6 new VAT laws to ensure compliance in 2021

6 new VAT laws to ensure compliance in 2021

Marketplaces become deemed suppliers when facilitating sales in the EU, UK, Canada, New Zealand, US, Norway.

EU: Distance sales thresholds were replaced by an EU-wide €10,000 threshold for digital services and goods. That means intra-community sales are subject to VAT in the EU country of destination. Businesses need to ensure they use the correct VAT number for transactions to comply with the destination-based VAT rules.

To simplify reporting obligations due to this change, the Mini one-stop-shop was extended to a One-stop shop for goods and services, which centralizes VAT compliance and requires businesses to associate their VAT number with the scheme for efficient processing.

Import One-Stop Shop Scheme: The de minimis threshold for the import of low-value goods (LVG) was removed, and now VAT needs to be paid for all goods imported into the EU. This change aims to equalize conditions for non-EU and EU sellers. A parcel with an intrinsic value of less than €150 is considered LVG. To make imports simpler and less costly, European administration introduced the Import One-Stop Shop scheme, which also requires businesses to align their VAT number for accurate tax calculations and filings.

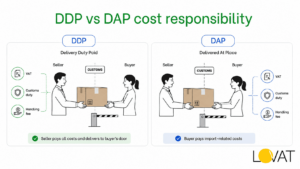

Brexit: On January 1st, the transitional period for the UK to leave the EU ended. That means free circulation for goods and services is no longer available for goods crossing the border between the UK and the EU. Customs procedures must now be executed for all goods—small parcels or large supplies—traveling from the EU to the UK and vice versa. Businesses must also use the appropriate VAT number when dealing with cross-border transactions to ensure compliance with the new tax regime.

Great Britain: De minimis was removed, and a new VAT scheme was implemented for the import of LVG. LVG refers to orders with an intrinsic customs value of less than £135. Businesses must now register for VAT in the UK and use their VAT number to account for transactions under the updated scheme.

Northern Ireland (NI): NI is treated as a Member State regarding VAT on goods. This means businesses do not need to fill out customs declarations or complete customs clearance for goods sold to NI. Businesses can also benefit from a distance sales threshold and do not need to register for VAT if they sell less than £70,000 worth of goods to NI. However, NI is not treated as a Member State for VAT on services. If you sell subscriptions or other services to NI, you must register for VAT in the UK and associate your VAT number with these transactions for compliance.