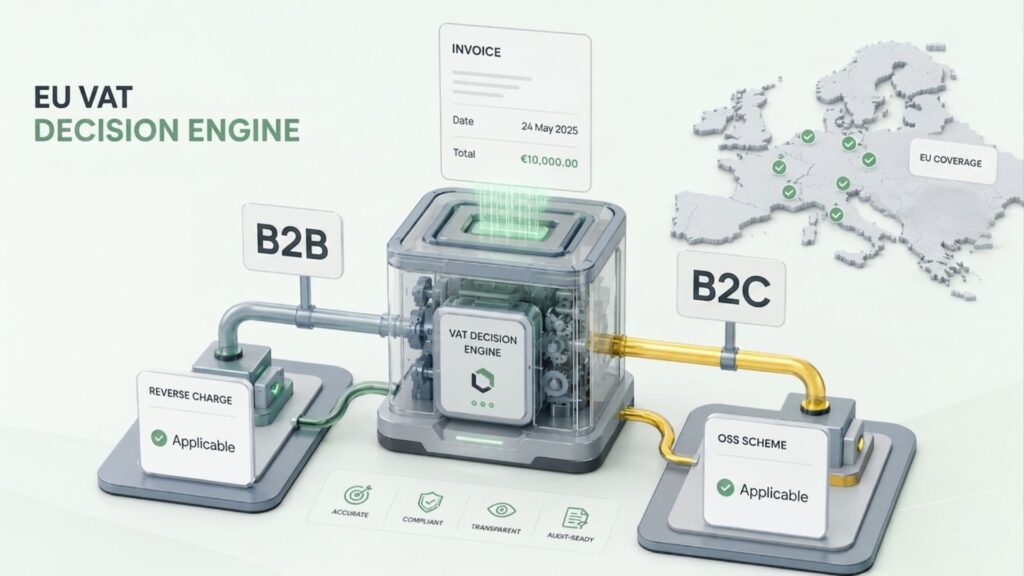

B2B and B2C VAT rules on Cross Border Sales in Europe

B2B and B2C VAT rules on Cross Border Sales in Europe

Two merchants sell identical software subscriptions online. One ships to another company with a German identification number. The other sells directly to a French consumer from a Lithuanian server. The sales look almost identical. The tax treatment could not be more different.

That gap — between how the bloc taxes deliveries to registered companies versus goods and provisions to final consumers — sits at the centre of every international compliance decision a European vendor makes. Get the classification right and the paperwork flows cleanly. Misread customer type and you either under-collect (owing the shortfall yourself) or over-charge and lose clients to competitors who did the homework.

Directive 2006/112/EC governs the entire framework, now substantially supplemented by the July 2021 reforms that replaced fragmented distance-selling thresholds with the One-Stop Shop (OSS) and Import One-Stop Shop (IOSS). These changes still catch firms off guard, particularly those that built cross-border processes under the old regime and never updated them.

This guide covers the full picture: the fundamental Wholesale/B2C distinction, place-of-provision rules determining where tax falls due, reverse charge mechanics making most cross-border Business-to-business dealings straightforward, OSS enrolment covering union-wide consumer obligations from a single filing, complexity introduced by digital platforms, triangulation, call-off stock, fiscal representation, e-invoicing obligations, and the compliance architecture coming with selling into mixed markets.

Whether you operate a SaaS platform, a physical merchandise manufacturer, a marketplace with vendors across twelve member countries, or a professional outputs firm advising European clients from outside the bloc, every rule covered here directly affects your filing position.

How the bloc Distinguishes B2B VAT from B2C levy at the Point of Sale

The entire architecture of European indirect taxation rests on a single question asked at the moment a dealing is recorded: is the customer a taxable person acting in that capacity, or a private individual making a final consumption purchase?

That question determines the place of supply, who accounts the VAT, reporting mechanism, invoice format, and risk exposure if the classification is wrong. Answering it correctly is not optional — it is the foundation of every international sale a European firm makes.

The Legal Definition of a Taxable Person

Article 9 of the Directive defines a taxable person as any individual who independently carries out an economic activity, regardless of purpose or result. This covers limited companies, sole traders, partnerships, and many public bodies. Employees representing their employer are excluded.

When a taxable person acquires goods or offerings in the course of business — the operation falls under wholesale rules. When a private individual makes the same acquisition — or when a taxable person purchases personally rather than professionally — the exchange is treated as B2C.

The VAT Number as the Classification Signal

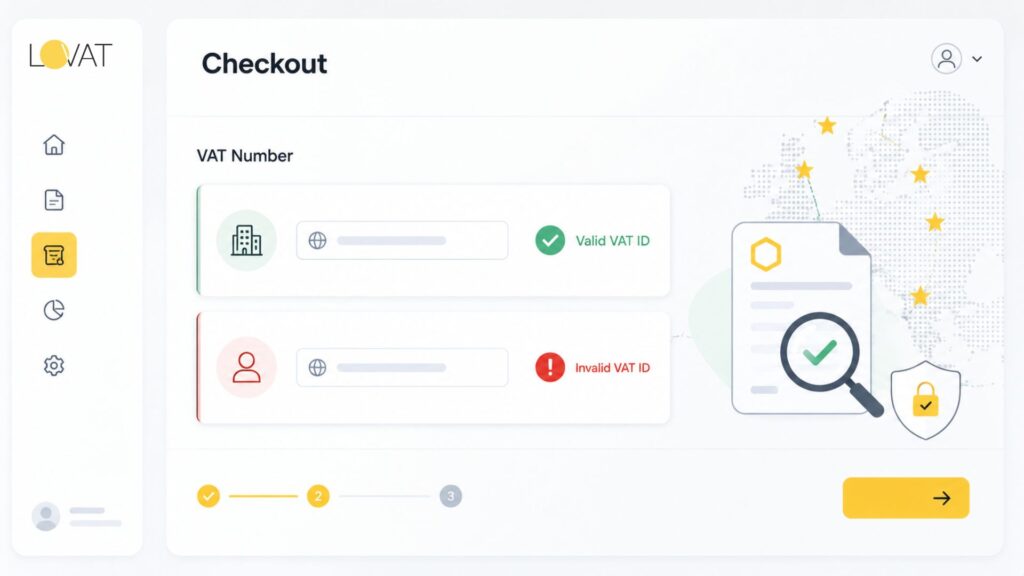

A entity registered in indirect tax in any member country holds a VAT identification number, verifiable through VIES. When a recipient provides a number VIES confirms as active, the supplier holds documentary evidence to treat the sale as Business-to-business.

Inter-company VAT EU rules therefore hinge, in most cross-border sales, on whether the acquiring party furnishes a verified number at the point of sale. Collecting the number is insufficient — you must validate it. A number failing VIES cannot support a Commercial classification covering cross-border activities or an intra-Community zero-rating for goods.

Every organisation processing cross-border deals needs a live VIES check at the time of sale (or before invoice issuance), timestamped, and retained as part of the deal record.

B2C VAT — The Default Position

Where no valid number exists, or the buyer identifies as a private consumer, the sale defaults to B2C. B2C VAT obligations apply: standard imposition at the purchaser’s territory percentage, collected by the merchant, remitted to the relevant authority, with no reverse charge available. The OSS collapses multi-country consumer reporting into a single quarterly return filed in the vendor’s home member territory.

Where Classification Gets Complicated

Three buyer categories create genuine ambiguity:

- Non-company legal entities: Charities, foundations, and public bodies may hold registration numbers covering specific activities while purchasing outside those activities. A hospital buying administrative software may not be acting as a taxable person in fiscal charge terms, depending on member-nation interpretation of its public authority status.

- Mixed-use purchasers: A freelance consultant who buys a laptop partly for business use, partly personal use is technically a taxable person — but the personal portion falls outside Wholesale treatment. Most European countries handle this through input-tax apportionment rather than dealing reclassification, but the seller still invoices from the enterprise-to-trader default when a valid number is provided.

- Sub-threshold enterprises: Small operators below the domestic registration threshold hold no number. From the seller’s perspective they look like consumers. Community law provides no shortcut here — suppliers must apply B2C rules to these purchasers even though the counterparty is commercially active.

European Court of Justice jurisprudence on misclassification is unambiguous. In Tolsma (C-16/93) and subsequent rulings, the Court consistently placed obligation on suppliers to determine the correct status of their counterparty. fiscal authorities in Germany, France, and the Netherlands have intensified audit focus upon cross-border classification since 2022.

Invoice Requirements and What They Signal

Invoice format confirms the classification applied. Business-to-business cross-border invoices must carry the purchaser’s identification number, a reverse-charge reference where applicable, and a zero-level annotation with its legal basis. B2C invoices must country the applicable percentage and tax amount, corresponding to the purchaser’s country of residence.

A Inter-company invoice template not prompting to capture number entry is not a formatting issue — it is a process failure creating systematic misclassification risk across every sale the template generates.

Cross Border VAT EU — The PROTECTED 0002 rules governing Every Transaction

“Place of supply” is a legal concept, not a physical one. It does not mean where goods originate or where the seller is incorporated. It means the territory holding the right to tax amount indirect tax on the operation. Cross border VAT EU obligations flow directly from these rules, and errors in place-of-delivery analysis routinely produce the most expensive compliance failures European traders face.

PROTECTED 0004 for Goods — General Rules

For physical merchandise, the general rule places output where goods are located when put at the purchaser’s disposal. Where transport occurs, supply moves to where transport begins — unless destination-country rules (OSS or distance selling) override the default.

- Intra-Community Commercial goods: A Polish seller dispatching goods to an Austrian entity zero-percentages the provision as an intra-Community transaction. The Austrian buyer self-assesses the acquisition charge in Austria at the local level and simultaneously recovers it as creditable input. No foreign VAT filing is required by either party.

- Intra-Community B2C goods: Since July 2021, a single union-wide threshold of €10,000 applies to distance sales of goods. Once a business’s annual cross-border B2C goods turnover across all destination member territories exceeds €10,000, the destination-country levels apply to all further consumer dealings. Compliance runs either through local registrations or the OSS.

- Goods entering from outside the bloc: provision occurs in the jurisdiction of entry. Import assessment is paid by the customs declarant at the frontier and recovered on the periodic return — unless a deferment mechanism applies (discussed in the third-country section below).

PROTECTED 0005 for Services — B2B and B2C Diverge Sharply

Wholesale provisions — the purchaser-location rule: The default place of supply is the customer’s jurisdiction. This single rule drives the reverse charge across the entire EU. A French agency invoicing a German GmbH for marketing services issues a zero-rated document; the GmbH self-assesses German imposition and recovers it simultaneously. No French registration, no German registration — the French agency.

Significant exceptions override the default: offerings related to immovable property are taxed where the property sits; passenger transport is taxed along the route; restaurant and catering delivery is taxed where the service physically occurs; short-term vehicle hire is taxed where the vehicle is put at the customer’s disposal.

B2C activities — the seller-country default: Fiscal charge ordinarily falls in the supplier’s jurisdiction. The commercially critical override is electronically supplied provisions (ESS), broadcasting, and telecommunications: since 2015 these are taxed in the consumer’s country from the first euro, regardless of where the supplier is established.

The €10,000 Threshold in Detail

The €10,000 union-wide threshold on cross border VAT EU B2C obligations combines both distance operations of goods and B2C digital services into a single annual calculation. Merchants whose combined cross-border B2C turnover stays below €10,000 in both the current and preceding calendar year may charge their home-country percentage on all European consumer exchanges. The moment the combined figure crosses the threshold, destination-country charges apply to every subsequent B2C exchange in that calendar year and the one following.

Critically, the threshold is not per-country — it is union-wide. A Dutch seller with €3,000 B2C items to Germany, €2,500 to France, €1,800 to Belgium, €1,400 to Italy, and €1,300 to Poland has already crossed €10,000 total and must apply destination-country percentages to every further European consumer deal that year.

B2B vs B2C VAT Treatment — Key Differences at a Glance

| Criteri | B2B (Taxable Person) | B2C (Private Consumer) |

| Who accounts for VAT | Buyer (reverse charge) | Vendor |

| VAT charged on invoice | No (zero-rated with VAT number) | Yes, at destination-country percentage |

| Registration trigger | VIES-validated VAT number provided | €10,000 union-wide B2C threshold |

| Filing mechanism | Home-country VAT return + EC Sales List | OSS (One Stop Shop) quarterly return |

| Place of supply | Buyer’s country | Vendor’s country (below threshold) / buyer’s country (above) |

| Invoice requirement | Full tax invoice with customer VAT number | Simplified invoice permitted |

| Proof burden | Vendor holds VIES confirmation | Vendor holds two non-contradictory location proofs |

Permanent Establishment and Its Effect on Cross Border Analysis

Place-of-output conclusions shift where a supplier holds a permanent establishment (PE) in the customer’s jurisdiction. A German company with a fixed establishment in France that serves French customers through that establishment is no longer making a cross-border supply of goods at all — the provision originates in France, French VAT applies, and the reverse charge is irrelevant.

Under Berkholz (C-168/84) and ARO Lease (C-190/95), PE in indirect tax purposes requires both human and technical resources in the member territory, operating with sufficient permanence to make outputs independently. Cloud hosting in another nation does not create PE. A warehouse staffed by a third-party logistics provider typically does not create PE unless the supplier retains operational control. A local sales office with authority to conclude contracts almost certainly does.

B2B VAT Rules and the Reverse Charge — When the purchaser accounts for Tax

The reverse charge is the operational backbone of international organisation commerce. Without it, every international sale between vendors would require the seller to obtain a foreign VAT filing, collect local tax, and remit it abroad — fragmenting the single market through administrative friction. Business-to-business VAT rules centred on the reverse charge eliminate that burden across most inter-company cross-border sales within the bloc.

How the Reverse Charge Operates in Practice

When a seller in one jurisdiction provisions services to a registered buyer in another, and the place of supply falls in the purchaser’s jurisdiction, the purchaser self-assesses the tax amount through the reverse charge. The seller issues a zero-rated invoice annotated “Reverse charge” (or equivalent in the buyer’s national language where required), displaying the buyer’s identification number. The buyer calculates charge at the local level, reports it as output tax, and simultaneously recovers it as creditable input — a net cash-neutral position to any fully taxable purchaser.

With a partially exempt organisation (a bank, insurer, or healthcare provider making both taxable and exempt supplies), the reverse charge is not cash-neutral. Input-input recovery is limited to the taxable-use proportion. A German insurer receiving reverse-charge invoices on services that are 80% attributable to exempt supply will recover only 20% of the reverse-charge VAT — a real cost that needs to be factored into commercial pricing negotiations.

Triangulation — Three Countries, Two Transactions, One Simplified Reporting Path

Triangular deals deserve detailed attention because they generate disproportionate compliance failures relative to their frequency. In a triangulation arrangement, Company A (established in country X) sells goods to Company B (established in country Y), who on-sells them to Company C (established in jurisdiction Z), with the goods transported directly from X to Z. Country Y — the “middle” company — never takes physical possession.

Without simplification, Company B would need an enrolment in both country X (to acquire the goods) and jurisdiction Z (to make a domestic delivery to Company C), creating two registration obligations purely from the position in the output chain.

EU simplification rules under Article 141 of Directive 2006/112/EC allow Company B to avoid both registrations, provided:

- All three parties are registered in different member nations

- The goods move directly from X to Z

- Company B issues an invoice to Company C with the annotation “Triangular dealing — reverse charge”

- Company B includes the operation in its EC Sales List with the “T” indicator

Company C self-assesses the acquisition assessment in jurisdiction Z. Company B reports the sale in its EC Sales List but pays no imposition in any country on the exchange. The annotation on the invoice is mandatory — omitting it disqualifies the simplification and creates an immediate registration obligation on Company B in jurisdiction Z.

Call Off Stock — The 2020 Quick Fix

Related to triangulation but distinct from it, call-off stock arrangements arise when a supplier moves goods to a warehouse in another jurisdiction, where they sit until a specific known customer collects them. Before the 2020 Quick Fixes (applied from 1 January 2020), this movement typically triggered a deemed intra-Community supply by the seller — requiring registration in the warehouse member state.

The Quick Fix simplification eliminates that registration requirement where:

- The supplier is not established in the destination member state

- The customer is identified before goods leave the dispatch state

- the merchandise is transferred to the customer within 12 months of arrival

- The supplier maintains a register of call-off stock movements

Both parties must record the arrangement, and the customer’s identification number must be verified before the goods depart. Failure to satisfy any condition collapses the simplification retroactively to the date of movement, generating an immediate registration obligation and potential penalties.

Zero Rating Requires Documentary Proof

Zero-rating an intra-Community Inter-company goods deal is conditional, not automatic. The seller must hold evidence goods physically left the dispatch member state and entered another. Under the 2020 Quick Fixes, a rebuttable presumption applies where the seller holds two non-contradictory documents from independent parties confirming transport — such as a signed CMR note plus a customs exit record, or carrier documentation plus insurer confirmation of delivery.

The zero-rating doesn’t work if there isn’t enough proof of transport. The seller owes the amount at the domestic percentage, plus interest from the filing date, plus penalties. The Teleos ruling (C-409/04) remains the ECJ’s definitive statement that good faith does not excuse evidentiary gaps. Supplying parties accepting buyer confirmation as sole proof of dispatch — particularly with high-value electronics, pharmaceuticals, and other carousel-fraud-targeted goods — carry significant exposure.

Domestic Reverse Charge for Sector Specific Fraud Prevention

Beyond the cross-border reverse charge, many member tax authorities operate domestic reverse-charge mechanisms targeting sectors historically targeted by organised carousel fraud. These apply to sales between entities within the same member state — not cross-border — and exist independently of the standard intra-Community framework.

The sectors most commonly covered across territories include: construction and installation services (mandatory in Germany, Italy, Belgium, and others), wholesale deliveries of mobile phones, tablets, and laptops (applicable where a firm-to-enterprise supply of goods exceeds a per-sale threshold), trading in greenhouse gas emission allowances, electricity and gas supplied through networks to reseller companies, and certain agricultural products in some jurisdictions.

Germany’s domestic reverse charge for construction services under §13b UStG applies when a construction contractor goods and services to another contractor whose own turnover from construction activities exceeds 10% of total revenue. The supplier issues a zero-rated domestic invoice. The recipient self-assesses VAT at the German standard rate. Contractors who receive a reverse-charge invoice but do not qualify as “construction firms” under the threshold face the full levy from their supplier — the threshold determination matters.

Italy’s domestic reverse charge (reverse charge interno) covers not only construction but also electronics, precious metals, and certain food commodities. The scope of Italian domestic reverse charge has expanded incrementally since 2015 through a series of budget laws, and sectors covered in Italy are not uniformly covered in other jurisdictions.

Enterprises operating in affected sectors across multiple European jurisdictions must maintain separate invoice logic covering domestic items in each jurisdiction: some dealings between the same trader types require normal invoicing in one jurisdiction and reverse-charge invoicing in another. A construction group with operating entities in Germany, France, and the Netherlands applies a different domestic reverse-charge rule in each jurisdiction covering intercompany outputs within the group, even on the same service type.

The operational impact on any entity with a presence in multiple European markets is that “domestic” does not mean “simple.” The domestic reverse-charge rules layer additional sector-specific logic onto an already complex international framework.

B2C VAT and the One Stop Shop — Threshold, Registration, and Filing

Before July 2021, a Dutch retailer selling physical merchandise to consumers in 22 member countries with meaningful volumes needed separate registration in most of them—filing local returns on local schedules, paying in local currencies, managing correspondence in local languages, and tracking 22 sets of filing deadlines simultaneously. The compliance burden was so severe that most small and mid-market operators either restricted themselves to their home market or quietly ignored foreign obligations until audit pressure arrived.

OSS enrolment and What It Covers

OSS allows a single registration in the seller’s home state to cover all EU B2C VAT obligations across:

- intra-Community distance operations of goods dispatched from EU warehouses to consumers in other jurisdictions

- B2C provisions of services taxable in the consumer’s country (including all electronically supplied services, telecommunications, and broadcasting)

- Certain domestic deliveries of goods facilitated by electronic interfaces

Under OSS, one quarterly return lists sales by destination state at that jurisdiction’s level. One payment goes to the home authority, which distributes funds to receiving-country authorities. The entire multi-country filing burden compresses to four return submissions per year.

Rate Complexity Under OSS

Correctly applying destination-country levels is the most operationally demanding aspect of OSS compliance. Standard charges range from 17% (Luxembourg) to 27% (Hungary). Beyond standard percentages, 27 member territories maintain their own reduced, super-reduced, and zero-rate schedules of specified goods and service categories. Ireland zero-levels children’s clothing that France taxes at its standard 20% rate. Germany applies a reduced 7% rate to printed books while applying 19% to ebooks (a disparity several member nations have recently closed by adopting reduced digital rates under the 2022 Directive amendment).

A product catalogue of any meaningful size requires automated rate determination — not a spreadsheet. Rate changes in member jurisdictions do not follow a predictable schedule, and a rate correct in January may be incorrect by September if a member state implements a budget-driven adjustment. Tax technology vendors maintain live rate databases updated continuously precisely because of this.

IOSS — Import One Stop Shop for Low Value Consignments

The IOSS covers goods imported from outside the bloc to European consumers where the consignment’s intrinsic value does not exceed €150. Without IOSS, the consumer faces import levy at delivery — unexpected charges, delays, friction, returns — a customer experience that measurably depresses conversion and repeat purchase rates.

With IOSS, the seller collects levy at checkout at the destination-country rate, files monthly IOSS returns, and remits centrally. The IOSS number on the parcel triggers accelerated customs clearance without additional payment at delivery. Consumers receive goods with no surprises.

Non-vendors in the bloc must appoint an locally established intermediary under IOSS in most jurisdictions. The intermediary bears joint and several liability under the levy declared, which makes the selection more than a cost decision — the intermediary’s processes to reconcile IOSS declarations against parcel manifests must be operationally sound. Discrepancies between declared dealing values and customs-declared consignment values attract audits from both tax and customs authorities simultaneously.

OSS vs IOSS vs Local Registration — When to Use Each

| Scheme | Covers | Threshold | Filing | Excludes |

| OSS (Union) | B2C goods dispatched from EU; ESS, digital, and electronic outputs to EU consumers | €10,000 union-wide B2C turnover | Quarterly, one return | Goods already in buyer’s country; installation supplies; new means of transport |

| OSS (Non-Union) | B2C digital/electronic outputs to EU consumers by non-EU vendors | None | Monthly, one return | Goods; marketplace-facilitated supplies |

| IOSS | None | Monthly, one return | Goods >€150; excise goods; inter-company imports | |

| Local registration | Domestic supplies from foreign warehouse; installation; new vehicles to consumers | Per-country return schedule | Per-country return schedule | Cannot be replaced by OSS/IOSS |

When OSS Is Not Sufficient — Scenarios Requiring local enrolment

OSS removes the need to multi-country registration in the vast majority of cross-border B2C scenarios, but it does not cover every provision type. Several situations still require a direct local enrolment in a specific member state:

- merchandise

Understanding where OSS ends and local enrolment begins is one of the most commercially consequential distinctions in cross-border tax planning. Vendors assuming OSS covers all consumer deals internationally can build significant local-registration obligations without realising it, particularly as they expand product lines and add foreign warehouse capacity.

B2B Ecommerce — Digital Goods, Platforms, and the Deemed Supplier Model

Commercial e commerce taxation follows the same reverse-charge framework as offline services when the buyer is a verified taxable person. Complexity arises at the intersection of platform intermediation, non-European seller populations, and the 2021 deemed-supplier rules that shifted liability for certain consumer sales from underlying merchants to the platforms facilitating them.

Defining Electronically Supplied Services

Community Regulation 282/2011 (as amended by 1042/2013) defines electronically supplied services (ESS) as services delivered over the internet or electronic network, essentially automated, involving minimal human intervention. The category covers software licences and SaaS subscriptions, digital content (music, games, films, ebooks), website hosting, automated data processing, cloud infrastructure, and automated distance learning.

Services are not ESS merely because delivery happens electronically. Consulting, legal work, accounting, and creative activities delivered by email involve material human input — they fall under general service place-of-output rules, not the ESS destination-country rule. For Wholesale e commerce operators with mixed service portfolios, correctly categorising each service type is prerequisite to correct rate determination.

The Deemed Supplier Rules — Structural Change for Platforms

Article 14a of the amended Directive makes an electronic interface (marketplace, platform, or similar) the deemed supplier — liable to collect and remit tax — in two scenarios:

- Imports under €150: Where a marketplace facilitates distance sales of imported merchandise to European consumers, consignment value not exceeding €150, the platform is deemed the supplier. The underlying seller makes a Business-to-business supply of goods to the platform (outside the scope of, or levy-zero-rated). The platform makes the B2C provision to the consumer and holds the IOSS or standard filing obligation.

- non-European seller goods already in the bloc: Where a marketplace facilitates items of goods (no value cap) by non-European-established supplying parties to European consumers, and the merchandise is already physically located within the bloc at point of sale, the platform is again the deemed supplier regardless of consignment value.

locally established vendors are explicitly excluded from both scenarios — they retain their own tax obligations on sales through platforms. This cross-border asymmetry creates a structurally unequal compliance burden the European Commission monitors through the DAC7 directive on platform data-sharing, effective as of 2023.

DAC7 — Platform Reporting to fiscal authorities

From 1 January 2023, the DAC7 directive requires digital platforms to collect, verify, and annually report to their home-country fiscal authority detailed data about suppliers using their service — including total consideration received, bank account details, tax identification numbers, and the number of dealings completed. Authorities share this data with member-state counterparts under automatic exchange arrangements.

For sellers on platforms, DAC7 means fiscal authorities in their home jurisdiction receive a report of their platform income directly from the marketplace. Sellers who have not declared this income face automatic cross-checks. For platforms, DAC7 adds a substantial data-collection and reporting obligation that layers on top of the deemed-supplier filing rules.

PROTECTED 0024 and the Movement Rule

In chains involving more than two parties — where goods move through multiple intermediaries before reaching the end buyer — only one operation in the chain can be the intra-Community supply (zero-rated). All other operations in the chain are treated as domestic supplies in either the dispatch or destination state.

Determining which exchange constitutes the intra-Community supply depends upon who organises (and bears risk for) the transport. Where the first supplier arranges transport, the first deal is the intra-Community supply. Where an intermediate party arranges transport, the first sale is domestic (in the dispatch state) and the intermediate party makes the intra-Community supply to the final buyer.

Getting this analysis wrong in a multi-party chain means the wrong entity zero-rates its delivery, and both the entity which should have zero-rated and the one which did so incorrectly face potential reassessment from their respective fiscal authorities.

PROTECTED 0026 VAT Verification — VIES, Valid Numbers, and Due Diligence

Confirming a buyer holds a valid identification number is necessary but not sufficient. The number must be current, belong to the actual counterparty, and be verified at the correct point in the dealing lifecycle. The business to business verification process — treated as a box-ticking exercise by many operations teams — is where systematic compliance failures build silently over time.

VIES — Capabilities and Limitations

VIES queries the registration databases of all member countries and returns a live confirmation of number status. Available at ec.europa.eu/taxation_customs/vies/, it accepts number and country prefix and responds with valid/invalid/not-found within seconds under normal conditions.

VIES confirms number status, not counterparty identity. A VIES-positive result does not confirm: the entity presenting the number is the entity registered against it. On high-value supplies, due diligence extends to cross-referencing the number against national company registers — the German Unternehmensregister, French Registre des commerces, Dutch Kamer van Koophandel — to confirm name, address, and legal status match what the buyer declared.

When VIES Returns No Result

“Not found” does not conclusively establish that a number is invalid. National VIES feeds update about varying schedules — some overnight, some with 48-hour delays, some with longer gaps around public holidays or system migrations. Recent registrations, temporarily suspended registrations, and format errors in the query itself all produce not-found results.

The correct business to business process on receiving no result:

- Retry within 24 hours, with the format double-checked against the jurisdiction-specific pattern.

- Request domestic confirmation from the buyer — official registration certificate or fiscal authority letter.

- Query the national register directly where accessible.

- Document every step and the result of each.

Pending confirmation, treat the operation as B2C: collect and remit destination-country levy. Issue a credit note and corrected Inter-company invoice once the buyer’s status is confirmed. The correction process is straightforward. Defending a position of having applied reverse charge with no VIES record is not.

Continuous Revalidation for Subscription Businesses

Initial onboarding validation addresses the buyer’s status at account creation. Registration status changes over time — entities deregister voluntarily, have registrations suspended due to non-compliance, or restructure through mergers and dissolve the original legal entity.

For SaaS, professional activities, and any business model with recurring revenue from Commercial customers, a quarterly VIES re-validation run across the active customer base identifies status changes before they accumulate into a compliance backlog. Automated re-validation integrated with the billing system — flagging accounts whose numbers have changed status and queuing them pending account-team review — handles this at scale without manual intervention.

Format Validation at Point of Entry

Format errors are among the most preventable sources of VIES query failures. each jurisdiction uses a distinct number structure: Germany’s Umsatzsteuer-ID follows DE plus nine digits, France’s Numéro de TVA follows FR plus two characters plus nine digits, Ireland’s follows IE plus eight characters. The European Commission publishes format specifications per jurisdiction, and libraries to validate programmatic formats exist across every major programming language.

Enforcing format validation at the point of number entry — in the checkout form, the CRM field, the ERP onboarding screen — catches transposition errors, missing prefixes, and extra characters before they generate failed VIES queries downstream.

API Based Validation at Scale — Integrating VIES Into Your Transaction Flow

Manual VIES queries work in low-volume operations where a compliance officer checks each new customer. At any meaningful exchange volume, manual validation is not viable — the human bottleneck creates delays in order processing and, more critically, creates gaps in validation coverage during busy periods.

The European Commission exposes a VIES SOAP API and, from 2022, a REST API endpoint, allowing programmatic validation of registration numbers in real time. Integrating the VIES API directly into your checkout, CRM, or ERP means every new buyer record triggers an automated validation at the point of creation. The API response — valid, invalid, or unavailable — is written to the customer record as a timestamped field. That field governs the tax treatment applied to all subsequent exchanges on that account.

Several tax technology platforms offer better VIES integration with fallback logic. If the official VIES API returns a service-unavailable response (which happens during high-traffic periods or maintenance windows), the platform sends the query to a mirrored or cached validation database, marks the result as “validated via cache,” and queues the number pending re-validation against the live API within 24 hours. This avoids blocking transaction processing during VIES downtime while maintaining the documentary integrity of the validation record.

Companies with global customer bases run VIES validation alongside equivalent checks covering other jurisdictions: UK HMRC’s online registration number checker, the Australian Company Register to validate ABNs, and Norwegian Brønnøysund register covering Norwegian org numbers. A single validation middleware layer routing each number to the appropriate national authority’s API and returns a unified status signal simplifies the integration burden across multi-market operations.

Retention of validation records is non-negotiable. Every VIES validation response should be archived against the transaction or account record it relates to, with the query date, the number queried, the jurisdiction prefix, and the response status. These records form the first line of defence in any audit examination of reverse-charge classification decisions.

B2B B2C supplies in Mixed Operations — Segmenting Your Customer Base for Compliance

A software company might licence its platform to enterprise clients on annual Wholesale contracts while simultaneously running a self-serve tier where freelancers, students, and unregistered firms purchase through a standard checkout. A food producer might sell to wholesalers and restaurant chains (Business-to-business sales) while operating a direct-to-consumer channel through its own website. Inter-company B2C supplies within a single commercial operation multiply the compliance surface area — and most cross-border filing errors originate not in the rules themselves but in the failure to separate these two streams cleanly at the transaction level.

Classification Must Precede Tax Calculation

Every rate determination runs downstream of customer classification. A seller who calculates levy before confirming buyer status is working backwards. The classification event — does this buyer have a verified registration number — determines which rate engine applies, which invoice template is generated, which return receives the entry, and which documentation is retained.

Commercial B2C supplies processes deferring classification to post-sale reconciliation accumulate errors at a rate proportional to order volume. The correction cycle — credit notes, amended invoices, return adjustments — consumes more resource than building correct classification into the front-end flow in the first place.

Three Architectural Approaches

Separate checkout flows: Wholesale and B2C checkout run on distinct journeys. The Business-to-business flow requires an enrolment number, validates against VIES before allowing order confirmation, and routes confirmed transactions to the reverse-charge engine. The B2C flow collects destination state and applies the OSS rate matrix. The boundary between flows is enforced technically, not procedurally.

Account-level classification: covering subscription and repeat-purchase enterprises, classification is set at account creation and governs all subsequent transactions until explicitly updated. The account record holds customer type, the registration number, the VIES validation timestamp, and the review date pending re-validation. Billing logic reads from the account record. Status changes trigger automated review workflows rather than ad-hoc corrections.

ERP-integrated rate determination: Large organisations running SAP, Oracle, or Microsoft Dynamics centralise tax determination in a dedicated engine (Vertex, Avalara, Fonoa, or similar) that receives customer status from the ERP master record and applies the appropriate rules in real time. The return is generated from ERP transaction data rather than assembled separately. This architecture requires rigorous master-data management — a customer record with the wrong classification tag produces systematically incorrect invoices at volume.

Record Retention and Audit Trail Architecture

Every international transaction in a mixed-operation firm generates an audit trail supporting reconstruction on demand. For Inter-company transactions: customer registration number → VIES validation record with timestamp → invoice bearing the number and reverse-charge annotation → EC Sales List entry (where applicable) → VAT return line. For B2C transactions: customer country → rate determination log → invoice carrying rate and tax amount → OSS return line with destination state.

Member-state retention requirements vary: 10 years in Germany, 10 years in Italy, 7 years in France, 5 years in Sweden. Traders registered in multiple jurisdictions observe the longest applicable period across all registrations covering their complete transaction archive. Digital record-keeping — cloud-based document management with indexed search — is effectively mandatory across any operation exceeding a few hundred monthly transactions.

Pricing Strategy in Mixed B2B and B2C Markets

Levy treatment directly affects pricing architecture in mixed-market vendors. B2B recipients in the bloc are typically quoted prices exclusive of levy — they will self-assess or recover it, so the gross figure they pay equals the net invoice amount. B2C acquiring parties see the VAT-inclusive price: the consumer pays the full levy-loaded amount with no recovery mechanism.

This creates a fundamental structural question to any enterprise selling the same product to both audiences: do you publish one price (and apply or not apply the rate depending on buyer status at checkout), or do you publish separate B2B and B2C price lists?

Publishing a single ex-levy price and adding levy at checkout is clean to B2B purchasers across borders — the price is always the same net figure, and the VAT treatment adjusts based upon customer status. The complication is B2C display: many member territories require consumer-facing prices to be displayed levy-inclusive. A seller with both B2B and B2C checkouts running from the same product catalogue may need to render prices differently depending on which checkout the customer is using — net in trader flows, gross in consumer flows.

Subscription entities face a further variant: a customer who upgrades from a B2C individual plan to a B2B corporate plan mid-cycle needs their billing revised retroactively or prospectively. If the switch happens mid-subscription period, the VAT treatment covering the remaining period changes. Prorated credits on over-collected charge on the B2C side and re-invoicing on B2B terms for the new period must be handled correctly in both the billing system and the underlying return data.

The commercial risk in pricing mixed operations incorrectly cuts both ways: under-pricing the levy-inclusive consumer tier means the entity absorbs the cost from margin; over-pricing the B2B tier (by adding the levy that should be reverse-charged) makes products unnecessarily expensive to organisation buyers and generates invoices B2B buyers reject as non-compliant.

Cross Border Trade with Third Countries — Exports, Imports, and input recovery

the bloc’s internal market rules address cross-border transactions. A substantial share of cross border trade affecting European companies involves non-non-European counterparties — the United Nations, the United Kingdom post-Brexit, Switzerland, Norway, Singapore, Japan, and Gulf markets. These transactions interact with union filing rules through customs, import procedures, and the place-of-output framework of services, each with specific compliance requirements.

Exports from the bloc

Goods exported to non-European buyers are zero-rated at the bloc exit point. direct liability is extinguished on the basis that consumption occurs outside the common tax area. The seller charges nothing and owes nothing on the supply of goods — but the zero-rating requires customs export documentation to support it.

Required evidence: the Export Accompanying Document (EAD) carrying the Master Reference Number (MRN) from the bloc’s electronic export control system, plus freight documentation confirming departure (typically a signed CMR for road, bill of lading for sea, or air waybill for air freight). fiscal authorities request these documents during audit. Sellers who zero-rate exports without retaining the MRN and transport evidence face reassessment at the domestic rate throughout the undocumented period.

Services to non-B2B customers are generally outside scope — the place of supply is the customer’s jurisdiction under the general rule, taking the transaction entirely outside the union fiscal system. Services to non-European consumers may still attract EU levy depending on service type and supplier establishment — electronically supplied services consumed by non-European consumers by non-European-established suppliers fall outside EU levy, but an locally established supplier invoicing non-European consumers for ESS should confirm whether OSS covers the provision or whether a local rule applies.

Imports into the bloc — Levy and Cash Flow

Cross border trade from outside the bloc generates import levy in the jurisdiction of entry. Levy is calculated on the customs value (transaction value plus cost of transport and insurance to the bloc border) at the destination-country rate. Commercial importers face a cash-flow gap between payment at customs and recovery on the periodic return — a gap that can extend to 60 days or longer in member jurisdictions without deferment mechanisms.

The Netherlands Article 23 permit eliminates this gap: permit-holders self-assess import VAT directly on their Dutch return with simultaneous recovery, producing zero net cash impact. Belgium, Italy, Poland, and Austria operate equivalent deferment regimes with varying eligibility conditions. Firms selecting their EU import hub should weight these deferment mechanisms alongside warehouse costs, logistics infrastructure, and labour market access — the cash-flow saving on import VAT deferment can be material on high-turnover importers.

UK and EU Cross Border Trade After Brexit

From 1 January 2021, the UK is a third country for customs and VAT purposes. Goods crossing the GB-EU border are subject to customs formalities and potentially tariffs in both directions, plus import levy at entry. For goods meeting the Trade and Cooperation Agreement (TCA) rules of origin (broadly: sufficient processing or transformation within the UK or EU), tariffs are eliminated — but customs declarations remain mandatory and documentary burden persists.

UK enterprises supplying services to B2B clients continue to issue zero-rated invoices (from the UK perspective) or invoices outside scope, with European clients self-assessing under the general B2B rule. UK traders supplying services to European consumers must register under the non-Union OSS in a single state of their choice to collect and remit EU levy on consumer transactions. There is no UK registration equivalent — each European consumer transaction generates a foreign-country obligation until the non-Union OSS is in place.

Fiscal Representatives

Several member states require non-European vendors registering in VAT terms locally to appoint a fiscal representative — a locally established entity assuming joint and several liability under the tax obligations of the foreign registrant. Italy, Spain, and Greece maintain mandatory fiscal-representative requirements of non-European registrants. Germany, France, the Netherlands, and others have removed the requirement for entities established in countries with which the bloc has levy cooperation agreements, though many UK entities (post-Brexit) fall back into the mandatory-representative category depending on the member state.

Fiscal representative fees are commercial, typically structured as an annual retainer plus a per-return charge. The representative’s liability exposure means reputable representatives apply rigorous KYC and compliance conditions on their clients — new tax registrations in mandatory-representative jurisdictions take longer to establish than simple local registrations in non-mandatory countries.

Customs Duty and Import Levy — Combined Liability on Inbound Goods

Import levy does not arrive alone. Goods entering the bloc from non-European origins face both customs duties and import VAT, calculated on related but distinct bases.

Customs duty applies to goods at the rate specified in the Combined Nomenclature

(CN) on the commodity code, applied to the customs value of the goods. For goods meeting TCA rules of origin between the UK and EU, or preferences under the bloc’s trade agreements with third countries (Japan, Canada, South Korea, Vietnam, and others), the applicable duty rate may be reduced to zero — but the rules-of-origin documentation (typically a declaration of origin or EUR.1 movement certificate) must accompany the shipment. Missing documentation means standard third-country duties apply at the border, recoverable in theory through post-clearance amendment applications but practically difficult and time-consuming to reclaim.

Import levy is then calculated on the customs value plus the customs duty amount plus the cost of transport and insurance from the frontier to the destination within the bloc. This “levy basis” is therefore higher than the customs value alone: a consignment with a customs value of €10,000, subject to 5% customs duty of €500, transported at an internal EU freight cost of €300, generates an import taxable base of €10,800. At a 21% Dutch rate, import VAT totals €2,268 — remitted to customs and recovered on the Dutch return.

Businesses on tightly controlled landed-cost budgets will find the interaction between duty and indirect-tax rates across different commodity codes can be significant in product and sourcing decisions. A product with a 12% customs duty rate carries a higher import taxable base than an identical product that qualifies for 0% under a preference agreement — even at the same declared value.

Recovery of levy on EU Expenditure by Non European businesses

Non-European entities incurring EU levy on business expenses — exhibition fees, hotel accommodation, professional activities, trade fair costs — can reclaim it through the 13th Directive refund procedure. Each claim is filed with the fiscal authority of the jurisdiction where the expenditure arose, using that authority’s prescribed form and supporting documentation. Deadlines: 30 June of the year following the expenditure year across most member states.

Processing times vary from three months (Netherlands, Germany) to over twelve months (Italy, Spain). Some member states require reciprocal arrangements before accepting 13th Directive claims — the US, for example, which does not operate a federal fiscal system, has limited reciprocity with most member states, making US businesses’ 13th Directive refund applications subject to additional scrutiny in several jurisdictions.

B2B Sales Compliance — Filing Obligations, Penalty Exposure, and Audit Readiness

Every B2B sale that crosses a border generates a filing obligation somewhere. Return cycles, EC Sales Lists, Intrastat statistical reports, OSS and IOSS declarations — all flow from the same underlying transactions, on different schedules, through different systems, with different consequences when they contain errors. The compliance architecture for B2B sales across jurisdictions needs to be understood as an interconnected system, not a set of independent obligations.

Return Frequencies and the Multi Jurisdiction Filing Calendar

Return frequency ranges from monthly (Germany mandates monthly returns on new enrolments and where registrants exceed €7,500 monthly VAT liability) to quarterly (default in most member states) to annual (low-turnover concessions in a minority of jurisdictions). A business registered in Germany, France, the Netherlands, Poland, and Italy manages five different return schedules — monthly German returns, quarterly French and Dutch returns, quarterly Polish returns, and quarterly Italian returns — each with its own deadline, filing format, and payment mechanism.

OSS returns are quarterly, due by the last day of the month following each calendar quarter (30 April, 31 July, 31 October, 31 January). IOSS returns are monthly, due by the last day of the following month. These deadlines are fixed. Persistent late OSS or IOSS filing results in compulsory exclusion from the scheme, carrying a two-year mandatory waiting period before re-registration. Exclusion means reverting to individual member-state registrations covering all previously OSS-covered supplies — a compliance burden multiplier making consistent on-time OSS filing a business-critical process.

EC Sales Lists — What Goes In Them and When

EC Sales Lists (recapitulative statements) must be filed by sellers of goods making intra-Community zero-rated supplies. Each list entry records the buyer’s registration number, the total value of supplies to that buyer in the period, and a triangulation indicator where applicable. Returns are typically quarterly but become monthly in member states where intra-Community supply values exceed a threshold — in Germany, the threshold is €50,000 per quarter in the current or preceding quarter.

Some member states (Germany among them) require EC Sales Lists covering cross-border B2B services subject to the reverse charge — not only goods. This is an area of union-level fragmentation: several member states have no ESL obligation on services while others maintain full reporting. Businesses making significant cross-border B2B services sales need to check the specific requirements of each registration jurisdiction separately.

E Invoicing and Digital Reporting — The Next Compliance Wave

The European Commission’s ViDA proposal (VAT in the Digital Age, published December 2022, with phased implementation planned from 2025 to 2028) will introduce mandatory digital reporting and e-invoicing requirements across the bloc. Under ViDA:

- From 2028, structured e-invoices using the EN16931 standard will become mandatory covering all intra-Community B2B transactions

- Near-real-time reporting of transaction data to a central EU platform will replace EC Sales Lists and Intrastat covering intra-Community B2B supplies

- Member states will gain the right to extend mandatory e-invoicing to domestic B2B transactions without requiring separate EU derogation

- Several member states are ahead of the union-wide schedule: Italy has operated mandatory B2B e-invoicing (Fattura PA / Fattura B2B via SDI) since 2019, Poland introduced the KSeF voluntary system in 2022, with mandatory implementation deferred to 2026, France is phasing in mandatory e-invoicing from September 2026, and Romania introduced mandatory e-Factura covering B2B transactions above certain values from 2024.

Businesses building filing compliance infrastructure today need to accommodate e-invoicing mandates in their technology roadmap. An ERP integration working in current return-based compliance may need significant modification to support near-real-time transaction reporting.

Penalty Regimes — Country by Country

| Country | Late filing | Late payment interest | Understatement | Fraud / deliberate omission |

| Germany | €25/month, max 10% of VAT due | 1.8% per year | 50%–400% of underpaid amount | Criminal prosecution possible |

| France | 5% (10% after 30 days) | 2.4% per year (0.2%/month) | 40% surcharge | 80% surcharge |

| Italy | 30% standard | 3%–4% per year | 90%–180% of underpaid amount | 240%–480% on omitted declaration |

| Poland | 30% standard | Statutory interest | 30% understatement; 100% on invoice fraud | Mandatory split payment on inter-company invoices >PLN 15,000 |

| Spain | 1%–20% depending on delay | 3.75% per year | Up to 150% of underpaid amount | Criminal referral above certain thresholds |

Standard Audit Files and Ledger Level Digital Reporting

Standard Audit file Tax (SAF-T) is a mandatory digital reporting requirement operative in several member states, with expansion underway. SAF-T requires businesses to provide their complete accounting ledger — or a standardised extract of it — in machine-readable XML format on demand from tax authorities, typically during audit. The data set covers all sales transactions, purchase transactions, general ledger entries, and in some versions fixed-asset registers and stock data.

Poland was among the first member states to make SAF-T mandatory, introducing JPK (Jednolity Plik Kontrolny) from 2016 for large firms, extended to all businesses from 2018. JPK in Poland is not merely an on-demand audit file — it is a monthly mandatory submission. Polish businesses submit their entire sales and purchase ledger in JPK format every month, alongside (or instead of, for micro-entities) the periodic return. Polish fiscal authority systems run automated cross-checks between the JPK data submitted by sellers and the JPK data submitted by their buyers, identifying mismatches in declared values, dates, and fiscal amounts.

Romania introduced SAF-T (D406) mandatory reporting from 2022 for large taxpayers, extended to medium and small taxpayers in subsequent phases. Hungary adopted real-time invoice reporting (RTIR) from 2018, requiring businesses to upload the data of every B2B invoice above HUF 100,000 to the national authority’s systems within 24 hours of issuance.

Businesses with operations in these jurisdictions treat SAF-T compliance as much a technology question as a fiscal one. Accounting systems must export data in the prescribed national format, with field mapping matching the authority’s schema exactly. Errors in field mapping, character encoding, or data completeness result in rejected submissions — and rejected submissions count as non-filings on penalty grounds in most jurisdictions.

The European Commission’s ViDA proposal envisions an union-level equivalent: real-time transaction reporting feeding into a central data repository, ultimately replacing EC Sales Lists and Intrastat with near-continuous data exchange. Businesses investing in compliance technology today need systems flexible enough to accommodate this evolution without a complete rebuild in 2028.

What Auditors Target

Cross-border B2B VAT EU audits consistently focus upon five areas:

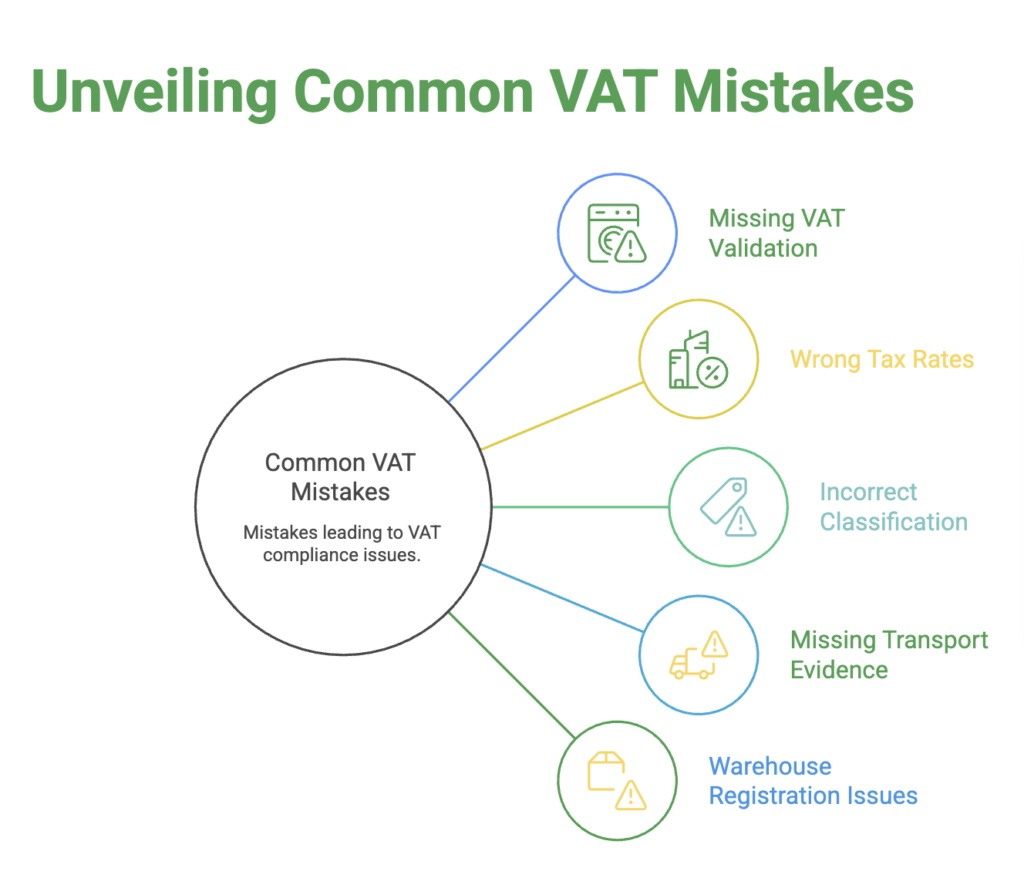

Zero-rated intra-Community goods supplies without transport documentation. The single most common audit finding in goods-trading businesses. Contemporaneous documentation means documents obtained before the return is filed — not recreated on audit request.

Reverse-charge services invoices where VIES validation records are absent. Auditors request the validation log alongside the invoice file. An invoice annotated “reverse charge” with no associated VIES timestamp is treated as undocumented zero-rating and assessed at the seller’s domestic rate.

OSS declarations with incorrect destination-country rates. Destination-country tax authorities receive OSS data from the filing member state and cross-check declared rates. Rate discrepancies generate automatic correction notices from multiple jurisdictions simultaneously.

Triangulation transactions lacking the mandatory “T” indicator on EC Sales Lists or the required invoice annotation. Missing indicators disqualify the simplification retroactively, creating registration obligations on the middle company in the destination state.

Intrastat filings missing or materially inconsistent with EC Sales List values. Reconciliation between the two data sources is a standard audit procedure. Unexplained discrepancies between the values of intra-Community goods movements in Intrastat and EC Sales Lists attract detailed examination of underlying transaction records.

Practical B2B and B2C VAT Scenarios That Expose Common Compliance Gaps

The rules in the preceding sections operate cleanly in simple scenarios. Real operations generate complications.

Scenario 1 — The B2B Software Company That Launches a Consumer Tier

A German software business has always sold enterprise licences to registered entities under the reverse charge. Its B2B transactions are clean. It launches a self-serve plan targeting freelancers and small operators — monthly billing, no sales team, checkout handles everything.

Within six months, self-serve revenue from 18 member states totals €180,000. Most buyers have not provided registration numbers. The business has been zero-rating all self-serve revenue. It has not enrolled in OSS. The combined cross-border B2C turnover crossed €10,000 in month two of the new product.

The exposure: sixteen months of under-collected destination-country levy on approximately €180,000 of consumer revenue across 18 jurisdictions. Penalties range from minor (Sweden, Netherlands) to severe (Italy). The most material jurisdictions — France and Germany — will each account with the largest volumes given population and digital services adoption rates.

The corrective path: voluntary OSS enrolment, calculation of the historical underpayment by destination state, voluntary disclosure to the three or four member states with the highest exposure, and immediate implementation of a checkout that requires VIES validation before the reverse-charge route is permitted.

Scenario 2 — The Marketplace That Did Not Read the 2021 Reform

A French marketplace connects craft sellers from Ukraine, Morocco, and the US with European buyers. The platform processes approximately 40,000 consignments per year, most under €150. It has not reviewed the deemed-supplier implications of the 2021 reform. Sellers believe they are liable to their own levy.

Under Article 14a, the marketplace is the deemed supplier on every consignment by non-sellers in the bloc under €150. It has been the IOSS-liable party since July 2021 without knowing it. The individual sellers have no EU filing obligation on these supplies — it has already been legally reassigned to the platform.

The exposure covers three-plus years of transactions. IOSS was not registered. no VAT was collected at checkout. The platform has no parcel-level transaction data in an IOSS-compatible format. Reconstruction requires cross-referencing order records against shipping manifests by destination state and date.

The resolution timeline: IOSS enrolment, retroactive assessment of the underpayment, voluntary disclosure, and a seller onboarding overhaul that documents establishment status covering every seller on the platform.

Scenario 3 — The Manufacturer Using Pan European Fulfilment

A Dutch household goods manufacturer sells products to European consumers through its own website. It has enrolled in OSS in the Netherlands, correctly applying destination-country rates to all distance sales. After negotiating a logistics contract with a third-party warehouse operator running facilities in Germany, France, and the Czech Republic, it moves inventory to all three warehouses to reduce delivery times.

From the moment merchandise crosses into the German, French, and Czech warehouses, the manufacturer has made deemed intra-Community supplies from the Netherlands — potentially triggering acquisition VAT registrations in each of the three countries. More importantly, merchandise sold to consumers from the German warehouse are no longer distance sales dispatched from the Netherlands. They are domestic supplies from Germany. OSS does not cover domestic supplies. The manufacturer needs German, French, and Czech registrations to legally self-assess the charge on sales dispatched from those warehouses.

The manufacturer continues filing OSS returns assuming full coverage. over two years, all sales from the foreign warehouses are reported through the Dutch OSS return as distance sales — incorrectly. German, French, and Czech authorities receive OSS data referencing Dutch dispatch on transactions that originated in their own jurisdictions. The discrepancy surfaces during a German audit triggered by a customs cross-check on the warehouse inbound movements.

The exposure: two years of domestic supplies in Germany, France, and the Czech Republic reported through the wrong mechanism. Penalties in all three jurisdictions. The additional obligation to retroactively register in all three countries and file corrective local returns. The commercial impact of retracing each affected transaction to determine the correct local rate — which across certain household goods categories differs from the Dutch rate applied through OSS.

The preventive action: any logistics contract placing inventory in a foreign member state must trigger a indirect-tax registration review before the first goods movement. The question “does this warehouse arrangement create a local delivery obligation” should be part of every 3PL and fulfilment contract negotiation, not a post-implementation compliance discovery.

Scenario 4 — The UK Consultancy With a Partially Exempt EU Client Base

A London professional services firm services European clients exclusively on the reverse charge, issuing zero-rated invoices with reverse-charge annotation. Post-Brexit, it continues the same approach — technically correct for fully taxable EU corporate clients.

Two clients are EU financial institutions. One is a German bank (partially exempt — over 70% of its supplies are exempt financial services). The other is a Dutch insurer (fully exempt). The reverse charge applies to both in terms of place of supply. But both clients’ input-input recovery on these services is restricted — the German bank recovers approximately 28%, the Dutch insurer recovers nothing.

The consultancy’s invoicing approach is correct. The risk lies elsewhere: if either client has been overclaiming creditable input on the reverse-charged supplies — treating the full amount as recoverable input tax when it is not — their domestic fiscal authority will recover the overclaim, potentially with penalties, on audit. The consultancy has no direct exposure but may face commercial questions from clients if audits disclose the issue and the clients attribute the oversight to inadequate guidance during the engagement.

FAQ

What is the difference between B2B VAT and B2C levy in the union, and how do I determine which applies to my transaction

- The key differentiator is whether the buyer holds a verified registration number in their member state and purchases in their capacity as a taxable business person. When a buyer provides a number confirmed through VIES as active and valid, the provision is B2B — the reverse charge typically applies to cross-border services, and zero-rating applies to cross-border goods. When the buyer has no number, or provides one VIES cannot confirm, the transaction defaults to B2C. This means you collect the amount at the destination-country rate and remit through OSS or a local enrolment. The classification event belongs at the point of sale, built into your checkout or order flow — not deferred to a post-sale reconciliation process where errors have already compounded.

Do I need to obtain levy registration in every EU country where I sell to consumers

- Not under the current system. The OSS, introduced on 1 July 2021, allows a single registration in your home member state covering all B2C obligations across distance sales of goods and consumer services (including all ESS) through one quarterly return. You are required to use destination-country rates — and therefore need OSS — once your combined union-wide B2C turnover exceeds €10,000 in a calendar year. Below that threshold, your home-country rate applies to all European consumer transactions. Non-sellers in the bloc use the non-Union OSS, registering in any single state to cover the full EU consumer market from one filing point.

What is the reverse charge and when does it apply to my cross-border B2B sales

- The reverse charge shifts levy accounting from seller to buyer. On cross-border B2B services within the bloc, the general rule places output in the buyer’s jurisdiction. You issue a zero-rated invoice annotated “Reverse charge applies,” carry the buyer’s registration number, and remit nothing to any authority. The buyer calculates levy at their local rate, reports it as output tax, and reclaims it as input tax simultaneously — net cash-neutral to any fully taxable purchaser. The mechanism operates automatically when you supply goods or services to a registered EU business under the general B2B rule, and requires: a verified VIES-confirmed registration number on the invoice, confirmation that the buyer is acting as a taxable person, and that the general place-of-provision rule (not an exception) governs the transaction.

My operation handles both corporate clients and consumers. How do I structure compliance for B2B B2C sales

- Mixed operations need transaction-level classification before levy calculation — not after. At checkout or order creation, your system captures whether the buyer provides an enrolment number and validates it against VIES in real time. VIES-confirmed buyers route to the reverse-charge engine and B2B invoice template. All others route to the B2C rate matrix and OSS invoice template. B2B goods supplies generate EC Sales List entries. B2C supplies feed the OSS return by destination state. Maintaining these two streams as architecturally separate — distinct invoice formats, separate return lines, independent audit trails — is the foundational requirement. At scale, an ERP-integrated tax-determination engine handles real-time classification and rate lookup; without it, the manual reconciliation burden grows faster than transaction volume.

What are the consequences of misclassifying a transaction — treating B2C as B2B or vice versa

- Both directions create liability. Zero-rating a supply which should have carried destination-country levy (treating a consumer as a B2B buyer without VIES confirmation) leaves the seller owing that levy, plus interest from the original filing date, plus late-filing penalties — with no mechanism to recover the shortfall from the buyer who never paid it. Charging charge on a supply that qualified for the reverse charge (treating a registered business as a consumer) means the buyer overpaid and cannot reclaim input tax on an incorrectly formatted invoice. Correction requires a credit note, a compliant B2B invoice, an amended return, and a refund of the over-collected levy. Either error is correctable — but the correction cost and authority scrutiny it attracts scale with how long the error ran before detection, which is why real-time VIES validation at point of sale is the single most cost-effective compliance investment most cross-border EU operations can make.