VAT Registration Thresholds by Country 2026

VAT Registration Thresholds by Country 2026

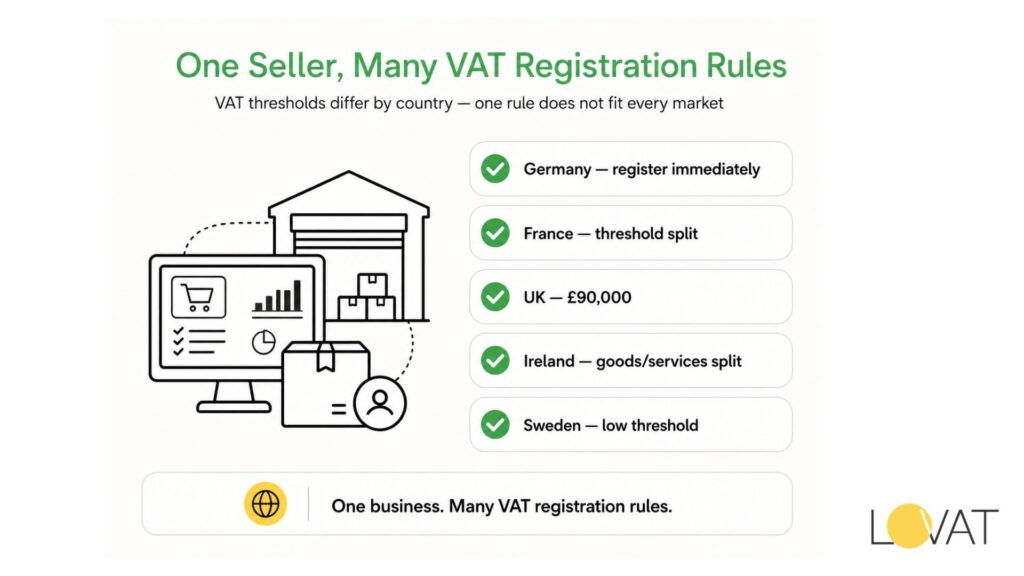

Get this wrong and you are trading illegally in a foreign market. The vat registration threshold is the annual turnover figure above which a business must register for VAT in a given country — and no two countries set it at the same level. Germany demands registration from your first sGet this wrong and you are trading illegally in a foreign market. The vat registration threshold is the annual turnover figure above which a business must register for VAT in a given country — and no two countries set it at the same level. Germany demands registration from your first sale. France gives resident traders room up to €85,800 on goods. The UK draws its line at £90,000. These gaps create both risk and opportunity for businesses operating across borders.

The numbers shifted again in 2025–2026. Austria raised its limit from €35,000 to €42,000. The UK moved its threshold from £85,000 to £90,000 on 1 April 2024, the largest single jump in two decades. Poland’s zloty-based figure fluctuates with exchange rates each year. Any compliance plan built on 2023 data needs updating before you file your next return.

This guide maps current registration thresholds across 12 major markets, explains the EU’s cross-border OSS system, breaks down the UK’s post-Brexit position, and covers Ireland’s two-tier structure in detail. No vague language — every figure below is the 2026 operative amount.

VAT Registration Threshold — What the Number Actually Means

A registration threshold is not a tax-free allowance. Revenue below the limit is still taxable in principle; the threshold simply determines whether the business itself must collect and remit the tax. Cross the line in any 12-month rolling period and registration becomes mandatory — usually within 30 days, sometimes immediately. The date you exceed the threshold, not the end of the financial year, is what triggers the clock.

Three types of threshold appear across European markets. The first is a universal domestic threshold that applies to resident businesses regardless of sector. The second is a sector-split version, where goods and services carry different limits (Ireland and France both use this). The third — most relevant to non-resident sellers — is zero: no threshold at all, mandatory registration from the first euro of sales. Germany, Italy for non-residents, and most non-EU countries operating under destination-tax principles fall into this last group.

The catch: exceeding a registration threshold in one country does not trigger registration in another. Each jurisdiction tracks turnover independently. A UK business selling €50,000 of goods into France and €50,000 into Germany might owe nothing in France (under the domestic threshold) but must register in Germany from sale number one. Blanket assumptions get businesses into trouble fast.

Taxable Turnover vs Total Revenue

Not every euro of revenue counts toward the threshold. Most jurisdictions measure taxable turnover, excluding VAT-exempt supplies such as financial services, residential lettings, and certain medical transactions. A business with €200,000 gross revenue but €150,000 in exempt supplies may sit below the registration line on taxable turnover alone. Get the definition right before you calculate.

VAT Threshold by Country — The 2026 Comparison

The table below sets out the operative VAT threshold by country for 12 major European markets as of January 2026. Figures for non-eurozone countries are shown in local currency with approximate euro equivalents based on Q4 2025 exchange rates. Non-resident thresholds are listed separately where they differ from the domestic figure.

| Country | Standard VAT Rate | Registration Threshold 2026 | Key Notes |

| Germany | 19 % | €0 (no threshold — register immediately) | Compulsory from first taxable supply |

| France | 20 % | €85,800 (goods) / €34,400 (services) | Two-tier threshold; lower for services |

| Italy | 22 % | €0 for non-residents; €85,000 for residents | Non-residents must register before trading |

| Spain | 21 % | €0 for non-residents; no general threshold | Resident traders: volume-based exemption |

| Netherlands | 21 % | €20,000 (small business KOR scheme) | KOR = optional flat exemption |

| Poland | 23 % | PLN 200,000 (~€46,000) | Złoty-denominated; reviewed annually |

| Sweden | 25 % | SEK 120,000 (~€10,500) | One of the lowest thresholds in the EU |

| Austria | 20 % | €42,000 | Threshold doubled from €35,000 in 2023 |

| Belgium | 21 % | €25,000 | Applies to resident traders only |

| Ireland | 23 % | €80,000 (goods) / €40,000 (services) | Split threshold — goods vs services |

| United Kingdom | 20 % | £90,000 | Post-Brexit; set by HMRC, not EU |

| Norway (EEA) | 25 % | NOK 50,000 (~€4,400) | Not EU; EEA rules apply |

Reading across country-by-country thresholds, a clear split emerges. Destination-based economies like Germany and Italy push non-residents to register immediately, protecting domestic traders who already carry a compliance cost. Countries with higher domestic limits — France at €85,800 and the UK at £90,000 — are partly protecting their own small business base from administrative burden, not making life easier for foreign sellers.

Sweden’s threshold of SEK 120,000 (roughly €10,500) is one of the lowest in the EU for resident businesses. A small Swedish artisan selling craft goods domestically hits the registration line faster than an equivalent business in almost any other member state. Nordic compliance costs are correspondingly high for micro-enterprises.

VAT Threshold EU — Harmonisation vs National Variation

The EU does not impose a single vat threshold eu-wide for domestic transactions. The VAT Directive sets a minimum floor — member states may grant exemptions to businesses with turnover below €85,000 — but each country chooses its own figure within that ceiling. The result is the patchwork visible in the table above. France is near the maximum. Sweden is near zero. Both are legally compliant with EU rules.

Where the EU has moved toward genuine harmonisation is on cross-border B2C sales. The One Stop Shop (OSS) scheme, mandatory from July 2021, changed the game for e-commerce. Any business selling goods or digital services to consumers across multiple member states can register for OSS in a single country and file one quarterly return covering all EU-wide sales. The trigger: €10,000 of cross-border B2C turnover in a calendar year. Below that figure, the seller can treat sales as domestic. Above it, the destination country’s VAT rate applies.

The EU-wide threshold of €10,000 catches more businesses than many operators expect. A Polish software company selling €900 per month to German consumers (€10,800 per year) crosses the OSS line in less than 12 months. OSS registration in Poland then covers all 27 member states — one return, one payment, no local registrations required. For businesses already above €10,000 in cross-border sales, avoiding OSS registration and filing locally in each member state is not cheaper. It is simply more complex.

The Import OSS Scheme for Non-EU Sellers

Non-EU businesses selling goods valued under €150 directly to EU consumers can use the Import One Stop Shop (IOSS). The IOSS threshold is per consignment, not annual turnover. Register in one member state, collect the destination country’s VAT at checkout, and remit via a single monthly return. Above €150 per consignment, customs duties and local VAT procedures apply instead.

VAT Registration Limits UK — Post-Brexit Rules in 2026

The VAT registration limits uk framework now operates entirely outside the EU VAT Directive. HMRC sets the threshold, the rates, and the exemption rules independently. As of 1 April 2024, the UK limit sits at £90,000 — the highest mandatory registration threshold of any G7 economy. A UK business can turn over £89,999 per year and remain legally outside the VAT system. The same business selling into France would need to consider French rules separately.

The UK’s registration limits apply on a rolling 12-month basis, not a calendar year. If your turnover crosses £90,000 at any point in the preceding 12 months, you must notify HMRC within 30 days and register from the beginning of the following month. There is also a forward-looking test: if you reasonably expect to exceed £90,000 in the next 30 days alone, registration is required immediately — before you cross the line.

Post-Brexit, UK businesses selling into the EU face the same rules as any non-EU seller. No OSS access, no domestic EU threshold benefit. A UK company generating €15,000 of B2C goods sales split across Germany and France must register separately in each country — or restructure via an EU-established entity to access OSS. This is one of the most underestimated Brexit compliance costs for e-commerce businesses with EU customer bases.

UK VAT Registration Limits — Voluntary Registration Below the Threshold

Businesses below £90,000 can register voluntarily. The UK VAT registration limits apply as a mandatory floor, not a ceiling on who can participate. Voluntary registration makes sense when your customers are VAT-registered businesses (they reclaim the VAT anyway) or when you have significant input tax to recover. A start-up spending £30,000 on equipment before making a single sale can reclaim that input tax by registering voluntarily from day one.

Voluntary registrants face the same filing obligations as mandatory ones: quarterly returns, Making Tax Digital (MTD) compatible software, and payment within one month and seven days of the period end. Deregistration is available when taxable turnover drops below the £88,000 deregistration threshold — a figure £2,000 below the registration limit, specifically designed to prevent businesses hovering around the line from constantly registering and deregistering.

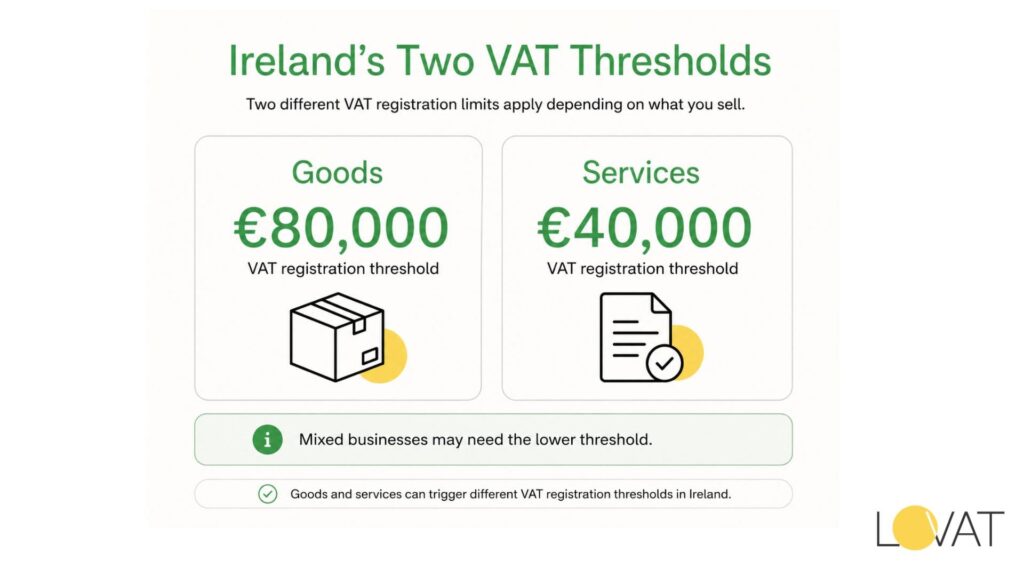

VAT Registration Limits Ireland — the €40,000 and €80,000 Split

Ireland operates a dual-threshold system that catches many businesses off-guard. The vat registration limits ireland structure separates goods from services: €80,000 for businesses supplying physical goods and €40,000 for service providers. A web design agency turning over €45,000 must register. A furniture retailer at the same turnover does not. The distinction matters because mixed businesses — those selling both products and services — must apply the lower limit if more than 90 % of their supplies are services.

Ireland’s limits have not been revised since 2019, despite inflation running above 4 % in 2022 and 2023. In real terms, the services threshold has shrunk. Revenue Commissioners have fielded repeated requests from SME lobbying groups to lift the €40,000 services limit. As of the 2026 Finance Act, no change has been enacted. Irish service businesses are therefore registering at lower real-income levels than businesses in Austria or the Netherlands.

Non-resident businesses supplying services to Irish consumers face a €0 threshold under the reverse charge mechanism — the Irish customer self-accounts for VAT above certain conditions. Digital services sold B2C follow EU OSS rules; the Irish revenue does not grant a separate domestic threshold to foreign digital sellers.

Cross-Border Sellers and the EU OSS €10,000 Threshold

The EU’s €10,000 cross-border rule sits within the broader framework of vat registration limits that apply to distance sellers. Below €10,000 in cross-border B2C sales per year, a business charges its home country’s VAT rate. Above €10,000, the destination country’s rate applies — and the seller must either register locally in every destination country or use OSS. Most businesses with any meaningful EU customer base exceed €10,000 within their first year of operation.

The applicable limits also interact with marketplace rules. If you sell on Amazon, Zalando, or another EU digital marketplace, the platform itself accounts for VAT on your B2C sales under the deemed supplier rules. Your individual turnover through that platform does not count toward your own OSS threshold for those sales. It does count for direct sales through your own website. Businesses mixing both channels need to track the two streams separately.

UK vs EU Registration Rules — A Side-by-Side View

The post-Brexit divergence between UK and EU VAT administration is clearest when mapped side by side. The table below compares the five most operationally significant differences for businesses trading across both markets.

| Feature | EU (OSS / domestic) | UK (post-Brexit) | Practical impact |

| Cross-border threshold | €10,000 OSS threshold for B2C digital/goods | No OSS equivalent — register in UK directly | EU sellers can file one OSS return; UK requires a separate HMRC registration |

| Domestic threshold | Varies by member state (€0 to €85,800) | £90,000 — one of the world’s highest | UK SMEs get more headroom before registering |

| Registration timeline | Before first supply in most member states | Within 30 days of breaching £90,000 | EU non-residents often must register on day one |

| Rate-setting body | EU VAT Directive sets minimum 15 % standard rate | HMRC sets rate independently | UK kept 20 % post-Brexit but is free to change it |

| Digital services (B2C) | OSS filing covers all 27 member states | Separate UK VAT registration required | Businesses serving both markets need two systems |

The practical conclusion: businesses with both UK and EU customers need two VAT infrastructures. OSS covers EU-wide B2C sales from a single registration. HMRC requires a completely separate UK registration, separate software, and a separate filing rhythm. No workaround exists under current rules — the UK deliberately chose not to join or mirror the OSS system post-Brexit.

What to Do When You Approach a Registration Threshold

Most businesses that miss a registration deadline do so because they were tracking annual turnover on a calendar-year basis rather than a rolling 12-month one. By the time December figures are clear, they are already late. Build a monthly rolling check into your bookkeeping process.

Four practical steps for businesses approaching any European threshold:

- Track taxable turnover monthly on a rolling 12-month basis, excluding exempt supplies

- Set an internal alert at 80 % of the relevant threshold — this gives roughly six to eight weeks of lead time for registration paperwork

- Identify whether your supplies cross any split-threshold categories (goods vs services in Ireland, France’s two-tier structure)

- For EU cross-border sales, check whether your combined B2C sales across all member states have passed €10,000 — OSS registration may be simpler than local registrations

Late registration penalties vary by country. HMRC charges a percentage of VAT owed since the date you should have registered — typically 5 % to 15 % depending on delay length. German authorities apply interest from the due date regardless of whether the shortfall was deliberate. Italian penalties for late registration start at 120 % of unpaid tax for the first offence.

Businesses that discover a historic registration gap have a narrow window to self-correct before a tax authority identifies the omission. Voluntary disclosure almost always attracts lower penalties than a triggered audit. A Hamburg-based accountancy firm advising UK e-commerce clients reports that most penalty settlements for late German registration run 30 % to 40 % lower under voluntary disclosure than under audit.

Related articles

Common Questions About

VAT Registration Thresholds by Country 2026

What is the VAT registration threshold in the EU for non-resident sellers?

Most EU member states set their domestic thresholds for resident businesses only. Non-residents — businesses established outside the EU — typically face a €0 threshold and must register before their first taxable supply in that country. The exception is the OSS scheme for cross-border B2C sales, which allows registration in one member state covering all 27, triggered at €10,000 of annual cross-border turnover.

Has the UK VAT threshold changed for 2026

The UK threshold moved to £90,000 on 1 April 2024 and has not changed since. HMRC typically reviews the figure in each autumn Budget. No change was announced for 2025–2026 in the October 2024 Budget, so £90,000 remains the operative limit. The deregistration threshold stays at £88,000.

Does Ireland have separate VAT thresholds for goods and services

Yes. Ireland’s split runs at €80,000 for goods and €40,000 for services. Mixed businesses apply the lower services threshold if more than 90 % of their supplies are services. Neither figure has been updated since 2019.

Can a small business in the UK use the EU OSS after Brexit

No. OSS is available only to businesses established in an EU member state or using an EU-based intermediary for IOSS purposes. A UK-only business must register for VAT locally in each EU country where it has taxable sales, or establish an EU entity that can then use OSS. Some businesses use a single EU subsidiary (commonly in Ireland or the Netherlands) as the OSS registrant for all EU sales.

What happens if you exceed the VAT threshold and do not register

The liability for unpaid VAT accrues from the date you should have registered, not from when you eventually do. HMRC, the German Finanzamt, and other revenue authorities can raise assessments covering the full period of non-registration plus interest and penalties. In serious cases involving deliberate non-compliance, criminal prosecution is possible. Voluntary disclosure before a formal inquiry almost always reduces the total bill. . Talk to a VAT expert