will be zero.

Reporting obligations:

- Seller needs to report this sale at a Sales list

- Buyer needs to report this purchase at periodic VAT return

Exemptions:

- Your buyer is an EU business but don’t have a VAT number

- Place of supply for VAT purposes in your country. It may occur when goods you sell don’t leave departure country. Or place of supply of services – is in Origin country (for example educational services, catering services, land-related services)

2 Supply between the EU and Northern Ireland (EU to NI)

EU has an agreement with NI and it covers the VAT issue. According to VAT protocol when you sell to NI business you need to use the reverse charge approach. Check it should be a VAT number started with NI. If you see a GB VAT number you need to apply the ROW rule.

Reporting obligations:

- Seller needs to report this sale at a periodic VAT return – zero-rated supply

- Buyer needs to report this purchase at a periodic VAT return

The main distinction from EU-EU is an absence of an obligation to report sales in a sales list.

3 Supply between the EU and the rest of the world (EU-ROW)

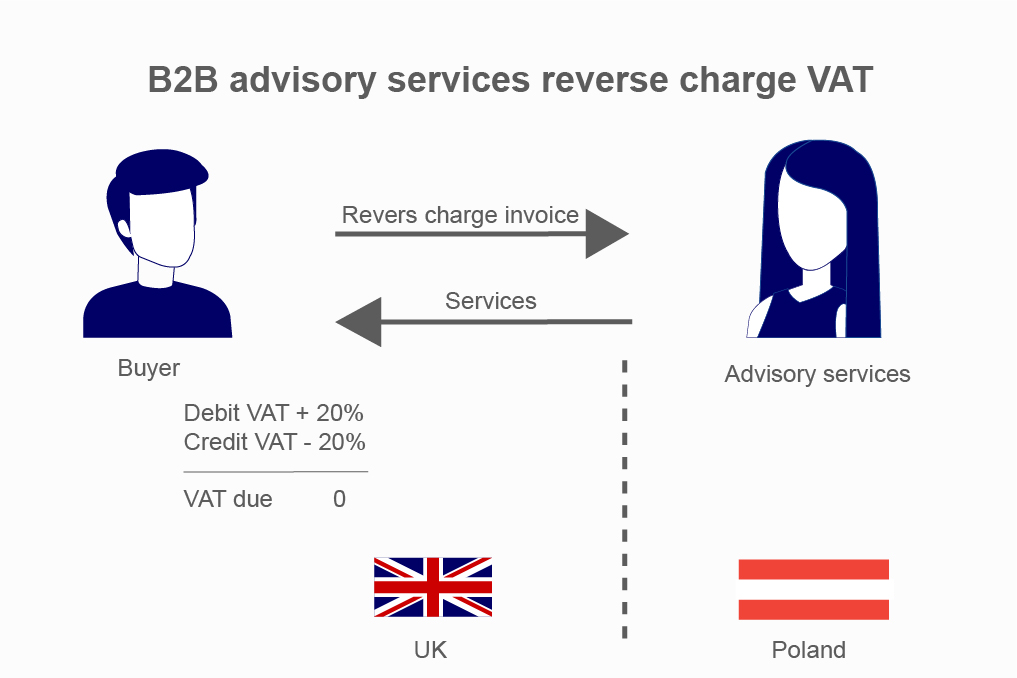

As you can never predict VAT rules for service you supply in another country you normally issue an invoice without VAT (not reverse charge invoice) if the place of supply is not your country. This is valid for bookkeeping, legal, advertising, and other services.

For example, a Polish company invoices its UK client for advisory services. Polish company must issue an invoice without VAT as soon as place of supply for such service isn’t Poland. Polish company doesn’t show this amount in their VAT return as it is out of scope of Polish VAT.

At the same time UK buyer shows this amount in the UK VAT return calculate 20% UK VAT and at the same time can credit this sum in the same VAT return.

A reverse charge for buyers

1 Purchase from a supplier from another EU member state (EU-EU)

When you are EU based company and buy goods in another EU country you pay an invoice without VAT which means that you need to calculate VAT in the destination country and show such expenses as intracommunity acquisitions in your VAT return.

The same situations when you move your goods from one EU country to another EU country. You need to invoice yourself with a reverse charge invoice. For example, when you move your goods from a French warehouse to a German warehouse you issue an invoice from your French VAT number to your German VAT number. And show the amount in a French sales list and a German VAT return.

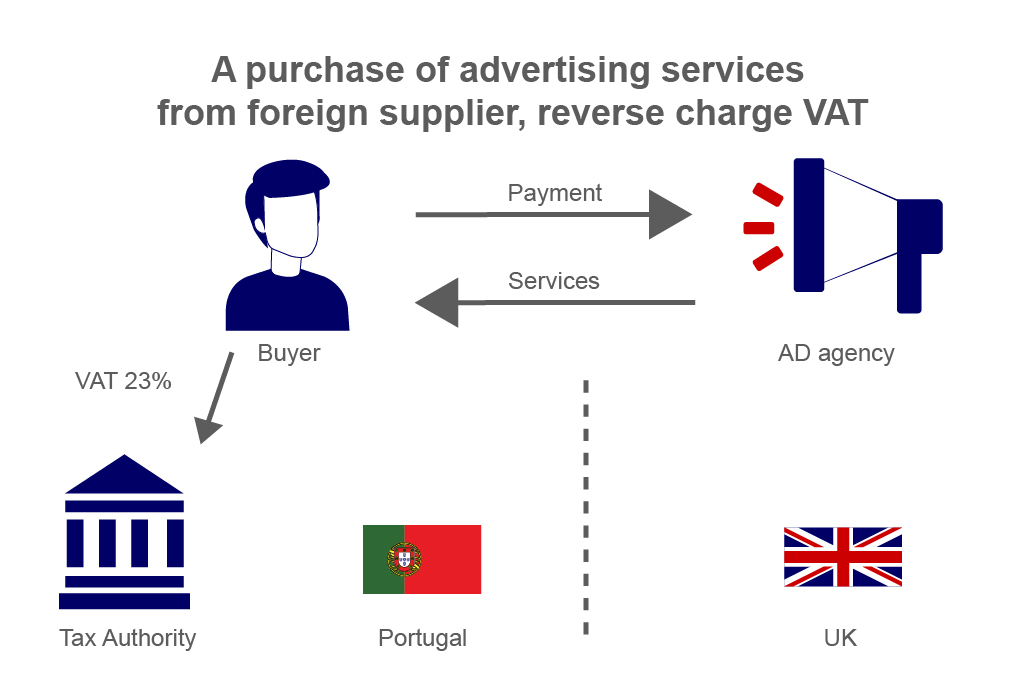

2 Purchase from a supplier from the rest of the world (EU- ROW)

When you buy services from the non-EU business and place of supply for such service is a place where the buyer is established you need to charge domestic VAT on such purchase.

For example, a Portuguese business buys advertising services from a UK business.

General rule according to EU Directive is when a place of supply is a Buyer country. That means that buyer needs to calculate VAT on the purchase invoice from the UK service provider and show this amount in the Portuguese VAT return.