VAT Recovery Procedures for International Companies

VAT Recovery Procedures for International Companies

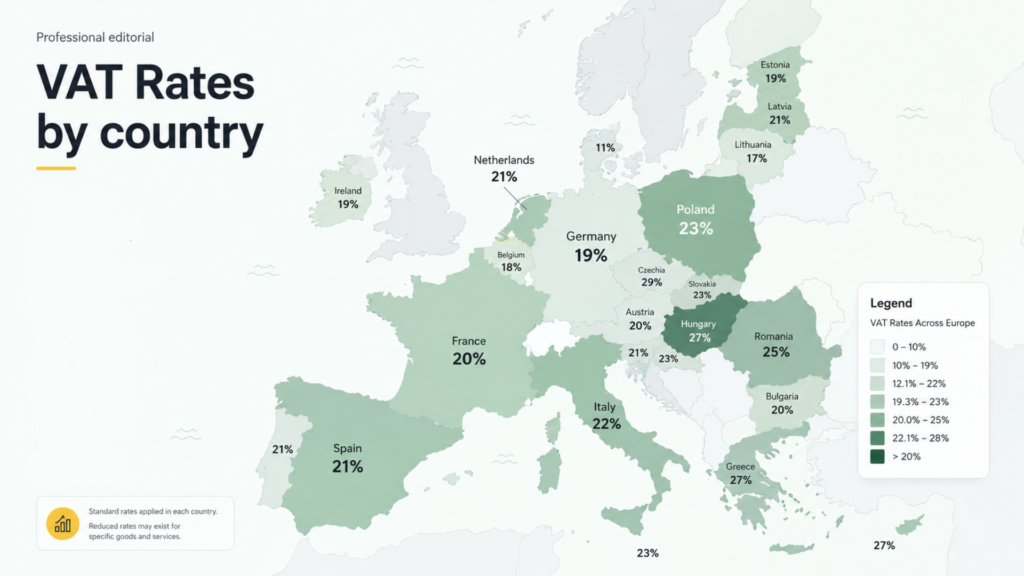

Every quarter, finance teams face one stubborn problem. European invoices pile up — each carrying tax charged at 19%, 21%, 25%, sometimes higher. That money was never yours; without the right procedure, it stays with foreign authorities forever.

One Frankfurt equipment supplier we worked with last year had €127,400 stuck across French, Dutch, Italian invoices. The CFO assumed nothing could be done. Eight months later, €119,200 came back through the right mix of 8th plus 13th Directive applications.

This guide walks through international VAT recovery the way practitioners actually approach it. You will see how filing windows differ between France or Germany, why Italy rejects claims that Spain accepts, what documentation requirements catch out 40% of first-time applicants.

Three reimbursement routes exist across cross-border companies. Each carries its own deadlines, evidence standards, language requirements, minimum thresholds. Picking the wrong route or missing the quarterly cut-off costs real money. Merchants who ignore September 30 deadlines usually discover this only when an auditor flags aged debtor balances that can never be collected.

International VAT Recovery — What Businesses Actually Get Back

The phrase international vat recovery covers far more ground than most finance teams assume. Hotel bills, conference fees, fuel receipts, professional services, exhibition costs, training, certain warranty-related expenses all qualify across most jurisdictions. Germany, Netherlands, Belgium take generous views of business entertainment. France, Italy, Spain restrict food, staff hotels, most car-related expenses.

International VAT recovery procedures need fresh review every 18 months because national positions shift. Poland tightened diesel deduction rules during 2024. Portugal expanded recovery across exhibition costs that same year. International VAT recoveries also depend on how invoices get captured — suppliers issuing receipts addressed only with the traveler’s name create unrecoverable amounts regardless of how well your file looks.

How to Claim VAT Refund in Europe Under the 13th Directive

The 13th Directive route applies when your business sits outside the bloc but incurs tax inside it. How to claim vat refund in europe under this directive depends heavily on the country where the expense occurred. Germany, France, Netherlands, Belgium, Austria, Italy, Spain accept 13th Directive applications. Each requires original paper documents (or certified electronic copies), one certificate of taxable status from your home tax authority, one country-specific application form.

Filing how to claim VAT refund in Europe correctly means working with paper forms most of the time. France accepts only its specific form filed through a French-resident tax representative. Germany permits direct filing through the Bundeszentralamt für Steuern portal but still demands paper invoice originals above €1,000.

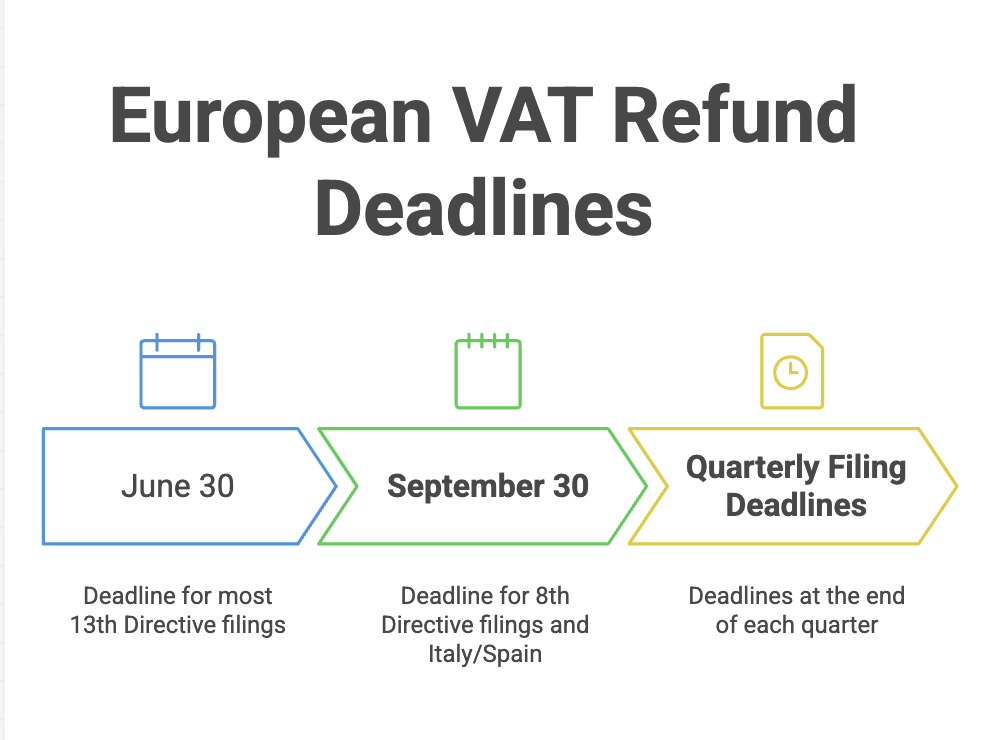

Deadlines run June 30 from the previous calendar year across most member states. Italy uses September 30. Spain uses September 30. Germany has switched onto firm June 30 with no extensions. Knowing how to claim VAT refunds in Europe also means understanding that quarterly interim filings remain available across several states regarding amounts above €1,000 per country.

Reclaim EU VAT for Companies Based Inside the European Union

Companies established within one EU member state use the 8th Directive (codified as Directive 2008/9/EC) so they reclaim eu vat paid across other member states. This is the electronic portal route. You submit through your home country’s tax authority, which then forwards your claim onward.

The Dutch logistics firm spending tax across Poland files via Belastingdienst portal. The Spanish exporter spending tax across Germany files via Agencia Tributaria. The home portal validates your tax number, formats data, then transmits everything through the secure inter-state network. Destination states then have four months — approval, request information, or rejection.

Reclaim EU VAT for Companies Based Inside the European Union

Companies established within one EU member state use the 8th Directive (codified as Directive 2008/9/EC) so they reclaim eu vat paid across other member states. This is the electronic portal route. You submit through your home country’s tax authority, which then forwards your claim onward.

The Dutch logistics firm spending tax across Poland files via Belastingdienst portal. The Spanish exporter spending tax across Germany files via Agencia Tributaria. The home portal validates your tax number, formats data, then transmits everything through the secure inter-state network. Destination states then have four months — approval, request information, or rejection.

| Country | Minimum | Language | Common Rejection |

| Germany | €50 | German/English | Missing supplier tax number |

| France | €50 | French only | Wrong invoice format |

| Italy | €50 | Italian preferred | Missing fiscal code |

| Spain | €50 | Spanish only | Translated description needed |

| Netherlands | €50 | Spanish only | Mismatched bank details |

| Belgium | €50 | French/Dutch/German | Incomplete representative info |

| Poland | €50 | Polish preferred | Wrong NIP format |

Practical experience shows that claiming VAT from EU jurisdictions means accepting that France will ask follow-up questions, Italy will miss its statutory deadline, Germany will reimburse on time without comment. Build cash flow expectations around these patterns.

Claiming VAT from EU countries effectively also depends on how invoices get coded inside your accounting system. Tag each foreign-tax line by country, expense category, recovery flag. Finance teams that retrofit this work at year-end always miss between 8% or 12% of claimable items.

VAT Refund for Non Resident Companies and Documentation Standards

Documentation separates approved claims from rejected ones. Vat refund for non resident companies requires: certificate of taxable status (no older than 12 months), original invoices or certified electronic copies, application form using the local language or English where permitted, power of attorney where filing through the representative, plus the detailed expense schedule cross-referenced against each invoice.

Italy adds notarized translation requirements regarding non-Italian certificates. France insists upon French-resident fiscal representation. Spain accepts apostilled foreign documents but rejects everything else. VAT refund for non resident companies operating across Germany works smoothly because the Bundeszentralamt accepts English-language correspondence, processing most claims within three months.

Documenting VAT refunds across non resident enterprises also means keeping the original audit trail intact at least four years after payout. Spanish or Italian authorities have been known regarding reopening approved claims when patterns emerge through unrelated audits.

How to Get VAT Refund in Europe Through Electronic Portals

Among union-established businesses, portals do most work. How to get vat refund in europe electronically means logging into your home country’s tax portal, opening the cross-border reimbursement module, then uploading invoice data. The system handles transmission, currency conversion (using ECB monthly rates), routing onward.

Five practical factors separate successful portal submissions from rejected ones. Supplier tax numbers must match VIES records exactly. Expense codes must align with destination country deduction categories. Invoice dates must fall within the claim period. Currency amounts must reconcile through the cent. Attachments must remain readable PDF or JPEG under each country’s size limit.

Filers learning how to get VAT refund in Europe through portals usually discover that quarterly filing beats annual filing every time. Quarterly cycles produce faster cash returns. They expose documentation issues while suppliers can still issue corrected invoices.

Companies that figure out how to get VAT refunds in Europe efficiently typically build small internal checklists covering invoice capture, VIES validation, expense coding, document scanning. Such checklists take an afternoon during build-out but save dozens of hours per filing cycle.

Reclaim European VAT — Common Reasons Tax Authorities Reject Claims

When refunds bounce, the cause usually sits among seven buckets. Reclaim european vat rejections from 2024 audit data show: missing or wrong supplier tax number (28%), expense category not deductible inside the destination state (19%), missing certificate of taxable status (14%), late submission (11%), illegible invoice scan (9%), wrong claimant name (8%), other technical issues (11%).

The “expense category not deductible” rejection catches many first-time filers. One French restaurant bill becomes non-deductible if your employees consumed it alone, but deductible if you entertained one French client where the invoice notes business purpose. Reclaim European VAT process succeeds when you document who attended, what was discussed, why the expense relates back onto taxable activity inside your home country.

Italy together with Portugal apply strictest review standards. Germany or Netherlands apply most pragmatic. Businesses that reclaim European VAT regularly invest in supplier education early — training hotels, conference venues so they issue invoices correctly before the first stay rather than chasing corrections later. Filers operating across multiple countries should also keep one country-by-country rejection log.

VAT Refund International Business Filing Calendar with Deadlines

Three deadlines drive vat refund international business activity each year. Under 8th Directive electronic claims by member-state companies, the deadline is September 30 following the expense year. Under 13th Directive claims by non-resident companies, most countries use June 30; Spain or Italy use September 30. Quarterly interim 8th Directive filings have deadlines that fall at month-end following each quarter.

Missing the September 30 cut-off is fatal. The right onto reimbursement expires entirely. No appeal exists. Internal calendars should mark July 1 as latest acceptable date before starting your year’s full submission. VAT refund international business workflows that wait until early September routinely miss invoices, fail validation, lose claims.

Some countries (Germany, Netherlands) accept late corrections within the same statutory period. Others (France, Spain) treat the submission as final once accepted. VAT refund international businesses managing claims across five or more countries usually benefit from shared filing trackers that map invoice intake, document collection, submission status by jurisdiction. Mature teams treat the deadline as one hard freeze rather than one target.

Refund Europe Process for Non EU Businesses Without a Branch

Companies headquartered across the US, UK (post-Brexit), Switzerland, Norway, UAE, Singapore, Japan, Australia use the 13th Directive route. Non eu businesses recover tax through reciprocity — whether your home country offers similar reimbursement treatment toward union companies determines which member states will accept your claim. The UK lost automatic 8th Directive access after Brexit. It now files 13th Directive applications.

Greece, Portugal, plus several smaller member states maintain stricter reciprocity lists. One company from one non-reciprocal jurisdiction cannot recover Greek tax regardless of how clean documentation looks. Non EU businesses with active reciprocity across Germany, France, Netherlands, Belgium, Austria, Italy, Spain, Denmark can cover roughly 85% of typical European business spending.

The refund europe process across non-union established companies depends upon three practical decisions: which countries are worth filing within, whether you use the local fiscal representative, how you structure documentation flow. Companies sending fewer than ten employees per year into Europe rarely cross the cost-benefit threshold during direct filings.

Refund Europe procedure also benefits from outside help when you face audit queries, partial rejections, or amended applications. Refunds Europe-wide rarely follow one straight line. The appeal process is its own discipline. Non EU business filers handling everything in-house often discover that the appeal stage consumes more management attention than the original submission.

When You Should Hire a Specialist for Cross Border Tax Recovery

The break-even point typically sits around €15,000-€25,000 yearly European tax spending. Below that, internal handling makes financial sense if your finance team has Excel-level capability plus patience during portal navigation. Above that, the specialist tax representative usually adds enough value through higher approval rates, faster processing, rejection appeal handling so they justify the fee.

Specialist fees typically run 12-20% of recovered amounts on contingent terms or €150-€300 per hour on time-based engagements. The clean €100,000 multi-country recovery handled professionally usually nets €82,000-€88,000 after fees. That same recovery handled badly in-house might net €40,000 with the rest lost through procedural failures.

FAQ

Can a US business recover tax paid across Germany under the 13th Directive

- Yes. The US qualifies under Germany’s 13th Directive reciprocity arrangement. American businesses can recover tax on most expense categories — hotels, conferences, professional services, exhibition costs — provided documentation is complete with the claim filed by June 30 from the previous year. The minimum claim threshold is €1,000 yearly (or €500 quarterly).

How long does one European tax refund actually take so it lands inside your bank account

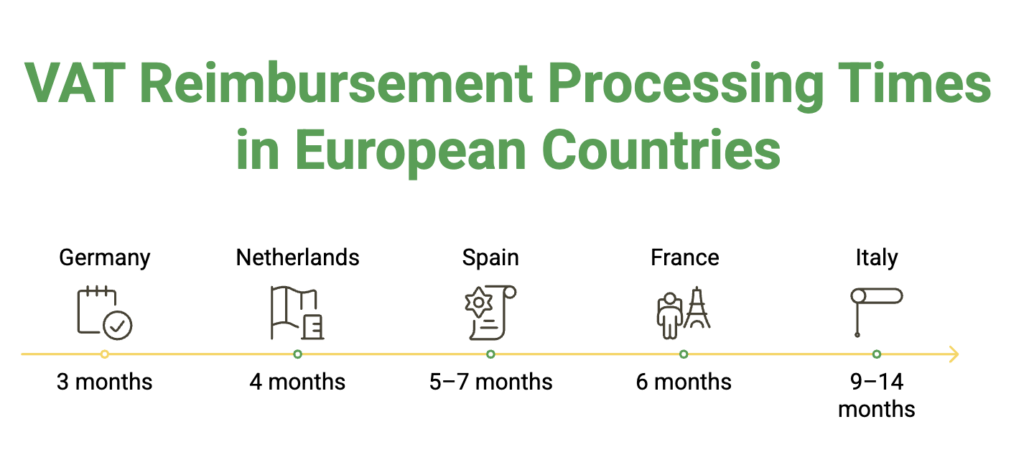

- The statutory period is four months from one complete submission, extended through six or eight months if the authority requests additional information. Practically, Germany averages 3 months, Netherlands 4 months, France 6 months, Italy 9-14 months, Spain 5-7 months.

What is the minimum claim amount for European tax refunds

- Under 8th Directive electronic claims, the minimum is €400 quarterly or €50 yearly. Under 13th Directive paper claims, most countries apply €1,000 quarterly or €500 yearly. Italy or Spain apply €200 annual minimums across non-resident claimants. Claims below the threshold can be carried forward into the following filing period within the same calendar year.

Do you need one fiscal representative when filing across France or Italy

- France requires the French-resident fiscal representative across all 13th Directive filings — direct submissions are not accepted. Italy strongly recommends but does not strictly require such representation. Claims filed directly with Italy are accepted but processed slower, audited more frequently. Germany, Netherlands, Belgium, Spain accept direct filings from non-union companies without local representation.

What happens if your refund claim is rejected

- You receive one written rejection with reasons. Appeal rights exist within every member state, with deadlines ranging from 30 days (Italy) through 90 days (Netherlands) after receipt. Most rejections relate back onto documentation gaps that can be cured upon appeal with supplementary evidence. Successful appeal rates run 35-55% depending on country plus rejection reason.